Global semiconductor giant Taiwan Semiconductor (TSM) has caught the attention of Needham analyst Charles Shi. He maintained a Buy rating on the stock and a price target of $110. According to the analyst, the three key parameters that will define TSM’s revenue growth in the upcoming quarters are wafer capacity, fab utilization, and wafer price. Based on his analysis, Shi is confident that the chip maker will be able to grow its revenue by 15% in 2023.

TSMC is one of the largest semiconductor manufacturers in the world. Its chips are used in several end markets, including high-performance computing platforms (like personal computers, tablets, servers, and game consoles), automotive, Internet of Things (includes connected devices like smart wearables and surveillance systems), and digital consumer electronics like TVs and cameras.

TSMC’s Wafer Capacity is Expected to Rise

A wafer is a thin slice or substrate of semiconductor material that is used in the production of integrated circuits (ICs). Thus, a foundry’s revenue earning capability depends on the total wafer capacity.

Shi noted that TSMC’s revenue growth potential for 2023 depends on the amount of wafer capacity it adds in 2022. TSMC has guided for $40 billion of capital expenditures in 2022, 70%-80% of which will be spent on advanced nodes (7nm and below), 10% – 20% on mature nodes (16nm and above), and the remaining 10% on the packaging, testing, and photomask making.

Moreover, TSMC has projected annual capacity growth of 7% in 2022. As per Shi, this will result in the company adding “30-40K monthly capacity for 5nm, 30-40K monthly capacity for 3nm, and 40-50K monthly capacity for 28nm and 40nm in 2022.”

TSMC’s Fab Utilization to be Fully Loaded by 2022

Fabrication is the manufacturing site where raw silicon wafers are converted into ICs. Shi believes that TSMC’s fab utilization will reach almost 100% by the end of 2022, except for a minor decline of 7nm fab utilization in November and December.

Furthermore, Shi anticipates that the semiconductor industry will be in a downturn in 2023. His model assumptions portray that, under a worst-case scenario, “TSMC’s fab utilization rate for 28nm and above dropping to 80%, on par with the company’s 28nm utilization rate in the 2018-2019 downcycle.”

Moreover, the fab utilization rate for 16nm and 7nm could also see a slight decline in 2023, but the full year 2023 rate should remain at or above 90%.

Remarkably, Shi believes that TSMC’s 5nm fab utilization will remain full, thanks to a majority of customers migrating to its 5nm nodes from the earlier adapted 7nm nodes. However, since TSMC is the only major player in the 5nm nodes, Shi believes that it will keep these nodes strategically undersupplied.

Most importantly, Shi expects TSMC’s latest entrant, the 3nm fab, to remain underutilized in 2023 once it enters mass production. In Q4FY23, the 3nm fab may hit full utilization once iPhone demands hit their seasonal peaks.

TSMC’s Wafer Pricing Will Remain Strong

TSMC may not be under pressure to lower wafer prices as much as competitors due to its premium offerings. The analyst believes that TSMC’s price increase of 6% may kick in during Q4FY22 and continue well in 2023.

On the contrary, the tier-2 and tier-3 foundries may cut prices by 10%-20% in the near term as they have rigorously hiked prices in 2021.

To sum it up, Shi noted, “Fundamentally, we believe TSMC’s near monopoly position in 5nm and 3nm, both of which are expected to ramp meaningfully in 2023, will help the company defy the industry downcycle. We think TSM stock is in the bottoming process.”

Shi reiterated a Buy rating on TSMC stock with a $110 price target which implies an impressive 38.1% upside potential to current levels.

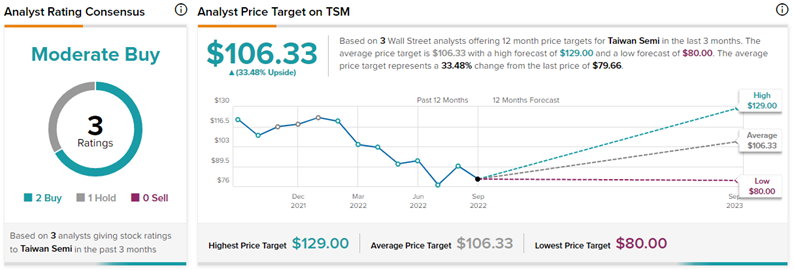

What is TSM’s Price Target?

On TipRanks, TSM stock has a Moderate Buy consensus rating based on two Buys and one Hold. The average Taiwan Semiconductor price target of $106.33 implies 33.5% upside potential to current levels. Meanwhile, the stock has lost 37.7% so far this year.

Ending Thoughts

Based on Shi’s assumptions of wafer capacity, fab utilization, and wafer pricing, the analyst is confident that Taiwan Semiconductor will be able to achieve a 15% revenue growth rate in 2023. TSM’s 5nm and 3nm will contribute the most towards the revenue jump. Importantly, Shi believes that 5nm nodes will hit a 50% revenue growth in 2023, accounting for almost 33% of TSMC’s sales next year. Also, 3nm nodes, which are still in their nascent stages will contribute 4% of 2023 sales.