Years ago, Peter Lynch popularized the concept of “picks and shovels,” noting that most of the miners who joined the Gold Rush to get rich failed to do so, but the people who focused instead on selling picks, shovels, and other supplies to the miners came out far ahead.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

That same concept applies to a lot of industries, including biopharma: pick the right gene therapy up-and-comer and an investor can multiply his or her money several times over, but pick the wrong one and the losses could be significant. Repligen (RGEN), though, will be a winner, as long as the development and use of biological products like antibodies, vaccines, and cell/gene therapies continue to grow.

Core production demand for these types of biological products grew nearly 20% in 2020, excluding the impact of COVID-19, and looks poised for more than a decade of strong growth as biopharma companies and contract manufacturers continue to scale up their production capacity.

Repligen is still a relatively small player in the field compared to companies like Danaher (DHR) and Thermo Fisher (TMO), but management is leveraging a strong foundation in filtration and purification to build an increasingly compelling picks-and-shovels player in a large growth industry.

Capacity Growth Remains Strong

Biological drugs, including antibodies, vaccines, gene therapies, RNAi and antisense therapies, and other cell therapies, already represent more than $200 billion in annual sales for the biopharma industry. Antibody therapies currently make up about 60% of the total and are growing at a low double-digit rate.

On top of that, over half of all drugs in biopharma pipelines today are biologics, and sub-categories like biosimilars (essentially generic versions of antibody therapies), RNAi/antisense, checkpoint inhibitors, and gene therapy have only just gotten started in terms of their significance and contribution to the total market.

Biological drugs require different manufacturing setups, and the effort to ramp up production of new COVID-19 vaccines and therapies has highlighted the existing capacity constraints in the system. Simply put, there isn’t all that much spare capacity in the system, and Samsung Biologics echoed that earlier this year, noting that in January, it was already near full capacity for 2021.

At the same time, Repligen management asserted that the bioproduction market grew roughly 20% in 2020, and other names in the space have discussed similar growth rates. Moreover, this market is not a one-year or short-term phenomenon.

Assuming that clinical success rates for biological drugs in the pipeline today will be broadly similar to others in the past, the industry will need to ramp up manufacturing capacity at a rate of at least mid-teens growth over the next decade.

Building Out Capabilities Across The Board

Historically, Repligen’s strengths have been in filtration and purification, which are crucial steps in the bioproduction chain that represent about 20% to 25% of the addressable market. That said, the company also has meaningful exposure to areas like process analytics and has been growing its portfolio through internal R&D and serial M&A. Currently, the company has little presence in areas like cell culture, fermentation, and fluid management, but these could be areas where management looks to M&A to expand its presence.

For Repligen, filtration grew 60% year-over-year in the last quarter, and the company now has solid low to mid-teens share, with capabilities in both alternative tangential flow (ATF) and tangential flow filtration (TFF).

As for purification, Repligen offers pre-packed chromatography columns with whatever resin the customer wants (Danaher has historically offered only its own resins), and Repligen’s columns are a disposable alternative to stainless steel columns in an industry rapidly converting to single-use devices.

What’s more, Repligen has remained quite active on the M&A front, recently acquiring ARTeSYN, NMS, and EMT. The latter two are somewhat less dramatic deals, adding internal capabilities for single-use products like silicone assemblies and components (like flow paths/tubing) and fabricated plastic containers and assemblies. ARTeSYN, though, brings in automation and integration capabilities, allowing Repligen to offer filtration, chromatography, and buffer/media prep in single-use systems.

The company has also been focusing on building up its presence in the gene therapy market. It added more gene therapy customers in 2020 (10 to 15), and now generates around 15% of its revenue from this fast-growing sub-sector of the market.

The Opportunity

Repligen is targeting $1 billion in revenue in 2025 and has a good chance of getting there. Even as the benefit from accelerated COVID-19-related spending fades (22% of Q4’20 revenue and likely to add 12% to 15% incrementally in 2021), underlying growth will still be in the mid-to-high teens. Repligen should continue to gain share on the back of its strong offerings in filtration, purification, and analytics, including a new FlowVPE system that measures protein concentrations on production lines in real time.

Longer term, 20% annualized revenue growth is possible, pushing Repligen to over $1 billion in revenue in 2025 and around $2.4 billion in revenue in 2030. The company is already free cash flow positive and can generate free cash flow margins in the mid-to-high 20%’s on revenue of $1 billion-plus.

Wall Street’s Take

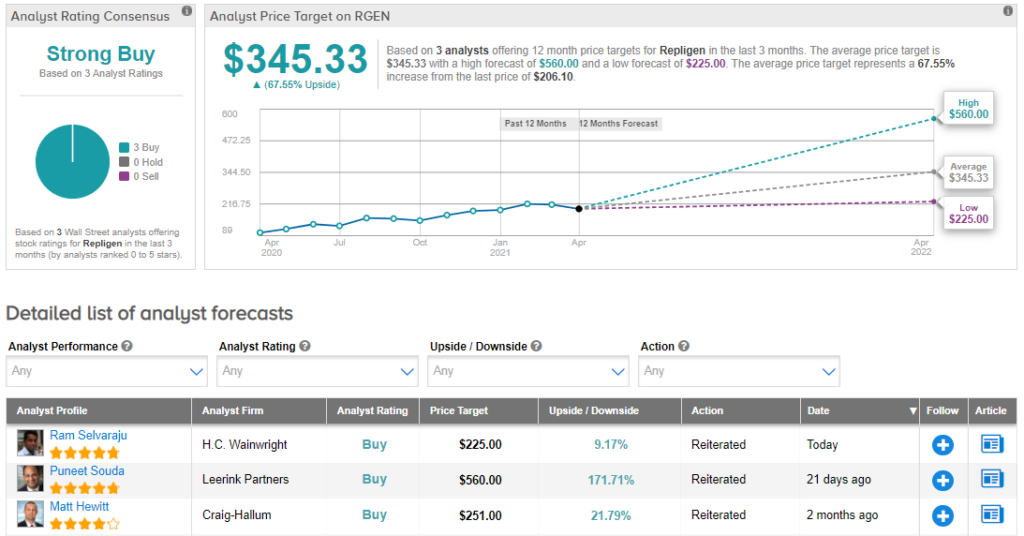

Turning to the analyst community, RGEN is a Strong Buy, based on 3 unanimous Buy ratings assigned in the last three months. Given the $345.33 average analyst price target, shares could gain 68% in the year ahead. (See Repligen stock analysis on TipRanks)

The Bottom Line

Repligen is not conventionally cheap, but the valuation is not out of line with other high-growth life sciences and bioproduction stocks. It is not uncommon to see these stocks trading at EV/revenue multiples which are roughly in line with expected three to five-year revenue growth rates.

Still, this is very much a growth stock and priced accordingly, and it may not be suitable for more conservative or value-oriented investors. Having said that, its strong leverage to biological manufacturing capacity investment growth and market share growth potential may be appealing to growth investors.