Roku (ROKU) has been hit by two significant developments which have dampened expectations – supply chain disarray and slowing active accounts. According to Oppenheimer’s Jason Helfstein, the latest on the grapevine is that the outlook for neither over the near-term is very promising.

On the former, recent lockdowns in China have only exacerbated an already struggling supply chain for TVs. “Shipping giant Maersk recently warned Shanghai lockdown will lead to longer delivery times/higher transport costs,” explained Helfstein, who also notes that a quick search on Best Buy reveals that 12% of Hisense/TCL models are out-of-stock.

As for the latter, year-to-date Google search trends paint a disquieting picture; as of March 20, searches for the term Roku TV had the “lowest” 2-year CAGR (0%) since June 2021.

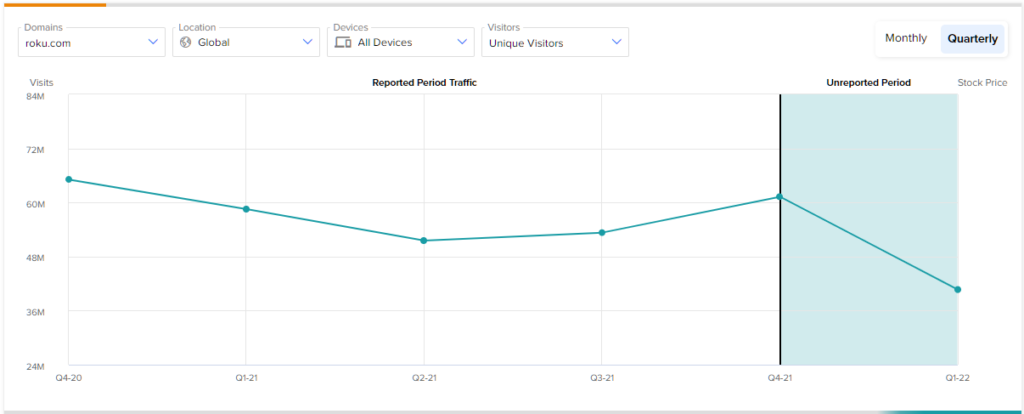

A look at website traffic trends also unsettles. In 1Q22, Unique Visitors (UVs) have dropped by ~34% from 61.28 million to 40.68 million, whilst year-over-year UVs have fallen by over 30%.

So, plenty of bearish developments to mull over. That said, it is not all doom and gloom; while Helfstein remains cautious on 1Q active accounts, considering Europe accounts for less than 5% advertising revenue – well below other CTV plays – the company is still among the “best insulated from European risk.” Additionally, even though the return to work means viewing per user is “normalizing” to 2019 levels, 3P data shows ROKU is now gaining share of viewing time.

Another promising sign is that vs. streaming competitor Netflix, Roku’s valuation is “attractive,” and going by prior times Roku was at such a comparatively low level, what followed should have Roku investors feeling confident.

“Since Jan. ’19, ROKU has traded at a discount to NFLX twice (once from Jan. ’19 to May ’19, and again from Mar. ’20 to June ’20),” Helfstein explained. “Within six months, ROKU outperformed NFLX as EV/GP expanded. Within this context, we view ROKU’s current 45% discount to NFLX as compelling.”

All in all, while Helfstein has tweaked some estimates to account for slowing net adds, the 5-star analyst sticks with an Outperform (i.e., Buy) rating and $185 price target. Should the figure be met, investors are looking at one-year returns of ~37%. (To watch Helfstein’s track record, click here)

At $183.67, the Street’s average price target is only fractionally off Helfstein’s objective. Rating wise, 14 analysts remain in Roku’s corner, and with the addition of 1 Hold and 3 Sells, the stock makes do with a Moderate Buy consensus rating. (See Roku stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.