Investors are still trying to determine the key value drivers for Palantir Technologies (PLTR) stock, but nobody has cracked the code.

Pick the best stocks and maximize your portfolio:

- Discover top-rated stocks from highly ranked analysts with Analyst Top Stocks!

- Easily identify outperforming stocks and invest smarter with Top Smart Score Stocks

Palantir surged up to the $45 mark in January, as options volume pushed the stock higher. It has since sold off and has been trading close to $25 in August, despite beating earnings on multiple occasions. (See PLTR stock charts on TipRanks)

Palantir — a software company that specializes in data analytics — could be at a turning point due to a better revenue blend, accompanied by continued organic growth.

Better Revenue Mix

Palantir has de-risked its business model by investing across industries. The conglomerate-style allocation of capital will allow for more sustainable revenue, with less reliance on contract-based work alone.

Palantir has invested aggressively of late. The company has gained exposure to the telemedicine industry with an investment in Babylon Health, a doctor/patient facilitator, with a significant value add through its artificial intelligence (AI).

Palantir has invested in six special-purpose vehicles, which intend to provide venture capital to companies in hypergrowth industries such as robotics, drug discovery, and air transport.

Lastly, Palantir has invested $50 million in gold bars as a store of wealth. This makes sense with the bond and money markets suffering a great deal at the moment.

I expect Palantir to acquire on a vertical basis as well, with the objective of synergies. The likes of Silk, Kimono Labs, and FT Technologies were acquired between 2015 and 2016 to improve business intelligence, AI, and digital publishing, but it’s been a while since Palantir has acquired for growth.

Blockbuster Growth

Palantir has continued to strike up deals, with 62 new contracts earned in its second quarter, of which 21 are worth $10 million or more. 20 long-term customers were added in Q2, with the total customer base up 13% quarter-over-quarter, and commercial customers up by 32%.

The company managed to top analysts’ expectations with a revenue beat of $14.54 million, driven by a 90% increase in U.S. commercial revenue. EPS also beat estimates by $0.01.

Wall Street’s Take

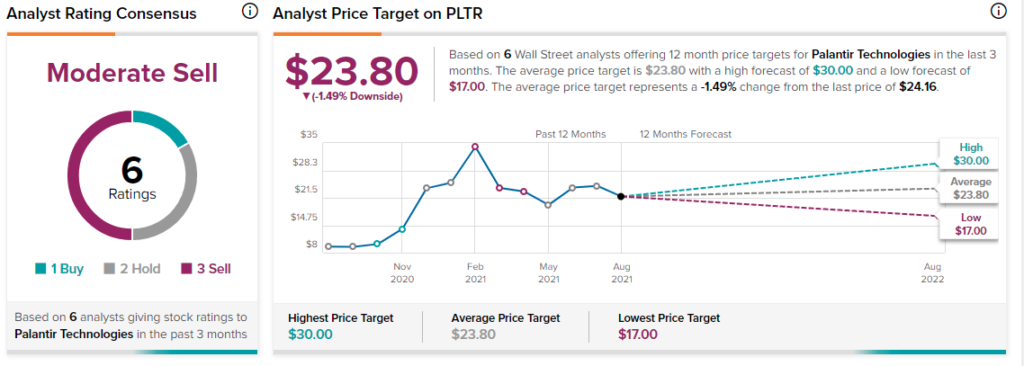

According to TipRanks, consensus among analysts is a Moderate Sell. Out of six analyst ratings, the stock has 1 Buy, 2 Holds, and 3 Sells. The average PLTR price target of $23.80 implies 1.5% downside potential.

What This All Means

Palantir is a company that is growing substantially and using its earnings to acquire assets, which could provide a more diverse revenue mix.

The company still has ridiculously high relative valuation metrics, with a price-to-sales ratio of 36.86 and a PEG ratio of 7.3, but its solid asset base offsets the negatives. Palantir has a debt-to-equity ratio of only 0.5 and has an enterprise value of $46.16 billion, which means that it holds intrinsic value in abundance.

Palantir could be entering a new paradigm, making it an actual investment for once and not just a speculative bet.

Disclosure: On the date of publication, Steve Gray Booyens had no position in any of the companies discussed in this article.

Disclaimer: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities.