Qualcomm (QCOM) investors have several worrying macro developments to contend with right now. These include weak 5G smartphone trends and new Covid-19 lockdowns in China which are impacting smartphone production over the near-term.

Yet ahead of the chip giant’s FQ2 earnings on Wednesday, brushing these developments aside, Canaccord analyst Michael Walkley is expecting the company to deliver the goods.

“Based on Qualcomm’s content share gains in higher-end Android smartphones and broad-based strength across the entire QCT portfolio, we anticipate solid Q2/F2022 results and F2022 outlook despite some growing macro headwinds and investor concerns,” the 5-star analyst said.

Handset revenue showed a 41% year-over-year uptick in FQ1 and Walkley believes it will probably be up by even more in FQ2, but further down the line, as industry “supply-demand dynamics” reset to more normalized levels and handsets pull back to “slower growth trends,” the analyst expects other parts of the business to pick up the slack and grow faster in FQ3.

And looking ahead to F2023 and beyond, Walkley expects Qualcomm will benefit as 5G smartphones “ramp,” the company’s mix of 5G increases with 50% more content compared to 4G smartphones, and the RF business grows. Additionally, the “strong trends” in IoT and automotive will supplement the overall uptick in revenue and “contribute to expanding margins.”

As management has said smartphones have been a priority during the first half of F2022, Walkley expects 2HF2022 estimates will be positively impacted from the “strong backlog for the margin accretive IoT and automotive businesses.”

Walkley is bullish not only on 5G and its positive implications for the QCT segment but sees a $10 billion SAM opportunity in Android smartphones as the company takes market share from Huawei. Additionally, anticipating “sustained higher margin trends,” Walkley sees no reason to change his current F2022 and F2023 estimates despite the current headwinds.

More in the here and now, Walkley believes the company’s FQ2 results will at least meet Qualcomm’s guidance for revenue of $10.6 billion and non-GAAP EPS of $2.90 at the midpoint.

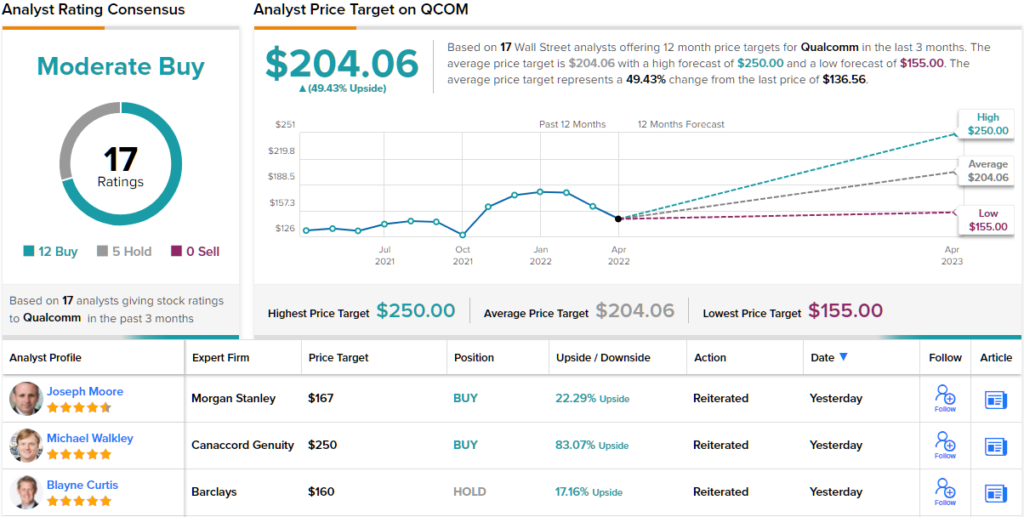

So, promising for Qualcomm, but what does it all mean for investors? Walkley rates QCOM stock a Buy, while his $250 price target makes room for 12-month growth of ~83%. (To watch Walkley’s track record, click here)

Looking at the consensus breakdown, with 12 Buys and 5 Holds, the analysts rate this stock a Moderate Buy. Given the average price target clocks in at $204.06, shares are anticipated to appreciate ~49% in the year ahead. (See Qualcomm stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Questions or Comments about the article? Write to editor@tipranks.com