The past month has been volatile for tech stocks, but Qualcomm (QCOM) has been able to buck the trend. Since early March, shares have gone from $123 to around $136, bringing the market cap to $154.8 billion.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

That said, this probably won’t be the end of the gains. Qualcomm is one of the best positioned tech companies to benefit from the 5G megatrend.

This technology has been in the works for some time, but it is still in the early phases of the rollout. And yes, 5G will be transformative. Compared to 4G, the speeds are as much as 100 times faster. This means much less latency, which will allow for better cloud solutions, video experiences and AI models.

Augmented Reality (AR) and Virtual Reality (VR) will also likely see adoption increase. According to a research report from Ericsson (ERIC), the coverage for 5G will reach about 60% of the world’s population and the number of mobile subscriptions will be roughly 3.5 billion by 2026.

Qualcomm Has Solid Standing In The Space

As for Qualcomm, the company has the benefit of more than three decades of experience in developing standards for advanced communications systems, such as its CDMA (code-division multiple access) technology.

The result is that it has one of the most valuable set of patent portfolios. As a testament to this, Apple had little choice but to abandon its massive lawsuit against Qualcomm because it needed the IP (intellectual property) for 5G.

So far, Qualcomm has more than 120 5G license agreements, which will bring in large amounts of high-margin revenues for years to come. It also helps that the company has a myriad of solutions for its Snapdragon platform, such as next-generation basebands and sophisticated RF front-ends. In fact, in just a few years, Qualcomm has turned into one of the world’s largest suppliers of RF systems.

Acquisitions will also play a critical role with the strategy. For example, Qualcomm recently shelled out $1.4 billion for NUVIA, with the deal providing significant improvements in performance and energy efficiency for 5G computing.

Yet the 5G opportunity will go well beyond the upgrade of smartphones. The technology will be essential for enterprises, such as smart factories, IoT (Internet-of-Things), self-driving cars, robotics and advanced AI applications. It should be noted that Qualcomm’s technology is currently embedded in over 150 million vehicles across the globe.

There’s another interesting catalyst: Biden’s proposed $2.3 billion infrastructure plan. Consider that about $100 billion will go towards providing high-speed broadband to all Americans. No doubt, this will drive an acceleration of demand for 5G systems from Qualcomm.

Conclusion

Qualcomm stock is certainly not without its risks. The shortage of semiconductors is a nagging issue, especially since the company relies on third-parties for production.

However, this may be more of a short-term problem. With the COVID-19 pandemic fading, the supply chains and production capabilities should improve. The Biden Administration is also focused on spending substantial amounts on building more chip capacity in the U.S.

In the meantime, the valuation for Qualcomm stock remains fairly reasonable. Consider that the forward price-to-earnings ratio is 16.87 and there is even a decent dividend yield of 1.9%.

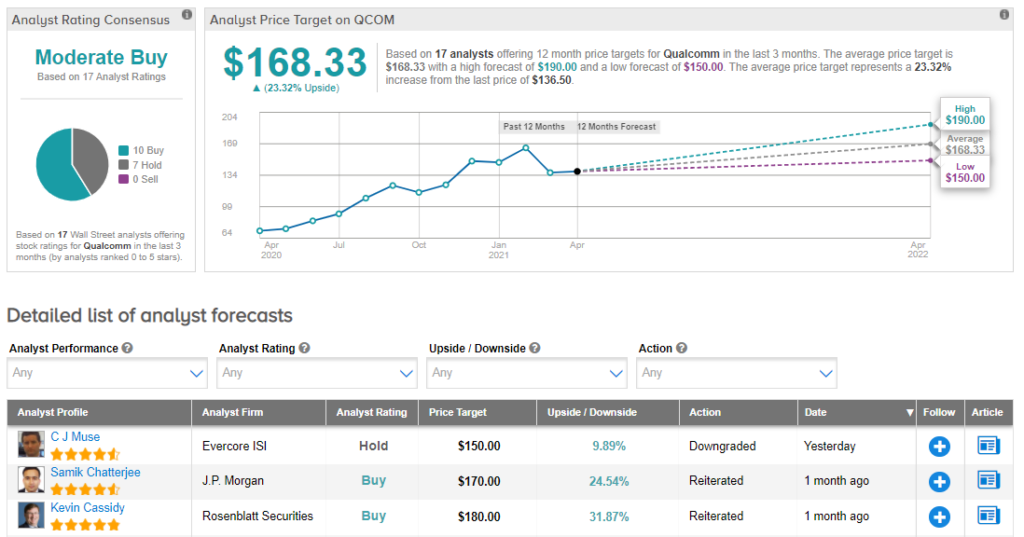

Wall Street analysts are also upbeat on the company’s prospects. According to TipRanks, the average analyst price target is $168.33, which implies 23% upside potential from current levels. Additionally, the Moderate Buy consensus rating breaks down into 10 Buys and 7 Holds. (See Qualcomm stock analysis on TipRanks)

So when it comes to a 5G play – as well as a play on other important technologies – Qualcomm stock definitely looks attractive now.

Disclosure: Tom Taulli had a long position in Qualcomm stock at the time of publication.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.