Plug Power’s (PLUG) stock price has experienced a catastrophic decline over the past few years. While revenues have surged due to growing demand for hydrogen infrastructure and advancements in the burgeoning alternative fuel sector, the company’s widening losses have eroded shareholder equity significantly. As a green hydrogen solutions developer, PLUG is currently the world’s largest buyer of liquid hydrogen, having installed over 69,000 fuel cell systems and more than 250 fueling stations.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Positive factors, such as expanded electrolyzer deployments and partnerships in Europe and North America, have fueled topline growth. However, with no concrete plan to stem its financial bleeding, Plug Power has relied on debt and shareholder dilution to sustain operations. Given that this trend will likely persist, I am very bearish on PLUG in the short, medium, and long term.

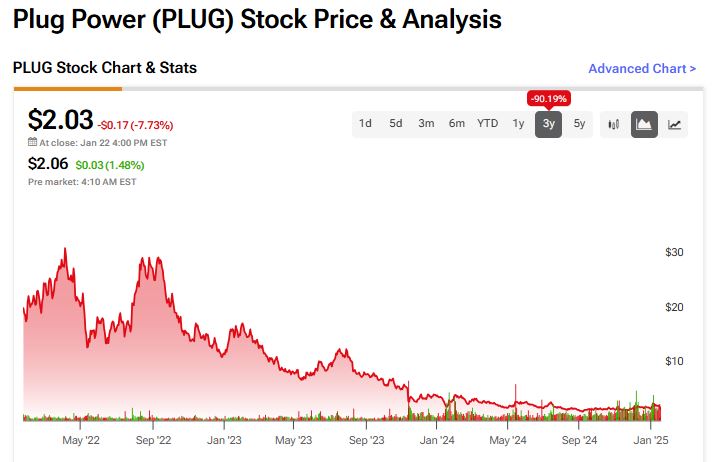

PLUG shareholders have suffered immensely as the stock cascaded 90% lower since 2022.

Why is PLUG Stock So Low Despite Strong Revenue Growth?

At first glance, Plug Power’s revenues have grown quickly in recent years. And yet, its losses have widened even more significantly, which, as any accountant knows, is unsustainable. For context, Plug Power recorded $891.3 million in revenue in 2023, marking a notable jump from $701.4 million in 2022. This increase was powered by advances in the company’s hydrogen fuel cell technology and promising partnerships with Amazon (AMZN) and Walmart (WMT). But sadly, its operating losses more than doubled from $679.6 million to $1.34 billion year-over-year.

The severe multi-year downtrend has become synonymous with the company. As you can imagine, Plug Power aggressively raised capital through debt and share issuance to keep funding its ballooning losses. How costly this has been to PLUG shareholders cannot be stressed enough. Plug Power’s outstanding shares currently stand at 911.2 million, up from 595 million in 2023, 580 million in 2022, and 558 million in 2021. The pace of share issuance (and dilution) is frightening for seasoned investors.

If that wasn’t worrisome enough, Plug Power’s total debt has reached $928.6 million, which, besides eroding shareholder equity, further pressures its profitability due to interest expenses, resulting in additional outflows.

Debt and Dilution Sink Plug Power’s Prospects

Plug Power’s Q3 2024 results reminded investors of the company’s deteriorating trajectory. The company reported declining revenues from $199 million to $174 million in the previous year due to weaker equipment sales and reduced customer demand. So not only is PLUG hemorrhaging cash consistently, but its once-surging revenues are no longer there to preserve the little investor sentiment that remains.

Although management tried to rein in operating expenses, the revenue decline raised red flags. Also, efforts to optimize the hydrogen production process and reduce costs in its electrolyzer business showed limited impact. In simple terms, high fixed costs and declining economies of scale further raised worries regarding Plug Power’s bottom line.

PLUG Shareholder Value Decimated

Looking ahead, I struggle to see how Plug Power could stage a U-turn to reverse its loss-making course. The company expects its revenue to rebound to approximately $270 million in Q4 2024, thanks to expected growth in its electrolyzer and hydrogen production businesses. However, Wall Street analysts still project an EPS of -$0.23 for the quarter, reinforcing the long-term trend of unprofitability and gaping losses. It’s also striking that consensus estimates suggest that Plug Power will remain unprofitable until at least 2030, probably requiring further capital raising and diluting existing shareholder value further.

Put simply, investors shouldn’t expect balance sheet deterioration to end anytime soon. To fund its sprawling losses, PLUG’s management has leaned heavily on stock-based compensation and typical equity issuances, further diluting shareholders. In fact, I believe that dilution will accelerate over the medium term as creditors back away from lending capital to PLUG. The ones that do lend PLUG capital will demand higher returns, given the added risk. Additional borrowing would extend PLUG’s interest rate expense burden, further delaying PLUG’s ultimate goal of operating with a positive bottom line.

