In a recent note on the state of the stock markets, Raymond James equity strategist Tavis McCourt points out a series of policy factors that are playing a role in the current market volatility; the situation is more complex, perhaps, than most of us have been willing to admit. McCourt notes permutations of the SLR rule, political dynamics on the Senate Banking Committee, and the regulatory atmosphere towards potential capital return are all influencing the Fed’s moves and the market reactions.

“We believe the Fed will do everything they can to ensure orderly trading in US Treasuries and does not want to see the volatility and liquidity concerns that have occurred in the last week/over the course of the pandemic. We also believe that the Fed is not interested in having a spike in yields as Treasury seeks to finance the next round of stimulus,” McCourt opined.

The strategist added, “While the SLR conversation is a political and market issue for the Fed, we believe that any Treasury and/or equity market sell-off tied to the debate is transitory and overblown. We are more focused on the improving economic environment, vaccine distribution, and reflation.”

Bearing this in mind, our focus turned to three stocks backed by Raymond James, with the firm’s analysts noting that each could soar over 50% from current levels. Running the tickers through TipRanks’ database, we found out that the rest of the Street is also on board, as each boasts a Moderate or Strong Buy consensus rating.

Orasure Technologies (OSUR)

We’ll start in the medical industry, a field that has seen gains through the pandemic year. Orasure, through its subsidiaries, is a producer of medical diagnostic tests, and is known for developing rapid test kits for HIV, HEP-C, and Ebola. In the past year, the company created over 150 jobs at its Bethlehem, Pennsylvania facilities as part of an effort to develop fast, at-home, COVID test kits. The company’s product line has a wide range of uses, and is marketed to clinical labs, hospitals, physician practices, and public health agencies world-wide.

As can be imagined, Orasure has seen a quick recovery from a 1H20 revenue dip followed by strong gains. Q4 top-line revenues hit $62.9 million, for a 27% year-over-year gain. This was driven by product and services revenues, which grew 28% to reach $60.4 million. EPS was positive, at 3 cents per share, which was a good turnaround from negative results in the first half of the year – but was down 25% from 4Q19.

For the full year, Orasure reported $172 million in net revenues, an 11% yoy gain. Of this total, $50 million came from sales of oral fluid collection devices (mouth swabs) for COVID-19 test kits. In addition, the company reported continued progress on its COVID-19 rapid antigen test, and plans to submit prescription self-tests and professional-grade tests for EUA (Emergency Use Authorization) by the FDA by the end of the first quarter.

Analyst Andrew Cooper, in his coverage on the stock for Raymond James, saw plenty to like, ticking off the factors by the numbers: “What we liked: 1) Almost every revenue result. Orasure topped consensus sales estimates by 10%… 2) Concrete antigen EUA submission timeline. There is no misunderstanding an expected submission this month, with studies completed and only more administrative type work remaining… 3) More capacity expansion. Existing capacity timelines are on track, but management now intends to add another 50M of annual antigen capacity…”

To this end, Cooper puts a $16 price target on the stock, implying a 52% one-year upside, and rates OSUR an Outperform (i.e. Buy). (To watch Cooper’s track record, click here)

A solid reputation in the field, and clear path forward are sure to attract positive sentiment – and three Wall Street analysts have put Buy ratings on Orasure, making the analyst consensus a Strong Buy. Shares are priced at $10.49, and the $18.67 average price target is even more bullish than Coopers, suggesting a 78% upside for the next 12 months. (See OSUR stock analysis on TipRanks)

Sol-Gel Technologies (SLGL)

Sticking to the medical field, we’ll switch focus to a clinical stage pharmaceutical company. Sol-Gel is a biopharma with an interesting niche, developing topical medications for the treatment of skin diseases.

The company’s pipeline includes two proprietary formulations based on benzoyl peroxide, both creams: Epsolay, which is a treatment for papulopustular rosacea, and Twyneo, a treatment for acne. Both medications had their NDAs (New Drug Applications) filed with the FDA, and final approval decision is expected in April and August of this year, respectively.

Sol-Gel has, in addition, three other drug candidates in early stages of the pipeline process. Two are still in the research phase, while SGT-210 is in Phase I trial, with results due in 1H21. SGT-210 is a potential treatment for palmoplantar keratoderma, a thickening of the skin on the palms of the hands and feet which is sometimes seen as a symptom of several rare conditions.

Furthermore, Sol-Gel is working in collaboration with Perrigo as the US manufacturer of generic labels of that company’s brand-name products. In 2020, the two companies signed four agreements, and now have 12 total collaboration projects.

