What should we make of the stock markets? The S&P 500 plunged into correction territory last week – its first since 2023. Several factors weighed on investors’ minds, including President Trump’s inconsistent use of tariffs, recession worries, and a close skate by a US government funding shutdown.

The shutdown was averted when Senate Democrats refused to filibuster the continuing resolution, but the real confusion likely stems from a sudden and radical shift in policy with the change in power in Washington. We’re only two months into Trump’s new term and still waiting to see how things unfold.

Yung-Yu Ma, chief investment officer of BMO Wealth Management, sums up the situation in recent comments: “The markets are grappling with the notion of where fair value rests for a stock market that faces headwinds from tariffs, fiscal spending cuts, and potentially softening economic data… Negative investor sentiment is building, so a multi-day relief rally could be coming soon.”

The stock analysts at BMO are following that line of thought, pointing out two stocks that investors should buy ahead of a potential rebound. We dug into the TipRanks database to get the full picture on these picks. Here’s what we found.

Samsara, Inc. (IOT)

The first stock we’ll look at, Samsara, is a leader in the field of operational software. The company offers a variety of software packages designed to coordinate and connect the disparate and related activities of industrial and management physical operations. In short, the company offers a wide range of safety, efficiency, and control solutions for many of the day-to-day tasks faced by urban managers and physical plant operators in the construction, energy, public sector, and retail, transportation, and utility industries.

Samsara’s software products provide data analysis, network connections, video monitoring, workforce and workflow apps, site visibility—among a host of other functions. The company has found success, visible in its $21 billion market cap and a customer list that includes such major names as Ecolab, Home Depot, and Sysco. Samsara boasts that its software platforms are in use by tens of thousands of customers, and digitize over 265 million workflows annually. Even more important, for both users and the public, the company’s products help prevent more than 200,000 industrial accidents every year.

The company manages all of this on the global stage. In North America, it has offices in San Francisco, its headquarters, as well as in Atlanta, Phoenix, and Mexico City. Globally, the company has footprints in Taiwan, India, the UK, the Netherlands, France, Germany, and Poland.

Since peaking at approximately $61 in February of this year, shares in IOT have fallen by more than 37%. At the same time, however, the company has reported continued gains in revenue and earnings. The last quarterly report, which covered fiscal 4Q25, showed a top line of $346.3 million, up 25% year-over-year, and a bottom line, by non-GAAP measures, of 11 cents per share, almost triple the 4-cent figure reported for fiscal 4Q24. In addition, both revenue and earnings beat their forecasts, revenue by almost $11 million and the non-GAAP EPS by 4 cents per share.

Of particular interest, as an indicator of continued growth, the company’s annual recurring revenue at the end of fiscal Q4 hit $1.46 billion, for a 32% year-over-year increase.

Yet, the shares fell following the quarterly readout due to a soft guide. For FY26 Samsara anticipates revenue will land in the range between $1.523 billion to $1.533 billion, with the midpoint slightly below analysts’ expectation of $1.53 billion.

However, for BMO analyst Daniel Jester, the pullback in this stock creates a sound buying opportunity. He focuses on the company’s combination of solid performance and potential to maintain the same, writing, “With shares down more than [30%] over the past month, we see a more attractive risk/reward for a high-quality company. Shares now trade at ~12x NTM revenue, towards the low-end of the range seen over the past two years, and at the smallest premium to the broader software market in nearly a year… We think 4Q results did not suggest a material shift in underlying trends, and anticipate both revenue and EBIT margin upside to emerge as the year progresses.”

Jester goes on to outline a path forward for the stock, and says of IOT, “While worries are reasonable amid unknown impacts from slower growth and tariffs, Samsara has been navigating challenging end markets in several key verticals for some time with still impressive growth, thanks predominately to supportive ROI dynamics which we think drive growth resiliency across the cycle. The company’s massive data assets are growing 1.5x of the pace of ARR growth, supporting AI-use cases in training, safety and more.”

