NIKE (NYSE: NKE) is the world-leading designer, marketer, and distributor of footwear and sports apparel globally. The company recently reported revenues of $46.33 billion over the past 12 months.

What I find most exciting about Nike is that the company finds ways to grow every quarter. The most recent expansion strategy has been to use its online presence to sell directly to customers through a “Customer Direct Acceleration” strategy.

Also impressive is the company has added 280 basis points to its gross margin, bringing it up to 45.9%. Other remarkable numbers from Nike’s most recent quarterly reports (Q2 2022 released on December 20, 2021) were Nike direct sales were $4.7 billion, up 9%, and Nike brand digital sales were up 11% on a currency-neutral basis, led by a 40% growth rate in North America.

These figures all make me believe that Nike has figured out the correct strategy to continue to grow during 2022 and beyond.

Based on the intrinsic value of this stock, the Wall Street analyst’s estimates, blogger estimates covering NKE, and the strength of its management team and track record, I am bullish on this stock.

Recent Results and Dividend

Nike stock has been trading between $125.44 (the 52-week low set on June 18, 2021) and $179.10 (the 52-week high set on November 5, 2021).

The company reported Q2 2022 earnings of $0.83 per share, beating analyst estimates of $0.63 per share by $0.20. It has also reported $3.82 in earnings per share for the past 12 months, beating analyst estimates of $3.02 for that period.

The company also has an impressive history of increasing its dividend. The company announced on November 18, 2021, that it was increasing its quarterly dividend by an outstanding 11% to $0.305 per share. This marks the 20th year in a row that Nike has increased its dividend.

Nike has also placed itself in the small group of dividend-paying stocks that are increasing the size of its dividend by more than inflation, meaning investors are earning more over time.

The company has a solid set of financial statements. Nike has a current ratio of 3.06, so it has enough current assets on hand to pay its bills for the next three years at its current cash burn rate.

It also means it has the cash to fund research and development as well as fuel purchases of things like wearable technology.

I also noticed that Tim Cook is a member of Nike’s board of directors. This suggests multiple possibilities for future collaborations between Nike and Apple on wearable technologies in clothing and footwear.

While I have no idea if these talks are happening, the chance of having the people who run both companies in the same room multiple times a year makes me very excited for future opportunities.

When I calculated the stock’s intrinsic value by modeling discounted cash flows, I pegged it at $189.18.

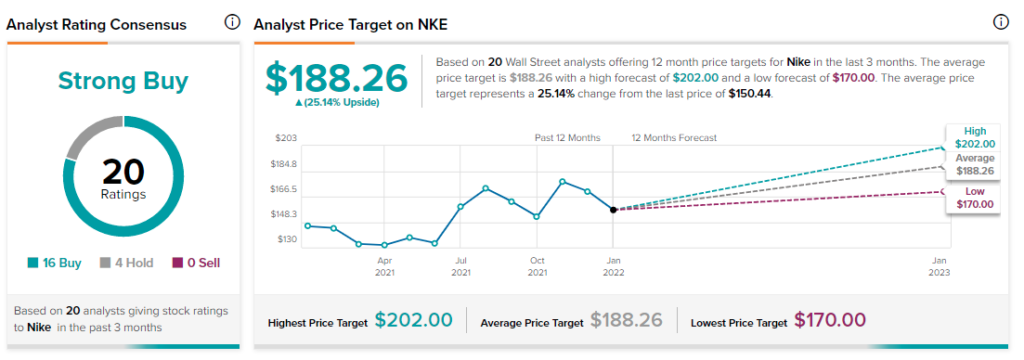

Wall Street’s Take

Twenty Wall Street analysts currently cover NKE and have issued 12-month estimates for the price. The stock holds a Strong Buy consensus rating, based on 14 Buys and four Holds assigned.

The average Nike price target of $188.26 suggests 25.1% upside potential.

TipRanks.com shows that of the 46 bloggers that have blogged about NKE, 80% of them are bullish.

Conclusion

This company is a significant growth stock, paying a hefty dividend to boot, which should be translated into healthy returns for shareholders for years to come.

Download the TipRanks mobile app now

Read full Disclaimer & Disclosure