Snap (SNAP) has had its fair share of ups and downs this year. First, the company’s stock jumped almost 60% on February 4th after its first quarter’s financial forecast was updated.

However, the surge was short-lived. The stock shed more than 40% on May 24th after the CEO declared that the company is expected to generate lower revenue and earnings than expected and pull back on hiring in the future.

Currently, the stock is down more than 82% off its all-time high, which has sparked curiosity among investors about buying SNAP. It is common to grab a stock after a steep devaluation, but SNAP stock likely remains a risky play at this stage. I am bearish on SNAP stock.

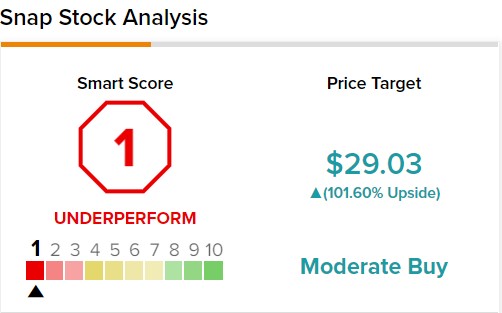

Also, on TipRanks, SNAP stock receives a 1 out of 10 Smart Score Rating, indicating a high potential for the stock to underperform the broader market.

The Broader Economy Affects Advertising Demand

SNAP is free for customers to install and use. Currently, the platform enjoys 332 million active users compared to the 318 million in the last quarter. Since it is free, the company generates revenue by running ads on its app and website.

The competitive edge for SNAP is that users browsing on their phones are more likely to be swayed by an ad on their phones than other mediums. This gives value to SNAP advertisements and propels advertisers to invest in the company. However, the macroeconomic headwinds could hamper ad expenditure in 2022.

The COVID-19-induced lockdown caused supply-chain issues for many businesses. Given the demand and supply imbalance, companies are less motivated to advertise their products. Moreover, Russia’s invasion has worsened supply-chain problems, further resulting in marketers reducing ad spending in many regions.

Another problem that SNAP faces is Apple’s revised ad-tracking policies. Apple’s policies have made it challenging for marketers to target ads to their potential customers. This factor has hit SNAP hard this year and might continue to haunt the company for a long time.

These headwinds forced SNAP to warn investors that the company might not fulfill its second-quarter guidance. The same headwinds resulted in SNAP plummeting by more than 40% in one day, as mentioned earlier.

Will a Reduction in Hiring Affect SNAP’s growth?

Investors’ confidence has been shattered of late due to rising interest rates, high inflation, the Russia/Ukraine war, and supply-chain issues. The uncertainty has harmed many companies in different industries. The problem is that there’s only so much that companies can do to alter the external environment. Hence, they must wait and suffer till the macro economy stabilizes.

Given high labor costs and slow revenue growth, Spiegel, SNAP’s CEO, said that the company would reduce its pace of hiring workers for the rest of 2022. The CEO suggested that SNAP employ around 500 new employees vs. the 2000 employees hired last year and reiterated that he expects existing employees to work productively.

Spiegel also mentioned that upper management had been asked to review spending. This means the company will cut spending on areas contributing the lowest to growth. Slow hiring entails that the company will slow down its prospects, affecting revenue and profits.

A Move Away from Technology Investments

Brent Thill, an analyst at Jefferies, said that investors are shy of shifting away from technology investments. In addition, the technology sector is facing a downturn as the pandemic ends.

However, lower investment in technology isn’t the only problem for SNAP. For SNAP, the other difficulty is the rise of TikTok. The new and widely used platform has given tough competition to Facebook and Snapchat as its weekly usage continues to increase.

The high TikTok penetration could pose significant threats for SNAP if advertisers shift to the new and trendy platform. Hence, the company has to fight inflation, uncertainty in the global markets, supply-chain problems, and competition.

Wall Street’s Take

Turning to Wall Street, SNAP stock maintains a Moderate Buy consensus rating. Out of 32 total analyst ratings, 24 Buys, six Holds, and two Sell ratings were assigned over the past three months.

The average SNAP stock price target is $29.03, implying 100.9% upside potential. Analyst price targets range from a low of $14 per share to a high of $59 per share.

Takeaway – Is SNAP Stock Attractive?

SNAP has crashed almost 70% year-to-date. However, the stock likely isn’t a cheap Buy even after the crash. SNAP has a price-to-sales ratio of 5.5x, which is more expensive compared to its peers, Pinterest (PINS) and Meta Platforms (META). Moreover, Apple’s privacy changes are likely to weigh down the company’s fundamentals for the foreseeable future.

Additionally, the macroeconomic issues don’t be fading away anytime soon with the Federal continuing to raise interest rates to fight the inflationary pressures. Hence, investors should probably employ the wait-and-see approach before thinking about investing in SNAP stock.