Just how high can Pluristem Therapeutics (PSTI) climb? The Israeli biotech has outperformed in 2020, with shares up by 94% year-to-date. Driving the micro-cap’s forward charge has been a familiar 2020 narrative. The company’s PLX-PAD cell therapy, which uses allogeneic mesenchymal-like cells with immunomodulatory properties, has shown promising early results as a possible treatment for COVID-19.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

However, Jefferies analyst Chris Howerton’s bullish thesis for PSTI rests on the PLX-PAD program’s potential as a therapy for an entirely different indication.

“PLX-PAD could be the first approved therapeutic in critical limb ischemia (CLI), which has massive unmet need (~2 million-plus US patients; $1 billion-plus potential, peak unadjusted sales),” Howerton said.

Critical limb ischemia occurs when blood flow to the limb is reduced, affecting the wound’s ability to heal. The mortality rate stands at 20% for the year following diagnosis.

The current standard of care involves revascularization surgery, but only 65% of patients are eligible for surgery, and amputation is often required. Additionally, at $75,000 per year, treatment is incredibly expensive. “In short, there are no viable medications for these patients, the SOC is often ineffective and expensive, and millions of individuals would benefit from an effective drug therapy,” Howerton said.

Currently, clinical data is limited, but a Phase 3 study is in progress in the US, Europe and Israel, with interim data expected in the fourth quarter (approvable data will be available in late 2021).

Although Howerton believes the primary endpoint of amputation free survival (AFS) will be difficult to achieve, the analyst argues “preclinical evidence for PLX-PAD and other cellular therapies is convincing, and the Phase 3 trial is among the largest in the CLI literature to-date.”

Howerton further stated, “PSTI has an extensive pipeline, however, key to its success is the Phase 3 readout in CLI. Even without credit for the Co’s broad pipeline and modest commercial projections relative to the long-term potential of the CLI indication – we would expect substantial upside from a successful Phase 3. We assign a 25% PoS for their Phase 3 CLI program…”

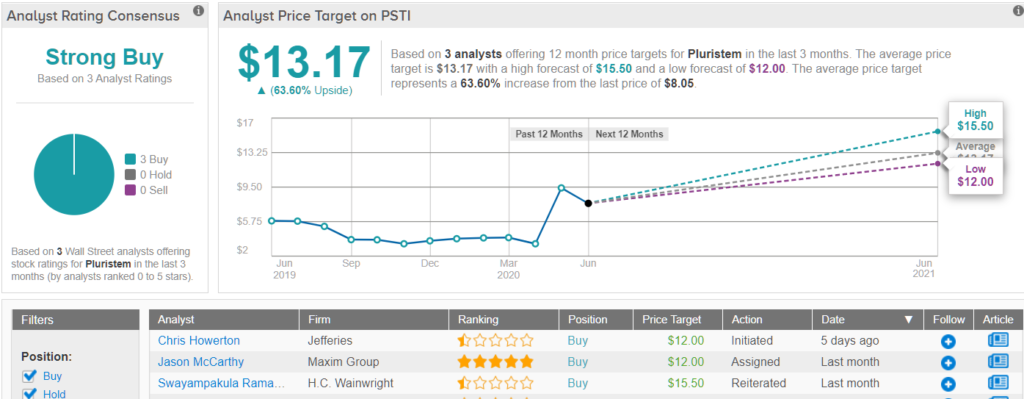

To this end, Howerton initiated coverage with a Buy rating and $12 price target. Investors stand to take home a 50% gain, should Howerton’s thesis play out over the next year. (To watch Howerton’s track record, click here)

The Street remains relatively quiet on the biotech, although all three analysts that have reviewed the stock over the last few months recommend a Buy. PSTI’s Strong Buy consensus rating is accompanied by a $13.17 average price target, implying upside potential of a plentiful 64%. (See Pluristem stock-price forecast on TipRanks)

To find good ideas for biotech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.