They say all good things must come to an end eventually, but luckily for Netflix (NFLX) all bad things don’t last forever too. After a period of sustained sub losses, the streaming giant managed to steady the ship in Q2 and delivered a better-than-feared earnings report.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Although global net paid subscribers fell by 1 million during the quarter, the figure bettered the 2 million losses Netflix and the Street had anticipated.

Subs in EMEA fell by 0.8 million compared to -0.3 million in the previous quarter and +0.2 million in the same period last year, while UCAN shed -1.3 million subscribers, worsening on the -0.6 million sub losses of Q1 and -0.4 million of one year ago. However, these regional losses were somewhat countered by positive subscriber growth in APAC and LATAM.

Reflecting the impact of price hikes earlier this year, churn was high in UCAN at the start of the quarter but got better as the period advanced and despite the subs decline, Netflix’s take of TV viewing stayed notably robust. According to Nielsen data, in June, the company notched a new high of 7.7% share of US TV viewing, a ~110bps year-over-year increase.

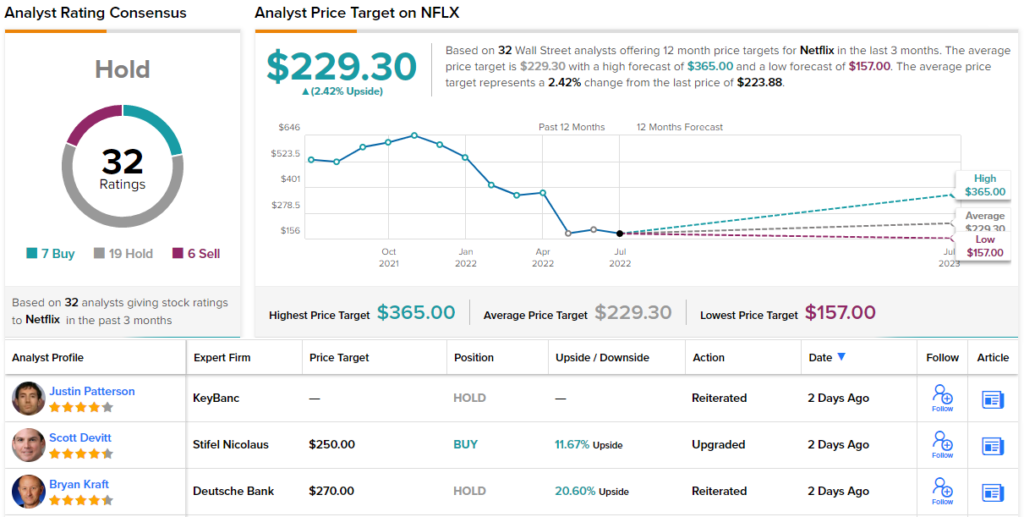

Assessing the print, Stifel’s Scott Devitt thinks the performance signals a “new beginning.”

“With signs of stabilization in the subscriber base emerging, we believe the prospect of a prolonged period of subscriber losses is becoming increasingly unlikely,” explained the analyst. “Investor focus can now appropriately shift to the viability of Netflix’s growth initiatives, including monetizing password sharing and the introduction of ad-supported tiers, both of which will be introduced next year.”

Netflix will also need to address its difficulties with pricing in developing regions and improve monetization in relatively established markets in order to spur growth. With a tried-and-true management team and improving FCF dynamics, Devitt believes the company has a number of “increasingly defined levers” to address these problems. As management realigns the company for its upcoming phase of growth over a multi-year timeframe, the analyst sees “numerous potential catalysts.”

Based on the above, Devitt thinks an upgrade is warranted; therefore, the rating moves from Hold (i.e., Neutral) to Buy, and the price target gets a bump too – shifting from $240 to $250. What’s in it for investors? Upside of 12% from current levels. (To watch Devitt’s track record, click here)

Most on the Street aren’t quite ready to make such a change; 19 Holds outgun 7 Buys and 6 Sells and result in a Hold consensus rating. Going by the $229.3 average target, shares are expected to stay rangebound for the foreseeable future. (See Netflix stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.