The bull market that has been charging for the past year has seen a surge in volatility recently. The Chinese startup DeepSeek released its latest AI model, R1, and shook up the tech world with claims that the new AI consumes just a fraction of the computing power as existing big-name AIs and has been much cheaper to develop – but gives comparable results. This rattled AI-related stocks as investors scrambled to gauge the impact of a low-cost, high-efficiency competitor shaking up the industry.

This development came alongside the most recent Federal Reserve statements, which hinted that the central bank will not be cutting interest rates this month. This was not completely unexpected – but it does imply that rates will remain elevated for longer than market watchers had hoped.

Amid these shifts, investors are seeking ways to build resilient portfolios that can thrive in any market environment. That’s where dividend stocks come in. That’s where dividend stocks come in. The best ones offer a steady income stream, with yields that not only beat inflation but also outshine current interest rates.

We’ve opened up the TipRanks database to find two such dividend stocks – stocks with dividend yields that reach as high as 13%. In addition, the shares we’ll look at here have been tagged by some of Wall Street’s analysts as potential winners for 2025. Let’s give them a closer.

MFA Financial (MFA)

First up is a real estate investment trust (REIT), MFA Financial. MFA operates as a specialty finance company, investing shareholder money in residential mortgage loans and mortgage-backed securities (MBSs), as well as other real estate assets. The company conducts its activities through direct purchase of properties and by financing loans on mortgages. MFA’s portfolio totals $10.5 billion, with the largest part, $4.2 billion, being in non-QM residential mortgage loans. In addition, the company has substantial positions in residential transitional loans and single-family rental loans. Together, these three segments make up $8 billion of the company’s investment portfolio.

Being a REIT, MFA is required by tax regulations to return profits directly to shareholders, and like most of its peers the company uses dividends as a means of compliance. MFA last declared its dividend payment on December 11, and the payout went out on January 31 at a rate of 35 cents per common share. This marked the ninth quarter in a row with the dividend at this level. The $1.40 annualized payment per common share gives a forward yield of 13.3%.

The company supports its dividend policy through its real estate activities. In the last reported quarter, 3Q24, MFA’s net interest income came to $50.6 million. While up almost 10% year-over-year, this figure missed the forecast by $6.57 million. The company’s bottom line was reported as a non-GAAP EPS of 37 cents. This was 4 cents per share lower than had been expected – but it was also a strong reversal of the 64-cent per share EPS loss reported in 3Q23. MFA’s distributable earnings per share also came to 37 cents, and directly supports the company’s dividend payment.

In his coverage of this stock for Janney, analyst Jason Stewart explains that he likes MFA for its exposure to MBS assets, as well as its likely trajectory given today’s mortgage market. Stewart says of the company and its position, “Historically, investors have fared well capitalizing on government intervention as non-economic participants in markets. Thematically, investment in the high-quality, liquid agency MBS market at current economic returns is attractive and MFA has been opportunistically growing the agency MBS portfolio. Mortgage spreads are wider than long-term averages and likely to tighten as fixed income volatility declines, driving MFA’s book value higher. MFA shares are trading at a steep discount to current GAAP BVPS and economic BVPS. We expect mid-single-digit growth in BVPS and multiple expansion toward economic book value.”

Stewart quantifies his position with a Buy rating, and a $14 price target that points toward a one-year upside potential for the stock of 33%. With the dividend return added in, that one-year return may reach as high as 46%. (To watch Stewart’s track record, click here)

This stock gets a Moderate Buy rating from the Street consensus, based on 5 reviews that include 3 Buys and 2 Holds. The shares are priced at $10.50 and their $12.55 average target price implies a 12-month gain of 19.5%. (See MFA stock forecast)

Apple Hospitality REIT (APLE)

Next on our list is Apple Hospitality REIT, a company with a narrow focus on real estate in the leisure industry. Specifically, Apple has built up a portfolio of hotels, upscale properties with a focus on maximizing guest rooms. The company’s hotels are spread across 37 states in 86 markets. In all, Apple owns 221 hotels with more than 29,700 guest rooms. Brands in the company’s portfolio include such names as Marriott, Courtyard by Marriott, Hampton by Hilton, and Hyatt House.

Apple’s properties are widespread. The company has 22 hotels in Florida, 26 in Texas, and another 26 in California. Apple even owns properties in Portland, Maine, and Anchorage, Alaska. The key point: the company’s properties are located in places with strong demand, close access to guest amenities, and a track record of delivering consistent performance.

