You can’t really go wrong with dividend stocks. These equities provide a stable, long-term income stream, one that supplements the return from share appreciation. And even if the share price goes down, you can still make bank via the dividend. It’s a solid advantage to add to any stock portfolio – and can be made even better by the high-yield dividends, ones that can provide yields of 9% or better.

For investors seeking out these high-yield dividend payers, the street’s analysts are on the job. They’ve been sorting through the ranks of div stocks, and tagging some of the 9%+ high-yield payers as Buys right now.

We’ve used the TipRanks platform to pull up the details on two of these picks. Let’s dive in.

Hercules Capital (HTGC)

We’ll start with Hercules Capital, a BDC, or business development company. Hercules focuses its work on emerging companies, particularly those with a bent toward the sciences and technology – life sciences, sustainable and renewable tech, and SaaS finance tech. Hercules is a leading specialty finance provider in this niche, supporting a venture capital-backed clientele with access to credit services and growth capital financing.

Since its founding in 2003, Hercules has provided funding for over 660 companies, to a total of $21 billion-plus in capital commitments. The company currently has over $4.6 billion in assets under management.

On the dividend side, Hercules has a long-standing commitment to keeping up capital returns to shareholders. The company’s current regular dividend, last declared on October 28 for payment this coming November 20, was set at 40 cents per common share and was supplemented by an 8 cent per share special dividend. The combined dividend payment, of 48 cents per common share, annualizes to $1.92 per share and gives a strong forward yield of 9.75%.

That dividend is supported by Hercules’ financial results, which were reported at the end of October for 3Q24. The company’s total investment income in the quarter was reported as $125.25 million, stated by management to be a company quarterly record. The investment income figure was up 7.3% year-over-year, although it missed expectations by $2.9 million. At the bottom line, Hercules had a quarterly net investment income of 51 cents per share.

This BDC has caught the attention of JMP’s Brian McKenna, an analyst ranked in the top 2% of Wall Street stock experts, who is impressed by Hercules’ business strength. McKenna writes of the firm, “Hercules continues to demonstrate its leading position within the venture lending space, and we are quite pleased again with the strength of quarterly results as well as the trajectory of the business into year-end. Lower base rates and tighter spreads will clearly be somewhat of a headwind within the P&L moving forward, but we also believe the company has demonstrated its ability to consistently deliver ROEs in the mid-to-upper teens through the cycle. So, while the stock trades at a healthy valuation multiple on paper, we believe underlying results and the outlook for the business more than justify this multiple.”

Quantifying his stance, the 5-star analyst puts an Outperform (Buy) rating on this stock, with a $22 price target that points toward a one-year upside potential of 11.5%. Add in the dividend yield, the potential one-year return on HTGC rises to 21.5%. (To watch McKenna’s track record, click here)

Overall, the stock has a Moderate Buy consensus rating, based on 6 recent reviews that split evenly into 3 Buys and Holds, each. The stock’s $19.7 trading price and $20.29 average target price combine to imply a modest 3% increase over the next 12 months. (See HTGC stock forecast)

Ares Capital Corporation (ARCC)

The second stock we’ll look at, Ares Capital Corp., is a BDC with 20 years’ experience under its belt. The company operates as a provider of credit and financing services to the small business sector in the US market, the small- and mid-sized companies that are the traditional drivers of the US economy. Ares’ services are essential for its clients, giving them the resources they need to thrive; in return, Ares reaps the return on its varied business investments.

In its lifetime, Ares has built up a portfolio with a $25.9 billion fair value, as of this past September 30. The company has investments in 535 client firms, and those investments are backed by 240 private equity sponsors. The company’s portfolio leans heavily on first lien senior secured loans, which make up 52.8% of the total. Second lien senior secured loans make up 10.6% of the total, and preferred equity securities comprise 10.4% of the portfolio. By industry composition, Ares’ largest investment targets are the software & services sector (25.4%), health care services (12.8%), and commercial & professional services (10.7%).

The company’s current common share dividend is set at 48 cents per share, and has been at this level for 9 quarters now. The dividend was last declared on October 30 for a payment on December 30. The 48-cent dividend annualizes to $1.92 per common share, and the forward yield is currently 9%.

