Just where is the stock market going, that’s the question investors are trying to answer. The answer isn’t fully clear, though; markets have fallen for most of this year, but the last few days have seen the best trading in weeks. The problem is, investors and economists aren’t sure if we’re at a true bottom or just in the midst of a bear market rally.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

What happens next is anyone’s guess, but the history of bears and rallies can offer some suggestions. Looking back to the end of the Second World War, single-day S&P rallies of more than 2.76%, as we saw this week, are hardly rare – but 65% of them came during bear markets, and most of those came before the true bottom was found.

If that is true, then investors should start looking for the defensive plays that will protect them when the markets shift downward again.

High-yield dividends are customary move in that regard – and we’ve found two dividend stocks in the TipRanks database that are yielding 10% or better. That’s some 5x higher than average, and yields don’t get much better than that. Even better or investors, both stocks also feature Buy ratings from the Street’s analysts and double-digit share gain potential for the year ahead. It’s a combination that presents a clear advantage for defensive investors.

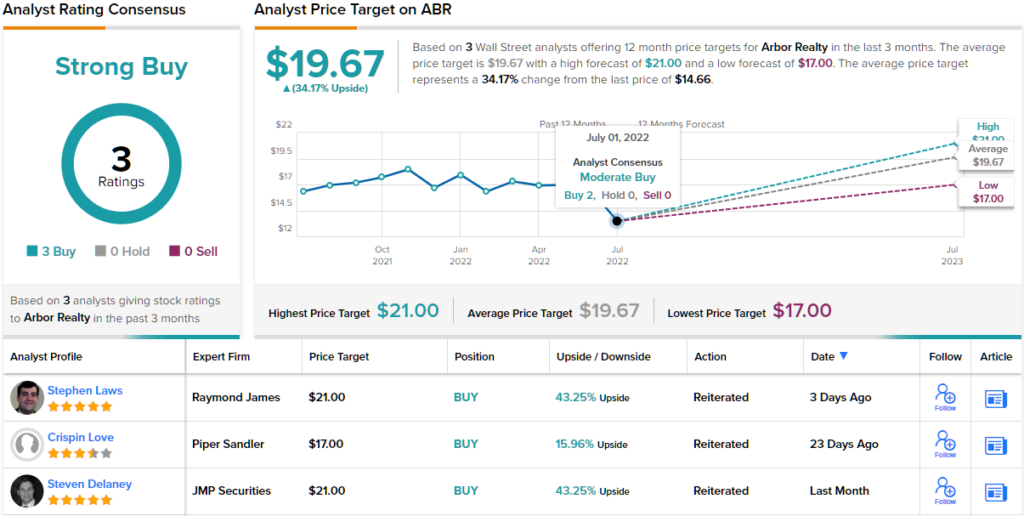

Arbor Realty Trust (ABR)

We’ll start in the real estate sector, with Arbor Realty Trust. This company focuses on providing funding for developers of multifamily residences, which, with commercial properties, make up the bulk of Arbor’s business. Arbor also works with Fannie Mae and Freddie Mac on loan funding.

Even though the real estate market is stating to cool off – an effect of high inflation and rising interest rates – Arbor can fall back on recent solid financial performances. In the most recent reported quarter, for 1Q22, the company beat the earnings forecast by a wide margin. EPS came in at 55 cents, well above the 45-cent estimates. The gains in earnings were driven by a 17% portfolio growth.

Sound earnings have allowed Arbor to not just maintain a reliable dividend over an extended period of time, but to increase it, making ABR one of the market’s best dividend stocks. The company has raised its common share dividend payment in each of the last 8 consecutive quarters – and over that time, the increases have added up to a 27% increase in the dividend payment. The current payout is set at 38 cents per common share, which annualizes to $1.58 and gives a yield of 10.2%. That is a 1.1% higher than June’s 9.1% inflation rate – an important point for investors to consider.

