Shares of data-warehousing company Snowflake (SNOW) have been crushed by the broader market sell-off. Shares lost around 72% of their value from peak to trough, briefly falling below the IPO price of $120 per share. Undoubtedly, the window to buy Snowflake stock below IPO levels came and went very quickly. Even if the broader market has yet to bottom out, I think the value proposition in Snowflake is hard to pass up at this juncture.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Snowflake may be a high-multiple growth stock, but unlike many of its more speculative peers, it has a path towards greater cash flow and margins. Further, its growth profile seems to be underestimated in a market that no longer cares as much for sales growth.

Though a coming recession could slow sales growth (it’s likely to look way worse, given Snowflake’s usage-based revenue recognition model), the long-term growth trajectory still seems as strong as ever. In short, Snowflake is still a hyper-growth company. It’s merely moving through a more challenging environment. As it does, the company will take steps to add even more innovations while improving its profitability prospects.

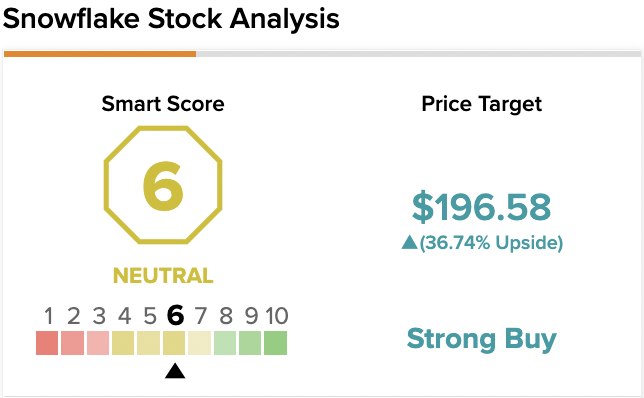

On TipRanks, SNOW scores a 6 out of 10 on the Smart Score spectrum. This indicates a potential for the stock to perform in-line with the broader market.

Snowflake: Sales and Margin Growth Together?

Usually, when you have hyper-growth, you can’t have substantial margin expansion and robust cash flows. That’s what makes Snowflake such an exciting company. It can grow at a staggering rate while maintaining profitability. Though profitability prospects could take a few steps back over the near term, I find it encouraging that the firm can grow without having to reinvest too much capital in its business.

Still, Snowflake will continue to invest where it makes sense. Whether through industry-specific services to entice more usage or going on the hunt for acquisition opportunities after the recent tech carnage, Snowflake still has its foot on the pedal.

Despite the recent Snowflake avalanche, Wall Street analysts remain incredibly bullish. The stock received a few upgrades over the past few months, and it’s not a mystery why.

JP Morgan’s annual chief information officer survey revealed that Snowflake was rated number one in installed-based spending intentions, beating out many enterprise behemoths.

Though price targets have decreased considerably in recent months, I remain bullish on Snowflake.

Snowflake Customers Love the Platform, and They Could Up Their Usage

The Snowflake platform allows corporations to unlock the full power of their data. Indeed, data is the new commodity, and Snowflake has the tools to help firms refine such data into something more useful.

Given that the platform creates so much value for users, it will be difficult for firms to cut Snowflake usage spending, even as the lights go out on the broader economy.

While IT spending could prove more resilient, Snowflake’s usage-based model is likely to introduce even more noise in coming quarters. And given how jittery investors have been of late, such noise is likely to be mistaken for something more ominous.

Looking ahead, CEO Frank Slootman looks to have lowered the bar amid macro uncertainties. Though Snowflake’s “noisy” revenue model warrants caution when it comes to forward-looking guidance, I think the potential to overshoot such a low bar is high.

Many firms are just beginning to harness the power of the Snowflake platform. The more firms use the platform, the more they’ll discover the value in increasing their usage. Though it could take years, Snowflake’s usage-based model could pay off in time once data-heavy firms start ramping up their usage.

Wall Street’s Take

According to TipRanks’ analyst rating consensus, SNOW stock comes in as a Strong Buy. Out of 28 analyst ratings, there are 23 Buy recommendations, four Hold recommendations, and one Sell recommendation.

The average Snowflake price target is $196.58, implying an upside of 36.74%. Analyst price targets range from a low of $120 per share to a high of $295 per share.

The Bottom Line on Snowflake Stock

Snowflake is a unique company with a very economical business model that can allow growth and margin expansion. Of all the stocks that have shed more than 70% of their value, Snowflake, I believe, is likeliest to see its highs again in this decade.

Even if a recession happens over the next year, Slootman and company continue to move forward with cutting-edge innovations.

Undoubtedly, it’s hard for investors, analysts, and even prospective users to understand the full extent of the intricate Snowflake platform. As the company shines a light on industry-specific applications, many firms will grow increasingly curious about what they’re missing out on. And it’s this curiosity that could help Snowflake capture its massive total addressable market, even if IT spending takes a hit come the next recession.

CIOs love the Snowflake platform, and they’re likely to push companies to spend more on usage as the digital transformation continues.

Read full Disclosure