Turning to its financial results, Ares Capital Corp. reported the 3Q24 figures at the end of last month. The company showed a total investment income of $775 million, up more than 18% from the prior year period – and $1.69 million ahead of the forecast. At the bottom line, however, the company’s non-GAAP earnings missed; the 58-cent EPS was a penny lower than had been anticipated.

The EPS miss didn’t bother RBC analyst Kenneth Lee, who is rated by TipRanks among the top 1% of Wall Street’s analysts, and who said of Ares Capital, “Credit performance remains solid; arguably, there is less downside risk given favorable macro backdrop. Focus likely to turn more towards the down rate cycle given floating-rate assets; our updated model still embeds multiple rate cuts and we still see well-supported dividends. Maintain our Outperform rating, as we favor ARCC’s strong track record of managing risks through the cycle, well-supported dividends, and scale advantages.”

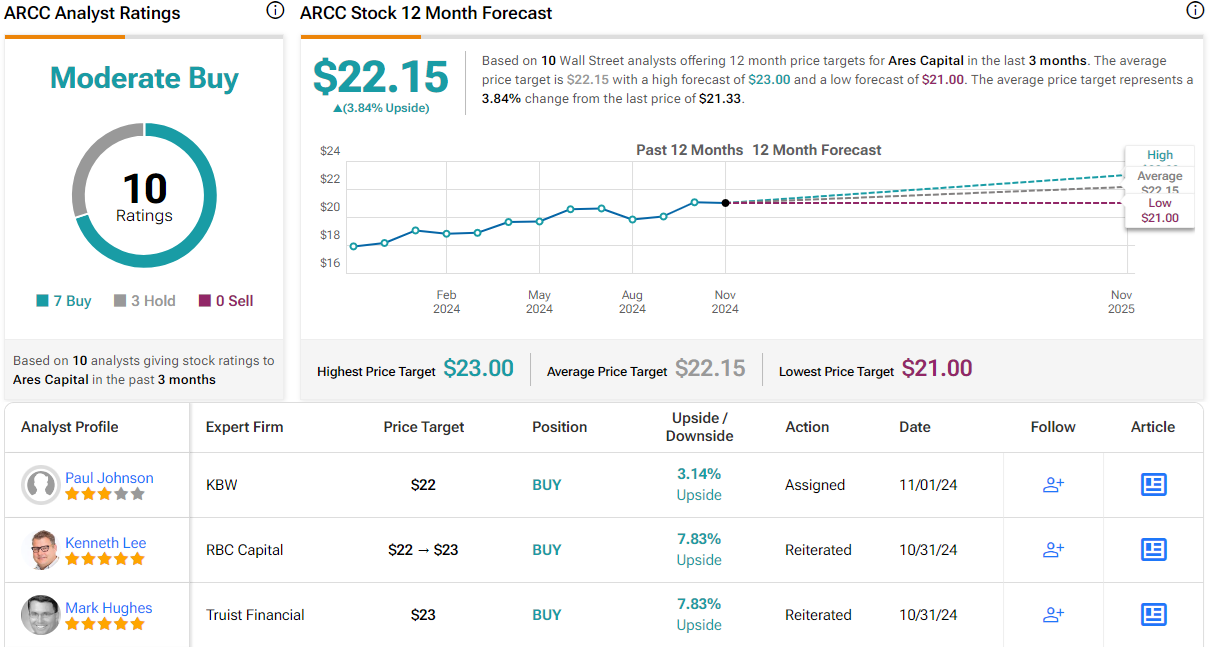

That Outperform (Buy) rating is backed by a $23 price target that indicates an upside of 8% for the year ahead. Adding in the dividend yield, the potential return here can reach as high as 18%. (To watch Lee’s track record, click here)

There are 10 recent Wall Street reviews on record for ARCC, and their breakdown includes 7 Buys to 3 Holds for a Moderate Buy consensus rating. The stock is priced at $21.33 and the average target price of $22.15 implies a gain of 4% on the one-year horizon. (See ARCC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.