Turning to that performance, we find that Apple realized revenues of $378.84 million from its properties in 3Q24. This was up 5.7% year-over-year, although it came in just under expectations, missing by some $800,000. Apple reported funds from operations, a key metric for REITs, of 45 cents per share. This was in line with the forecasts and matched the 3Q23 result.

Apple’s results were more than strong enough to support the company’s common share dividend, which is paid out monthly rather than quarterly. The dividend for February was declared in January 17 for 8 cents per common share. This annualizes to 96 cents per common share and gives a forward yield of 6.14%.

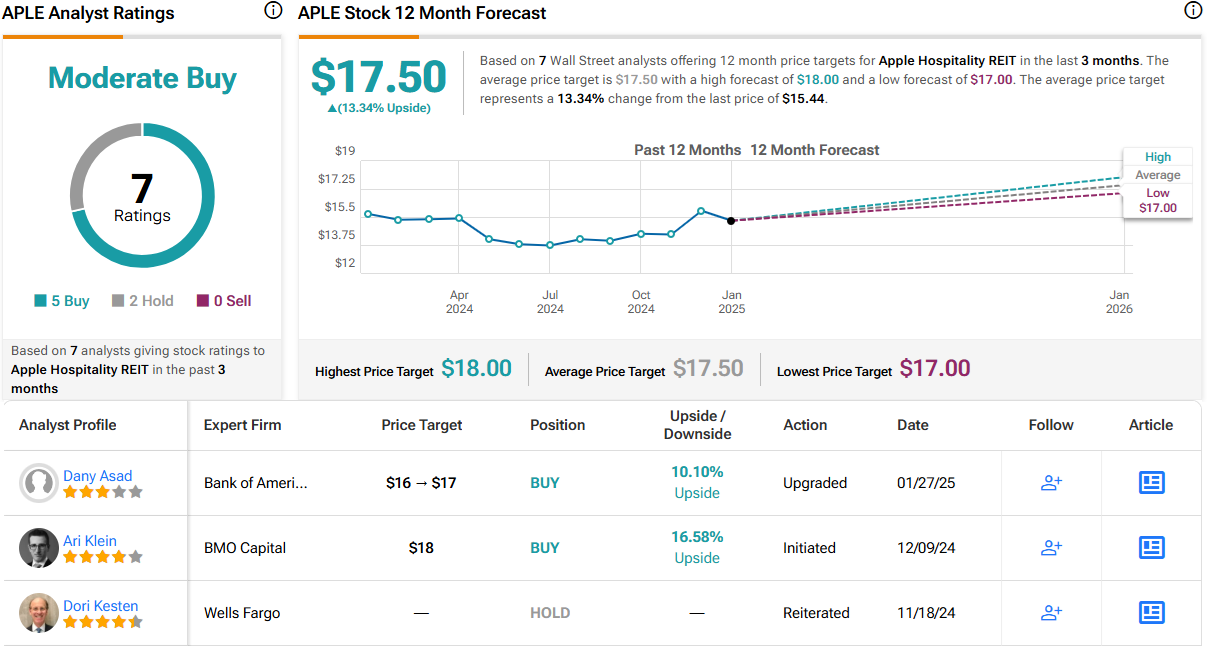

This stock has come to the attention of Dany Asad from Bank of America, who sees several reasons for an upbeat view on APLE—starting with the old standby of the real estate market, location. He writes, “We are upgrading Apple Hospitality from Neutral to Buy as 1) location, geographic and segment mix all skew favorably to this select service portfolio, 2) capital needs are limited given the low average age of the assets and 3) its dividend yield is above peers.”

Getting deeper into the details, the BofA analyst adds, “Apple is one of the most capital efficient companies in our REIT coverage, with capex as a % of revenue at 6% (vs peers at 9%). Its average effective age of hotels of 4-5 years is stable since 2019, meaning low deferred maintenance. High margins, low leverage and lower capex drives attractive Adjusted FFO, a strong and well covered dividend and should allow APLE to go on offense if the hotel M&A environment accelerates in 2025.”

Asad gives APLE shares a Buy rating and a price target of $17 that suggests a 10% gain on the one-year horizon. With the annualized dividend yield, the total return is likely to exceed 16%. (To watch Asad’s track record, click here)

Overall, this stock has a Moderate Buy consensus rating, based on 7 reviews that show a breakdown of 5 to Buy and 2 to Hold. The shares are trading for $15.44 and have an average price target of $17.50, implying a potential one-year gain of 13%. (See APLE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.