Paint and coating manufacturer Sherwin-Williams (SHW) shares slipped about 38% from peak to trough before bouncing back sharply. Now down 30% from its high, it’s in a tough spot. While there’s no denying SHW’s brand power among painters and homeowners, the implications of a coming recession may yet be fully factored into the share price.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

For now, I am bearish on Sherwin-Williams stock, primarily due to valuation concerns.

Nonetheless, architectural paint demand has remained robust. Despite the possibility of a drastic economic slowdown, the management team still expects 2022 sales to be in the high single-digit or low double-digit range. What’s behind management’s guidance reaffirmation?

A great deal of supply-chain disturbances and inflationary pressures could fade over coming quarters. SHW has done a relatively decent job of navigating through such transitory hurdles. Even if the worst of the supply-side issues are in the rear-view mirror, it’s tough to tell how sharply demand could slip if we are headed for a recession in 2023.

Recessionary headwinds could offset the long-term secular trends that have been powering SHW stock higher. Indeed, there’s a big risk that the stock could sink further if the weakening macro picture weighs on coming results. This could skew sales growth towards the lower end of the range, if not lower.

Economic Weakness Could Paint an Ugly Picture

Management’s 2022 reaffirmation is a huge sign of confidence. If the macro picture fades more than the firm expects, the stage could be set for a vicious leg lower. Arguably, it’s better to err on the side of caution these days, with so much in the way of macro uncertainty.

With interest rates on the rise and home sales likely to grind lower, investments in home renovations could be postponed indefinitely. Still, Sherwin-Williams derives around 30% of its overall sales from coatings, which provides the firm with greater diversification and a bit more resilience from an economic downturn.

When it comes to industrial coatings, Sherwin-Williams is a force to be reckoned with. However, the global coatings market tends to be more commoditized than its paints business.

Though margins from the coatings business are likely to remain modest over the long haul as a result of greater competition, I do view coatings as a great backdrop to help SHW better deal with a harsher economic environment. Further, the firm could do a better job of flexing its brand strength to enhance its coating margins.

The real source of Sherwin-Williams’ moat lies with its paint business. Should the coming recession weigh heavily on residential construction, SHW stock’s premier price tag could lose even more ground.

At writing, shares of SHW trade at 35.8 times trailing earnings and 26.6 times cash flow. That’s a lofty multiple, given the potential for a 2023 downturn.

SHW Has a High Smart Score Rating

On TipRanks, SHW has a 9 out of 10 on the Smart Score rating. This indicates solid potential for the stock to outperform the broader market.

Analysts are Moderately Bullish on the Stock

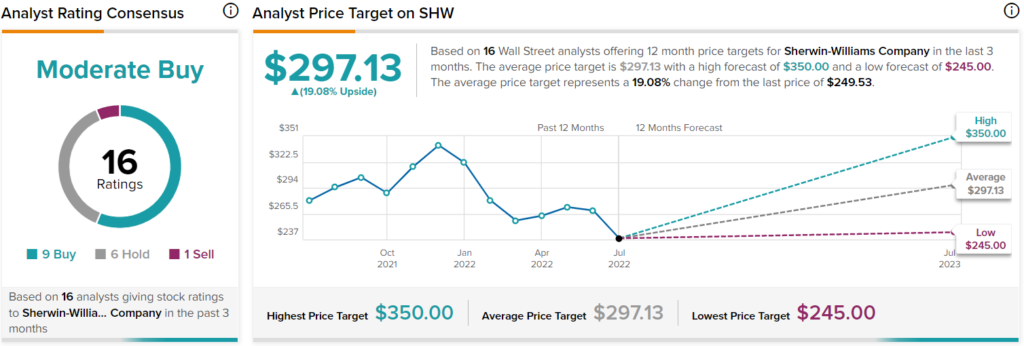

Turning to Wall Street, SHW stock comes in as a Moderate Buy. Out of 16 analyst ratings, there are nine Buys, six Holds, and one Sell.

The average Sherwin-Williams price target is $297.13, implying upside potential of 19.1%. Analyst price targets range from a low of $245.00 per share to a high of $350.00 per share.

Conclusion: Sherwin-Williams is Not Immune to Recessions

Sherwin-Williams is an incredibly well-run company that has a wide moat in its brand. Despite its stellar performance through recent pandemic and inflationary headwinds, the firm will not be immune from the effects of a recession. The architectural market tends to be very cyclical, and such cyclicality could result in wild swings in the stock.

Though Sherwin-Williams stock deserves a premium multiple, just how much a premium is a significant question mark at this time.

Wall Street analysts remain fairly bullish, but there have been a number of price target downgrades of late. Just over a week ago, Bank of America Securities analyst Steve Byrne downgraded the stock to “Hold” from “Buy.”

Could more such downgrades be in the cards as SHW’s relief bounce runs out of steam?

Perhaps. The analyst community has not been the biggest fan of discretionary or cyclical stocks with rising recession risks. Continued downgrades could apply even more pressure on the stock as the firm approaches its second-quarter earnings results due on July 27, 2022. It’s sure to be a nail-biter for investors.