It would be easy to think that data storage leader Seagate (NASDAQ:STX) would be largely insulated from an economic downturn. However, with Seagate down today, that doesn’t seem to be the case at all. Especially after a drop in Tuesday’s trading. While Seagate had some good news for investors with a new deal, its revised outlook proved much less confidence-inspiring. The good news for investors was that Climb Channel Solutions announced plans to bring Seagate’s Lyve Cloud system to its channel community.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

That would improve cloud storage capabilities by offering a tool that required no “…egress fees, API calls, and vendor lock-ins.”

However, this news was largely overshadowed by word that the company was revising its outlook for its fiscal first quarter. Previously, Seagate looked for first-quarter revenue to come in between $2.35 billion and $2.65 billion. Now, Seagate looks for revenue between $2 billion and $2.2 billion.

The last 12 months for Seagate shares started off well but couldn’t sustain the gains. This time last year, Seagate shares were up around $84 per share. By January 3, 2022, they reached just over $114. That started a series of drops and rallies for Seagate shares that ultimately sent them down to their current levels, around $66 per share.

The good news at Seagate is indeed pretty good, but it’s the bad news that’s likely to get more attention at this point. Previously, I was cautiously bullish about Seagate’s chances going forward. However, with the new information that’s emerged, I’m pulling back to neutral.

Investor Sentiment is Looking Up for Seagate Stock

While Seagate’s revised earnings projections may leave investors unnerved, there are signs that the company enjoys very positive investor sentiment right now. Seagate currently has a Smart Score on TipRanks of 8 out of 10. That’s the lowest level of “outperform,” which suggests a solid likelihood that Seagate will ultimately do better than the broader market.

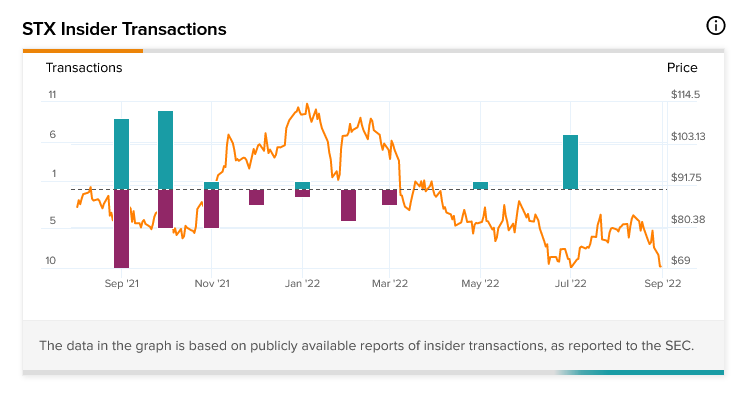

That sentiment is hardly alone, as Seagate insider trading is clearly buy-weighted for 2022. While the buys aren’t informative buys, the aggregate totals suggest that Seagate insiders are looking for gains to come.

In fact, in the last three months, all Seagate insider trading has been buying activity. For the last three months, there have been seven buy transactions and no sell transactions.

The last time a sell transaction was seen at Seagate was back in February 2022. Buy transactions and sell transactions proved perfectly matched over the past 12 months. Each type of transaction took place 29 times. The latter half of 2021 featured a lot of sell traffic, which was made up for after the company lost a significant portion of its value.

Macroeconomic Issues Proving Too Much for Seagate Stock

It seems clear at this stage that Seagate is going to take a hit from the declining overall market. There are virtually no companies that are completely immune to macroeconomic conditions; someone, somewhere, will reduce spending on just about everything when the economy turns down overall.

A few months ago, when discussing the company, I noted that Seagate had multiple potential applications. A company with a diversified product portfolio with plenty of use cases should be fairly well insulated against economic downturn. Certainly, it should hit, but it wouldn’t hit as hard as a company that tended to focus on one niche.

Seagate’s expansion efforts into data center operations, along with virtual reality and other efforts, were likely to prove beneficial. Indeed, this is the second time in recent months we’ve heard about progress from Seagate Lyve; previously, it started working with Atempo’s Miria system. Now, it’s also working with Climb Channel.

While Seagate has done well to protect itself against a downturn, it won’t stop the impact entirely. Worse, some of the issues are even beyond Seagate’s control. CEO Dave Mosely described disastrous conditions where just about everything that could go wrong did. Buyers were pulling back, and supply chains were still having trouble with delivery.

Thus, the company is actively working to reduce its output and save costs in the meantime. That will inherently limit its ability to make sales and, from there, revenue, which likely explains the cuts to projections.

Is STX Stock a Buy?

Turning to Wall Street, Seagate has a Hold consensus rating. That’s based on six Buys, 14 Holds, and one Sell assigned in the past three months. The average Seagate price target of $85.11 implies 27% upside potential. Analyst price targets range from a low of $58 per share to a high of $120 per share.

Conclusion: STX Stock is a Tempting but Dangerous Play

Seagate is a tempting prospect. It’s trading down around its 52-week lows. That puts it much closer to the lower price targets than the average price target and makes for a solid buy-in point. Plus, Seagate also has a solid position in the data storage market. That’s a very substantial market to be part of. However, the macroeconomic conditions right now are going to cause some trouble for Seagate in the short term. The company is already paring back production to accommodate the new conditions.

Granted, new partnerships are taking place, and new buyers are coming in, but they’re going to do so at a slower pace than previously seen.

It’s tempting to buy in on Seagate, but conditions suggest that the company may yet have a little farther to fall before it’s all said and done. That’s why I’m neutral on the company right now; those who already have Seagate shares should keep them.

There’s little risk of catastrophe here, after all; as long as there is data, it will require storage. However, buying in right now may be a step too far; the company’s active reduction in production will hurt it going forward.

Thus, for Seagate right now, the best plan may be to let the worst of the trouble pass by and be ready to come in later.