ONE Gas (NYSE:OGS) stands out as a captivating choice among the stocks I’ve researched, especially for those looking for stocks with strong dividend growth prospects. If you are not familiar with the company, ONE Gas is a regulated distributor of natural gas that holds a unique advantage due to its dominant position in the states it operates, forming a solid moat.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

With approximately 2.3 million customers, the company taps into the expanding natural gas market, which is increasingly sought after as a reliable energy source. Further, as a utility, it enjoys additional stability, as it is less affected by fluctuating commodity prices and enjoys secure, consistent cash flows. This stability allows management to provide investors with precise multi-year projections, offering exceptional visibility into the company’s future earnings and dividend growth.

Overall, ONE Gas can prove particularly suitable for investors who value predictable dividend growth and opt for investments with minimal volatility. Therefore, given that uncertainty in the market persists despite the recent relief rally, investors are likely to find increased interest in ONE Gas stock. Hence, I am bullish on the stock.

What Makes ONE Gas’ Business a Highly Predictable One?

To grasp the rationale behind ONE Gas’s ability to provide multi-year projections for earnings and dividend growth, it is crucial to comprehend the factors contributing to the business’ exceptional predictability.

Firstly, the firm’s strong market position plays a pivotal role. With an extensive distribution network spanning 65,000 miles of distribution mains, services, and transmission pipelines, ONE Gas supplies natural gas to approximately 2.3 million customers. This expansive reach has allowed the company to secure significant market shares in its operational areas, making it the leading natural gas distributor in Kansas and Oklahoma and the third-largest in Texas. Remarkably, ONE Gas commands 72%, 88%, and 13% in market share in these respective states, establishing a wide moat and a considerable competitive advantage.

Additionally, ONE Gas operates within a regulatory framework where its distribution rates are determined by state authorities. These regulatory bodies ensure that utility companies have the opportunity to earn fair and reasonable returns on their capital investments.

This predictable rate-setting process has enabled ONE Gas to provide highly precise outlook estimates for its medium-term net income and dividend growth. Specifically, management foresees base rate increases of 7% to 9% through 2027. Coupled with a growing customer base, consistent natural gas consumption patterns, pre-determined capital expenditure requirements, and share capital dilution, the company expects its annual earnings per share to grow between 4% and 6% over the same period.

The ability to forecast such a narrow earnings-per-share growth trajectory empowers management to present a corresponding dividend growth outlook. Thus, ONE Gas anticipates dividend hikes ranging from 4% to 6%. This aspect demonstrates the company’s commitment to driving strong investor confidence and enhances the stock’s attractiveness as a long-term investment.

Q1 Performance in Line with Management’s Target

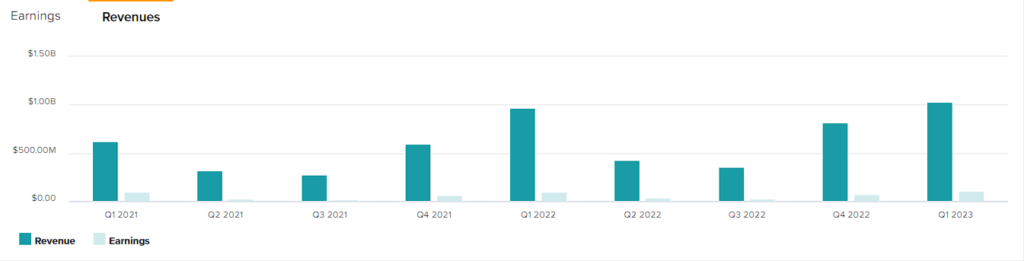

In its most recent results, ONE Gas once again showcased its remarkable ability to deliver stable results that are in line with management’s multi-year targets. In Q1 2023, the company posted revenues of $1.03 billion, representing a year-over-year growth rate of 6%. This performance can be attributed to robust demand for natural gas, a gradual increase in customer base, and strategically implemented rate hikes.

While operating costs also experienced a 13.8% increase to reach $217.1 million, the resulting growth in operating income, though more modest, was still quite favorable. Specifically, the company’s operating income stood at $149.2 million for the quarter, surpassing the prior-year figure of $140.8 million.

This achievement was fueled by rate increases totaling $17.3 million and a noteworthy reduction of $1.6 million in expenses associated with the lingering impact of the COVID-19 pandemic. Higher depreciation, employee-related expenditures, and a minor bad debt expense partially offset these advancements.

Furthermore, higher interest expenses placed some pressure on the bottom line. Nevertheless, earnings per share exhibited growth of two cents, reaching $1.85.

Of greater significance, management reaffirmed their previously provided guidance, expressing their confidence in ONE Gas’ performance for the Fiscal Year 2023. They anticipate earnings per share for Fiscal 2023 to fall within the range of $4.02 to $4.26.

Given that management’s intention would be to beat its own outlook, assuming earnings per share do indeed align with the higher end of this range, this would imply year-over-year growth of approximately 4.5%, aligning with the firm’s medium-term outlook. During Q1, OGS grew its dividend for the ninth consecutive year by 4.8%, which also matches its multi-year dividend growth targets.

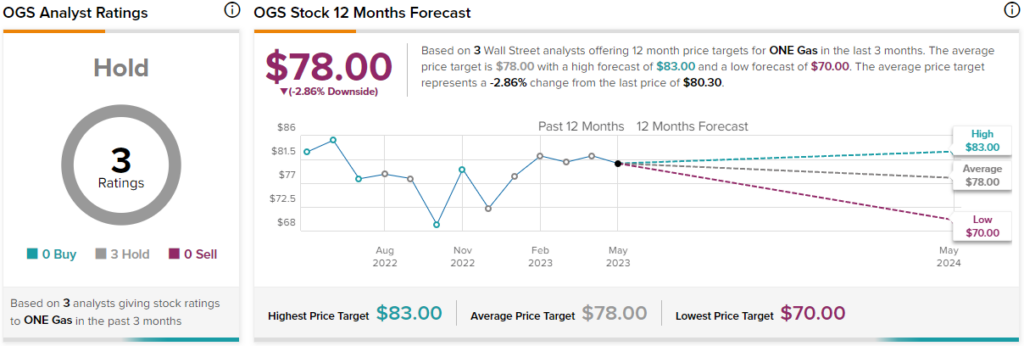

Is OGS Stock a Buy, According to Analysts?

Turning to Wall Street, ONE Gas has a Hold consensus rating based on three unanimous Hold ratings assigned in the past three months. At $78.00, the average OGS stock forecast suggests 2.9% downside potential.

The Takeaway

Wall Street analysts don’t seem too excited regarding ONE Gas’ upside potential, appearing neutral on the stock. To some extent, I would agree. Similar to other utility companies, OGS stock shouldn’t be anticipated to generate extraordinary returns for investors.

However, the company’s reliable business model and long-term projections offer a remarkable safety net and enhanced predictability. Presently yielding 3.2%, coupled with a clear trajectory for gradual increases in dividends in the upcoming years, dividend growth investors are likely to consider this stock a suitable addition to their portfolios, making me bullish overall.