Analyst Crispin Love, writing from Piper Sandler, describes Arbor as a ‘rock solid’ dividend payer, and writes of the stock: “Arbor is the key player where we have the most conviction in its current dividend as well as increases over the next several quarters to go along with eight consecutive increases from 3Q20 to 2Q22. In addition to the increases, ABR has handily covered the divided with distributable earnings, has among the lowest payout ratios in the industry at 70%, and has a diversified model and scale to weather uncertainty in the economy.”

At the bottom line, Love says, “We are confident that ABR will sustain its dividend even if we were to dip into a recession.”

These are not the comments of an analyst who has any doubts, and Love gives Arbor an Overweight (i.e. Buy) rating, with a $17 price target that suggests an upside of 15.5% in the next 12 months. Based on the current dividend yield and the expected price appreciation, the stock has ~26% potential total return profile. (To watch Love’s track record, click here)

Overall, Arbor get a unanimous thumbs up from the analyst consensus, with 3 recent Buy reviews adding up to a Strong Buy rating. The shares are selling for $14.69 and their average price target of $19.67 is even more bullish than Love would allow, implying a 34% one-year upside. (See Arbor stock forecast on TipRanks)

New Residential Investment (NRZ)

Sticking with the real estate investment trusts, or REITs, we’ll turn now to New Residential. This REIT is deeply involved in the market for residential properties and mortgage loans, and has an investment portfolio that exceeds $7.4 billion. The largest part of this comes from mortgage services, the second largest is MSR related investments, and the third largest is loan origination. Together, these segments make up 74% of the company’s total portfolio.

And that portfolio has been profitable for the company. Diluted GAAP EPS grew substantially quarter-over-quarter, from 33 cents in 4Q21 to $1.37 in 1Q22. In total terms, that was increase from $160.4 million to $661.9 million. Core earnings for the quarter came to 37 cents per share, based on a total of $177.4 million. New Residential also reported having $1.67 billion in cash and liquid assets at the end of the first quarter, and important asset for the company to fall back on should the real estate market turn south.

In an interesting note, in June, the company announced that it has entered agreements to convert to an internally managed REIT, a move which the company estimates will save $60 million to $65 million per year, or 12 cents to 13 cents per share going forward. Right now, the move will cost the company $400 million in management termination fees, payable in three tranches over the remainder of this year. Along with the conversion to internal management, New Residential will rebrand itself as Rithm Capital, with a new ticker RITM to take effect on August 2.

For now, investors should remember that the company’s cash holdings earnings and cash holdings are effectively guaranteeing the dividend. The current payment is 25 cents per common share, which makes 1Q22 the fourth quarter in a row that the dividend has been declared at this rate. The key point of the dividend, however, is the yield. At $1 per common share, the dividend is currently yielding 10%.

RBC Capital 5-star analyst Kenneth Lee has reviewed this stock in detail, and his take on it, for now, is that the internal management conversion and rebranding will come to a net positive. Lee writes, “We think many investors generally view internally-managed structures as potentially having much stronger alignment of interests between management and shareholders than externally-managed structures.”

Going on, Lee adds, “Looking further out, the rebranding of NRZ as Rithm Capital reflects ongoing diversification of NRZ’s business model and investment portfolio such that it is not just a residential-focused mortgage REIT. Management indicated there are plenty of attractive opportunities, and NRZ has $1.6bn of cash and available liquidity on balance sheet.”

With an outlook like that, it should be no surprise that Lee sides with the bulls on this stock. His comments come with an Outperform (i.e. Buy) rating, and a $13 price target that indicates potential for 30% share growth on the one-year time horizon. (To watch Lee’s track record, click here)

All in all, this stock has picked up 5 analyst reviews lately, with 4 saying Buy and 1 saying Sell, giving NRZ a Moderate Buy consensus rating. The average price target of $12.65 suggests ~27% upside from the current trading price of $9.98. (See NRZ stock forecast on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.