Is it all coming together for Rivian (NASDAQ:RIVN)? Against a backdrop of seemingly waning EV demand, the company managed to deliver a solid Q3 report that featured beats both on the top and bottom line, while the EV maker also increased its production outlook for the year.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks straight to you inbox with TipRanks' Smart Value Newsletter

With the company having already announced production (16,304) and delivery (15,564) numbers for the quarter, at $1.34 billion, the top-line showed a big 150% year-over-year improvement and beat the forecast by $30 million. Additionally, with the focus on managing costs and making operations more efficient, adj. EBITDA hit a loss of ($942.0) billion, some distance ahead of the Street’s ($1.05) billion estimate. The end result was also a bottom-line beat as adj. EPS of ($1.19), fared much better than Wall Street’s ($1.34) forecast.

Looking ahead as to what’s coming next, Rivian impressed, too. The company now expects to produce 54,000 units this year, up from 52,000 units beforehand. The full-year adj. EBITDA guide improved from ($4.20) billion to ($4.00) billion while capex is now expected to be around $1.10 billion vs. the prior $1.70 billion, as the company’s efforts to balance cost management and its build-out appear to be bearing fruit.

Rivian’s exclusivity agreement with Amazon also came to and end, enabling it to sell commercial vans to other customers. This is a development applauded by Wedbush’s Dan Ives, a 5-star analyst rated in the top 2% of Wall Street’s stock pros.

“With more than 10,000 EDVs (electric delivery vans) on the road, we believe this was a great move for the company as it works to meet its 100k delivery figure to Amazon while also expanding its EDV footprint to other customers,” Ives explained.

Rivian also anticipates a 1-week shutdown in Q4 to get ready for a longer shutdown in 2Q24 so it can bring forth new vehicle technology to the R1 platform. The downtime is expected to affect 2 quarters of production. “Although not ideal,” says Ives, “we believe this is the right long-term decision for the automaker to ultimately reduce costs and improve margins in FY24. With this quarter showing strong potential, we still remain confident in the long-term Rivian story, but will need a few more quarters of this performance and ahead of schedule innovations for the company to regain full credit from the Street.”

Meanwhile, Ives maintained an Outperform (i.e., Buy) rating on RIVN shares, while his $25 price target anticipates shares will rise by 45% in the year ahead. (To watch Ives’ track record, click here)

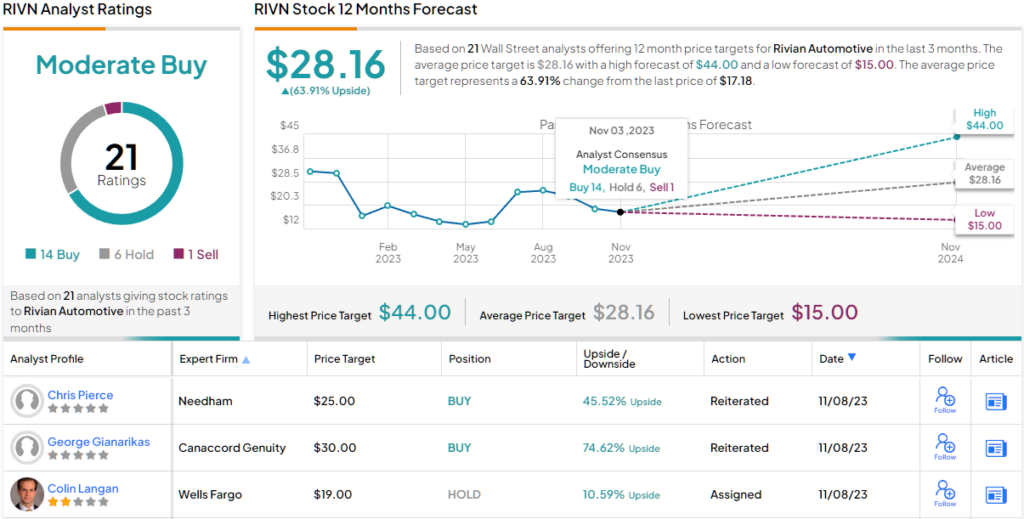

Most on the Street agree with Ives’ prognosis. 13 other analyst reviews slant positive and with the addition of 6 Holds and 1 Sell, the analyst consensus rates the stock a Moderate Buy. The forecast calls for 12-month returns of ~64%, considering the average target stands at $28.16. (See Rivian stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Looking for a trading platform? Check out TipRanks' Best Online Brokers , and find the ideal broker for your trades.

Report an Issue