Going by the recent performance of Netflix (NFLX) stock – the shares have fallen by ~17% since the late-January’s highs – investors appear to be not too keen on the Paid Sharing launches across several international markets (Canada, New Zealand, Spain, Portugal).

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

J.P. Morgan analyst Doug Anmuth believes the downbeat performance is due to “considerable early pushback” around the initiative, with “elevated news headlines, Twitter activity, & customer support engagement” all resulting in worries around “near-term churn.”

“Apptopia Downloads (DLs) data suggests increased volatility across all four Paid Sharing markets since the rollout,” the 5-star analyst went on to note, “but we believe headlines may also be impacting other markets where Paid Sharing has not yet been rolled out, including the US.”

Back in January, the streaming giant said it anticipates a wider rollout of Paid Sharing later in the quarter. With Q1’s end in sight, Anmuth believes that may yet happen over the next few days, but he also believes that given the “early friction,” investors are increasingly concerned the rollout might be delayed further into 2Q and beyond. “That could put NFLX’s projection for more net adds in 2Q than 1Q at risk,” says the analyst.

That also raises the prospect of a wider Paid Sharing rollout in what is usuallya “seasonally weak” quarter (Q2), which also does not seem to have much in the way of “hit content.”

On the other hand, a slower rollout of the initiative could lead to better-than-expected Q1 net adds. Timing considerations aside, Anmuth anticipates NFLX to “continue down the path of transitioning users away from widespread account sharing,” and making various tweaks along the way.

And that, in the long run, is no bad thing. “Ultimately we expect NFLX to generate more revenue through the combination of Extra Members and new standalone accounts, especially as Paid Sharing is paired with the low-priced Basic With Ads tier (BWA),” the 5-star analyst summed up.

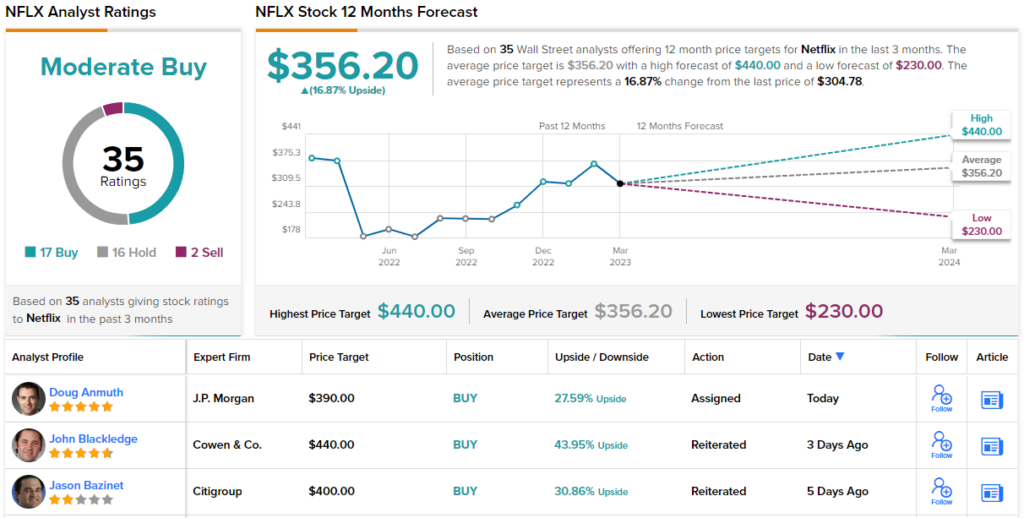

All in all, Anmuth keeps a bullish stance by reiterating an Overweight (i.e., Buy) rating, backed with a $390 price target. The implication for investors? Upside of 27% from current levels. (To watch Anmuth’s track record, click here)

Turning now to the rest of the Street, where NFLX’s Moderate Buy consensus rating is based on 17 Buys, 16 Holds and 2 Sells. The analysts see shares rising by 17% over the coming months, considering the average target currently stands at $356.2. (See Netflix stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.