One company that income-oriented investors have historically appreciated for its hefty dividends and overall qualities is Simon Property Group (NYSE: SPG). Shares of the company have declined considerably year-to-date, pushing the stock’s dividend yield to a sizable 7%. With the dividend appearing relatively well-covered and the stock’s valuation being rather cheap, in my view, I am bullish on the stock.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

With the market becoming more unpredictable by the day due to the current highly speculative macroeconomic and geopolitical landscapes, sizable dividend yields can reduce uncertainty and increase the overall predictability of a stock’s investment case.

SPG is a High-Quality REIT

Investors are usually skeptical when it comes to retail REITs, and for a good reason. With foot traffic in retail locations remaining rather soft despite the pandemic fading away and their growth prospects lacking meaningful catalysts, it makes sense retail REITs are not particularly popular these days. However, Simon Property Group features multiple qualities that differentiate it from its peers.

Firstly, with a market capitalization of around $32.6 billion, Simon is the second most valuable retail REIT in the U.S., only behind Realty Income (NYSE: O). Accordingly, Simon’s operations are exceptionally diversified.

Specifically, Simon owned or held an interest in 198 income-producing properties, according to its latest filings. They comprised 69 Premium Outlets, 94 malls, 14 Mills, six lifestyle centers, and 15 other retail properties located in 37 states and Puerto Rico. Simon also owns an 80% non-controlling interest in the formerly publicly traded Taubman Realty Group, which it bought out in 2020.

Further, the company’s international exposure boosts its geographical diversification, with Simon owning a 22.4% equity stake in Klépierre SA (PARIS: KLPEF), a French publicly-traded REIT that has, in turn, an interest in shopping centers located across 14 European countries.

Moreover, Simon’s aspiration is for its properties to be the prime destination for high-end retailers and their customers. This means that the company attracts high-quality tenants that cater to the high-end consumer, which has increased purchasing power.

Hence, Simon is not troubled with low-grade retailers whose financials can be easily impacted during a market downturn and which, in turn, would result in lower rent collections. This is evident by the fact that Simon currently features a base minimum rent of $54.1 per square foot, on average, which is incredibly high for retail space.

Another Rock-Solid Quarter for Simon Property Group

Despite Simon being one of the highest quality retail REITs out there, the company was impacted notably during the pandemic. However, its recovery momentum was strong last year, and the company has continued to improve since, as was the case in its most recent Q2 results.

Simon’s total revenues reached $1.28 billion, a 2.4% increase compared to last year. The improvement in revenues was primarily supported by strong leasing momentum and occupancy levels remaining elevated. Thus, FFO per share also grew, albeit by a humbler 1.4% to $2.96.

Simon’s portfolio NOI, which incorporates domestic properties, international properties, and Simon’s ownership in Taubman Realty Group, climbed by 4.6% compared to Q2 2021. This indicates that the company’s oversized buyout of Taubman continues to be accretive to Simon’s overall performance. Additionally, occupancy improved further, coming in at 93.8% compared to 91.8% last year or 93.8% last quarter. This is quite impressive considering the hurdles attached to the current economic environment.

With management growing optimistic amid a better-than-expected first half to Fiscal Year 2022, they raised their prior full-year outlook, now expecting FFO/share to be in the range of $11.70 to $11.77, up from 11.60 to $11.75 previously.

This range is quite close to the company’s pre-pandemic FFO/share number of $12.37 in Fiscal Year 2019, which indicates almost a full recovery in a very short period of time. This is attributed to Simon’s forenamed qualities, in my view, and specifically the company’s focus on high-quality tenants.

SPG Stock’s 7% Dividend Yield is Reliable

While Simon prudently cut its dividend during the pandemic, I believe that SPG stock’s current 7% dividend is reliable. This is backed by the fact that along with its Q2 results, the company increased its dividend for a sixth consecutive quarter to a quarterly rate of $1.75, marking a 6.1% increase sequentially, or a 16.6% increase year-over-year.

Additionally, the current annual dividend run-rate of $7.00, and the midpoint of management’s guidance, imply a comfortable payout ratio of 60%. Considering the sequential hikes and room for further hikes, the quarterly dividend should reach and even surpass its pre-pandemic levels sooner than later.

Is SPG Stock a Good Buy?

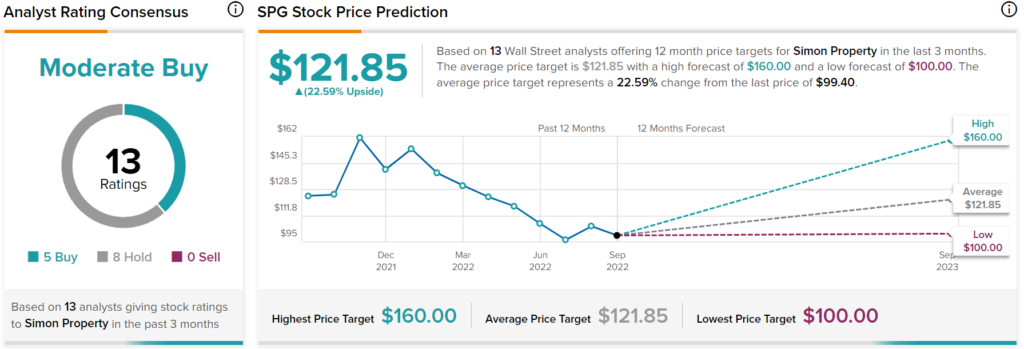

Regarding Wall Street’s sentiment on Simon Property Group, the stock has a Moderate Buy consensus rating based on five Buys and eight Holds assigned in the past three months. At $121.85, the average SPG price target implies a 22.6% upside potential.

Takeaway – SPG Stock Has a Wide Margin of Safety

Simon’s quality traits come in handy in the current, full-of-uncertainty economic environment. Additionally, based on the midpoint of management’s guidance, shares are trading at a P/FFO of roughly 8.5 at their current price levels, which, combined with the relatively well-covered 7% dividend yield, should provide investors a wide margin of safety.

The ongoing market setup may continue to apply pressure to shares of Simon. However, assuming the stock’s valuation returns towards its historical average of a P/FFO in the low teens, combined with the current dividend yield and assumptions of FFO/share in the low single-digits, investors could be easily looking at double-digit annualized over the medium-term. Accordingly, I am bullish on the stock.