Donald Trump’s Fossil-Fuel Agenda Clouds Future

The big issue that could affect not only PLUG but also many of its peers and other renewables companies is President Donald J. Trump. On his first day in office, the newly-elected commander-in-chief signed an executive order ending the so-called ‘Green Deal’ worth $300 billion in green infrastructure funding and revoking national electric vehicle (EV) mandates. Moreover, the most controversial President in U.S. history declared a “national energy emergency” that fossil fuel production would solve.

The news rocked several alternative energy companies, including Tesla (TSLA), Fuelcell Energy (FCEL), and Ballard (BLDP), as investors trimmed positions in green and renewable stocks likely to feel the pinch of fossil-fuel-leaning government policy coming around the corner. The ramifications could be bleaker for PLUG because it is far less established than Tesla in an industry that’s even more embryonic than electric vehicles.

Is PLUG a Good Stock to Buy?

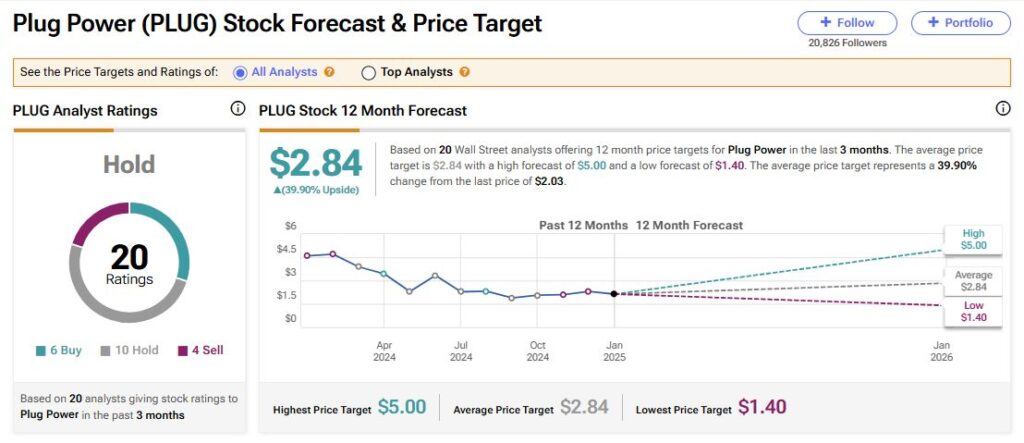

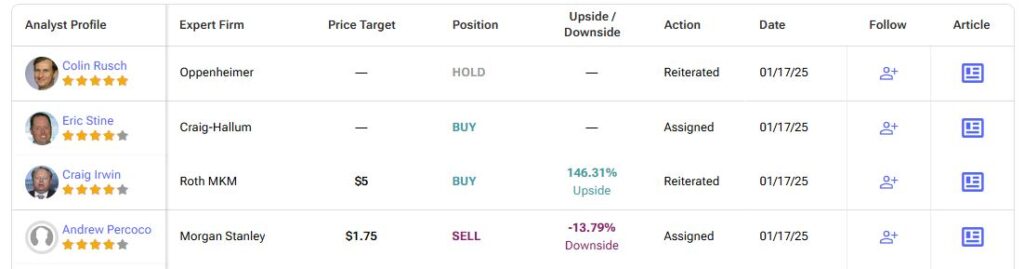

Wall Street analysts have mixed feelings about PLUG stock. The hydrogen technology firm has gathered six Buy, ten Hold, and four Sell ratings over the past three months, resulting in a Hold consensus rating. Note that PLUG stock carries an average price target of $2.84, which implies almost 40% upside potential from current price levels. Still, investors should be wary of the notable risks at present.

Shareholder Dilution Undermines PLUG’s Future

Plug Power’s extraordinary sales growth in recent years has been utterly overshadowed by its persistent losses. The futuristic hydrogen-cell developer relies on excessive debt and destructive shareholder dilution to stay in business, which, needless to say, is an unsustainable long-term business strategy.

Sure, progress in hydrogen technology and lucrative partnerships could push up revenues in the near term, but this may just be too little too late to preserve sentiment in the stock. As many investors can concur: once bitten, twice shy. With shareholder and brand value decaying and PLUG’s management remaining tight-lipped on any meaningful plans to reinvigorate margins, this hydrogen technology bellwether’s future is very gloomy indeed.