Pool Corporation (POOL) is the largest distributor of pool supplies in the United States. The stock has gained 34.5% year-to-date, yet is often overlooked by retail investors.

This is due to the company’s less-than-glamorous business model, but its high-quality fundamentals set it up for a bull run. I am bullish on the stock. (See POOL stock charts on TipRanks)

Force to be Reckoned with

Pool’s cost-leadership, and various product differentiation strategies, have allowed it to sustain its position as the market leader in the United States. The Return on Invested Capital metric is often used to measure competitive advantage; Pool’s ratio of 50.63% speaks volumes, exceeding the market average by eight times, ending any debate regarding its competitive advantage.

The company has a clever expansion strategy. It will typically open up shops in hypergrowth environments, and close down shops when geographic areas are experiencing slower growth.

In addition, the company expands through acquisitions. In 2020, Pool acquired Jet Line Products and Northeastern Swimming Pool Distributors. Jet Line owned nine distribution centers in Texas and South Florida. NorthEastern taps into the Canadian market, as it’s currently the second-largest distributor of pool equipment and chemicals in the country.

Constant Earnings Improvements

Analysts’ revenue expectations were beaten by $60 million in the company’s second quarter, while GAAP earnings per share beat estimates by $0.93. The company experienced a 40% growth in revenue year-over-year, and its operating margins increased by 280 basis points.

A driving force behind the better operating margins has been improvements in inventory management, and lower administrative costs overall. Pool’s operating margin trajectory has been trending upwards for the past decade; the improvement in margins should thus not be a surprise.

Providing Excellent Value to Shareholders

Pool Corp values its shareholders highly. The company has made it a priority to compensate shareholders since the turn of the millennium. Constant share buybacks have ensured that the stock price continues to improve, and continuous dividend increases in recent times have added to the optimism.

As of May 2021, Pool had made an additional $450 million available for share repurchases, which will surely be significant to the stock price.

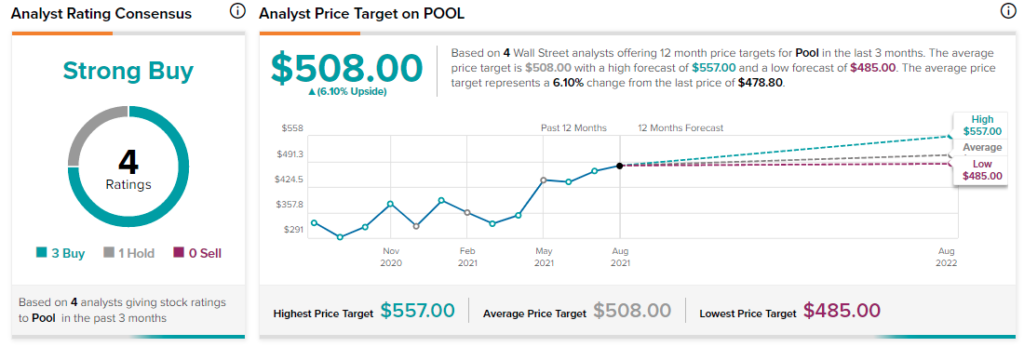

Wall Street’s Take

Wall Street consensus is that Pool Corp is a Strong Buy, with three Buys and one Hold assigned in the past three months. The average POOL price target of $508 implies 6.1% upside potential.

Bottom Line

I think the stock is very underrated, considering its market position, linear improvement in operating margins, and stock buyback program.

Wall Street’s price targets will surely become more bullish with time.

Disclosure: On the date of publication, Steve Gray Booyens had a position in Pool Corporation.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.