Among the fans is Raymond James analyst Elliot Wilbur who writes, “Given the large market opportunity in key pipeline products, coupled with recent acceptance of NDA submissions, we maintain our Strong Buy rating on SLGL shares, as we remain optimistic surrounding near-term growth prospects and financial positioning.”

The Strong Buy rating comes with a $23 price target, suggesting SLGL has room to grow an impressive 156% in the year ahead. (To watch Wilbur’s track record, click here)

Small-cap biopharmas don’t always get a lot of analyst attention – they tend to fly under the radar. However, there are two reviews on file here and both are to Buy, making the consensus rating a Moderate Buy. SLGL shares are priced at $9, with an average price target of $22 indicating a runway toward ~145% upside for 2021. (See SLGL stock analysis on TipRanks)

PAE (PAE)

Let’s switch gears, and look at government support services. It’s no secret that governments are huge users of contract service companies, and PAE is a major provider of contract services for US government and defense agencies. PAE has operations on every continent and in 60 countries, providing a range of services, including analysis and training, intelligence, infrastructure operations, management and maintenance, logistic and material support, and information optimization.

Until recently, PAE was a privately held company, but in February last year it was merged with Gores Holdings III in a SPAC transaction. The transaction brought PAE shares onto the NASDAQ exchange on February 10, 2020.

2021 has started with some changes in PAE’s contracts with the US government. At the end of January, the company lost a bid to renew a $125 million contract it had held with Customs and Border Patrol since 2009 – but earlier that same month, PAE was awarded a $3.3. billion contract with the US State Department. The contract with State involve consular operations at diplomatic facilities in 120 countries.

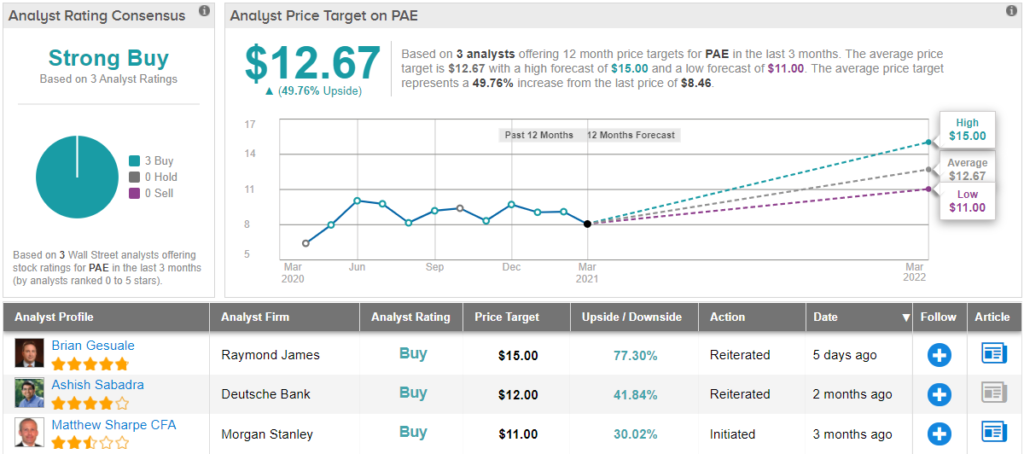

5-star analyst Brian Gesuale, in his coverage of PAE for Raymond James, notes the change in contracts, and does not believe it should trouble PAE.

“PAE’s qualified pipeline still sits around $40B and pending awards north of $6B, which when combined with the company’s 2020 recompete win rate of 93% provides us confidence that CBP contract can be adequately replaced,” Gesuale commented.

Turning to specifics on the State contract, Gesuale adds, “…this contract win could add upwards to $110 to $125 million of high-margin annual revenue to the 2022 model. Overall our estimates are going higher, and we continue to view PAE as one of the more compelling opportunities in the Government IT Services space. While we expect the group will face decelerating fundamentals and a potentially meaningful re-rating lower from near historically high valuations PAE should fare differently as it accelerates organic growth…”

In line with these comments, the analyst puts an Outperform (i.e. Buy) rating on the stock, and his $15 price target implies a 77% one-year upside. (To watch Gesuale’s track record, click here)

PAE stock has a resounding “yes” on Wall Street. TipRanks analytics show that out of 3 analysts, all 3 are bullish. The average price target of $12.67 shows a potential upside of about 50%. (See PAE stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.