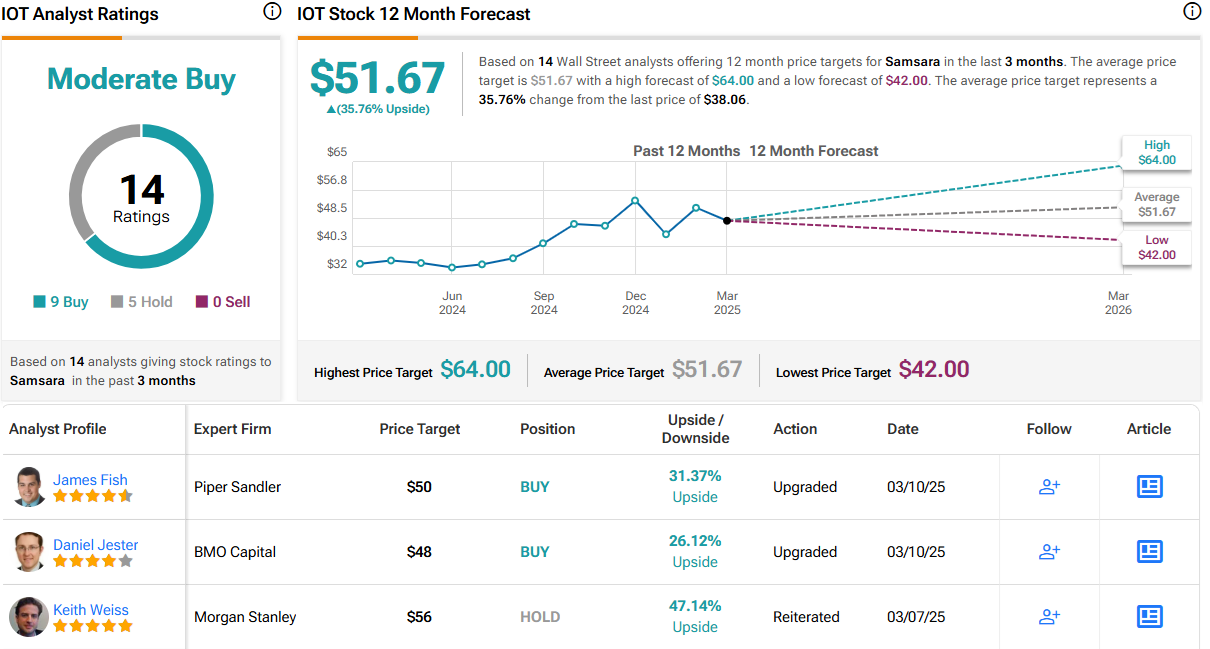

Taken together, these comments back up Jester’s Outperform (i.e., Buy) rating on this stock, while his price target of $48 points toward a one-year upside potential of 26%. (To watch Jester’s track record, click here)

Overall, IOT shares hold a Moderate Buy consensus rating from the Street, based on 14 recent reviews that break down to 9 Buys and 5 Holds. The stock is currently trading for $38.06, and the $51.67 average price target implies a 36% gain in the next 12 months. (See IOT stock forecast)

SailPoint, Inc. (SAIL)

Next on our list of BMO picks is SailPoint, the well-known identity security software company. SailPoint was founded in 2005, and today counts half of the Fortune 500 firms among its customer base. The company offers its customers an array of security solutions designed to ensure safe access and remote connections through a unified AI-driven platform. Using SailPoint’s platform, enterprise customers can streamline their security processes at any scale, reaping benefits in the form of increased efficiency and improved system protection.

SailPoint’s key attraction is automation; the company’s platform lets users automate much of their authentication work. According to SailPoint, up to 90% of all identity tasks can be automated, resulting in a 66% reduction in access privilege-related risk events, and a 60% reduction in onboarding costs. System managers can modernize their security, with up-to-date password management, access certification, and cloud governance. SailPoint’s flagship platform, SailPoint Atlas, provides all of this, and more, through use of both AI and scalable platform architectures.

We should note here that SailPoint first entered the public trading domain in 2017, and traded publicly until 2022 when it was acquired and taken private by the Thoma Bravo equity firm. Earlier this year, however, SailPoint re-entered the public markets with an IPO held in February, putting 60,000,000 shares on the market at $23 each. The company raised $1.38 billion in its IPO. However, since entering the public markets again, the stock has declined by 19%.

For BMO’s Keith Bachman, SailPoint’s greatest strength is the essential nature of its niche. IT security is a vital service in today’s digital world, and this fact underlies anything else that can be said about the company. Bachman writes of SailPoint, “We believe that security remains a top IT spend priority, identity is one of the most important areas within security, and SailPoint is one of the key players in the identity market. Further, we believe that SailPoint will benefit from consolidation of identity spend… We think SailPoint can sustain low-20% y/y type ARR growth over the next few years as identity becomes increasingly prioritized within security… We believe that the growth of machine and agent identities can drive potential upside to our estimates as we look longer-term.”

The BMO IT expert quantifies his stance on SAIL shares with an Outperform (i.e., Buy) rating and a $26 price target that suggests a 39% upside in the next 12 months. (To watch Bachman’s track record, click here)

SailPoint has picked up 10 recent analyst reviews since going public again, and these split 8 to 2 in favor of Buy over Hold for a Strong Buy consensus rating. SAIL is currently trading for $18.70 and its $27.05 average target price implies that the stock will gain 44.5% over the coming year. (See SAIL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.