Is it a good idea to bank on Bank of Nova Scotia (NYSE:BNS) (TSE:BNS) stock? Don’t get too excited about it, even if you’re a value seeker and a passive income investor. Certain key data points indicated that Bank of Nova Scotia (also known as Scotiabank) isn’t growing, so I am neutral on BNS stock.

Confident Investing Starts Here:

- Quickly and easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

Based in Canada, Bank of Nova Scotia has been around since 1832 and serves clients in multiple countries. The company is a giant among financial institutions in Canada, but many U.S.-based stock traders have never thought about Bank of Nova Scotia stock.

Yet, they might happen to come across Bank of Nova Scotia’s essential statistics and take notice of the company’s dividend yield and other facts and figures. It’s important to be aware of Bank of Nova Scotia’s valuation and yield, but don’t get trapped into a trade that you may end up regretting.

BNS Stock: Why It’s Not Such a Terrific Deal

As a habit, investors should dig deeper after browsing through a company’s vital stats. Otherwise, they might miss out on some deal-breaking details. Bank of Nova Scotia is a textbook example of this, as BNS stock isn’t necessarily the great deal that some value hunters probably think it is.

For example, Bank of Nova Scotia has a GAAP trailing 12-month price-to-earnings (P/E) ratio of 10x. This might sound like a great deal. It’s not too bad, but it’s also not far from the sector median P/E ratio of 9.54x. Thus, there are probably other financial sector companies that have more favorable valuation multiples.

Alternatively, we can consider Bank of Nova Scotia’s trailing 12-month price-to-sales (P/S) ratio, which is 2.4x. That’s actually higher than the sector median P/S ratio of 2.34x. The point is that any multiple should be compared to the sector as a whole, and Bank of Nova Scotia stock doesn’t appear to be a spectacular bargain.

For passive income investors, Bank of Nova Scotia does pay a forward annual dividend yield of around 7.4% after the stock’s latest dip, which seems impressive, especially compared to the financial sector average dividend yield of around 2.1%. On the other hand, Bank of Nova Scotia’s payout ratio (the portion of the company’s earnings that are paid out in dividend distributions) is quite high at 71.3%.

Anything over 50% should make prospective investors wonder whether a dividend is sustainable. Hence, Bank of Nova Scotia may end up having to cut its dividend payments at some point.

Bank of Nova Scotia Expects a “Challenging Environment”

Bank of Nova Scotia Chief Risk Officer Phil Thomas recently warned, “We expect a challenging environment will persist for consumers and businesses.” Moreover, the company cautioned that its earnings will increase “marginally” in 2024. These aren’t encouraging signs for prospective shareholders.

Not only that, but Scotiabank’s management stated that its Fiscal Year 2024 earnings would be impacted by “slowing economic growth across its markets and increasing regulatory capital requirements.” Again, investors should wonder whether Bank of Nova Scotia will be able to continue paying a 7.4% annual dividend.

It’s also a bad sign that BNS increased its fourth-quarter provision for credit losses to C$1.26 billion ($927.90 million), compared to C$529 million in the year-earlier period. This suggests that the company’s management expects borrowers to default on their loan obligations.

Turning to Bank of Nova Scotia’s Q4-FY2024 results, the company reported diluted unadjusted earnings per share of C$1.02, compared to C$1.63 in the year-earlier quarter. Meanwhile, adjusted earnings fell from C$2.06 to C$1.26. Additionally, Bank of Nova Scotia’s unadjusted return on equity (ROE) declined from 11.9% in the year-earlier quarter to 7.2% in Fiscal Year 2024’s fourth quarter, while adjusted ROE fell from 15% to 8.9%. Clearly, the company’s financials are far from perfect.

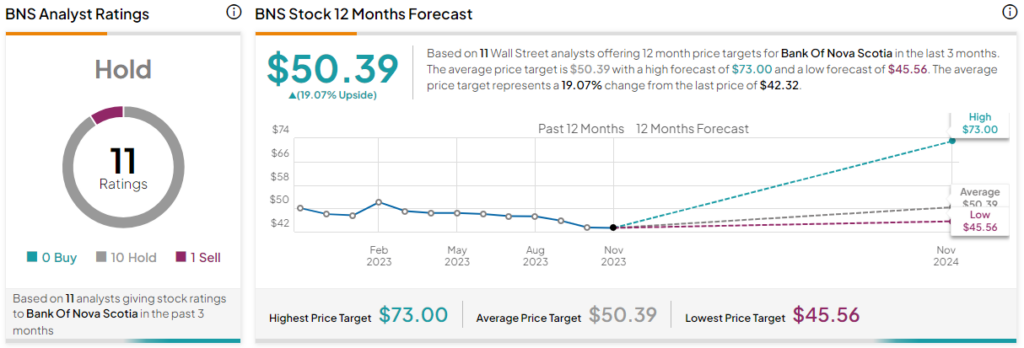

Is BNS Stock a Buy, According to Analysts?

On TipRanks, BNS comes in as a Hold based on zero Buy ratings, 10 Hold ratings, and one Sell rating assigned by analysts in the past three months. The average Bank of Nova Scotia price target is $50.39, implying 19.1% upside potential.

Conclusion: Should You Consider BNS Stock?

If you focus too much on basic data points, you might miss the big picture. So, don’t get trapped into a potentially losing trade by Bank of Nova Scotia’s apparently attractive valuation and dividend yield.

I encourage you to dig deeper and conduct thorough due diligence on Bank of Nova Scotia if you’re thinking about investing in the company now. Even though BNS is a large financial institution that might entice some traders, I’m staying on the sidelines and choosing not to consider BNS stock now.