The Q3 earnings season is in full swing, and we’ve already seen the first wave of big tech results. Investors were not thrilled; Google parent Alphabet reported a slowdown in cloud revenues, and the stock market fell sharply on sentiment that Q3 earnings may not be as pretty as predicted.

But the outlook is less cloudy for the coming year. In a recent note on current and coming conditions, investment bank Morgan Stanley notes that growth is expected to jump heading into next year: “For 3Q, consensus expects 1.7% sales growth before a recovery to the 3-4% range in 4Q and 2024… while 2024 EPS growth is expected to be 12%. Although 2023 and 2024 estimates have been relatively flat since February, the consensus… for the S&P 500 is approaching new highs as the time-weighting takes more of the 2024 estimate into account.”

So there’s some room for optimism as we head into 2024, and investors can definitely find stocks with solid growth potential, even in today’s unsettled conditions. Against this backdrop, Morgan Stanley’s stock analysts are busy pointing out ‘high conviction’ stocks with strong catalysts approaching in the near term – and the bank’s analysts are predicting that these names have at least 70% upside potential on those catalysts.

We’ve used the TipRanks platform to find the latest details on two of these stocks. Let’s take a closer look.

Don’t miss

- Wall Street’s Best Analyst Bets on These 3 Energy Stocks — Here’s Why You Might Want to Follow His Lead

- ‘Stay Cautious,’ Says Billionaire Leon Cooperman About the Stock Market — Here Are 2 High-Yield Dividend Stocks He’s Using for Protection

- Piper Sandler Says the S&P 500 Could Still Surge 14% in 2023 — Here Are 2 Stocks to Keep an Eye On

Cytokinetics (CYTK)

The first Morgan Stanley pick we’re looking at is Cytokinetics, a clinical-stage biopharmaceutical firm engaged in the discovery, development, and commercialization of new muscle activator and muscle inhibitor drugs. These are potentially first-in-class drugs designed as treatments for patients with debilitating diseases that cause compromise and decline in muscle function and performance.

Cytokinetics’ leading drug candidates are small molecule compounds engineered to target cardiac myosin contractility. The company’s late-stage candidate Omecamtiv Mecarbil is a cardiac myosin activator and has been tested as a treatment for heart failure with reduced ejection fraction. The drug has completed Phase 3 testing, and the company is in talks with both the FDA and EMA regarding further necessary regulatory procedures.

The bigger story here, however, is aficamten, another late-stage drug candidate. Aficamten is a cardiac myosin inhibitor and is being tested as a treatment for hypertrophic cardiomyopathy. The drug candidate is currently the subject of the SEQUOIA-HCM Phase 3 clinical trial, and preliminary data released earlier this month showed that the study is meeting its objectives. The upcoming catalysts for this program include the release of topline data from the Phase 3 study, expected by the end of this year.

5-star analyst Jeffrey Hung covers this stock for Morgan Stanley, and agrees that the SEQUOIA-HCM study is the key, writing: “CYTK has a favorable setup heading into the aficamten Phase 3 SEQUOIA-HCM results, one of this year’s high profile data readouts in biotech (expected by year end). CYTK shares have been under pressure for the last year as the launch trajectory for competing drug Camzyos has been disappointing, leading investors to question the market potential for aficamten. We think recently reported patient baseline characteristics in SEQUOIA-HCM and additional long-term data from FOREST-HCM further support the potential for positive results from SEQUOIA-HCM.”

Hung goes on to outline aficamten’s advantages over the competition, an important point for investors to consider: “We believe aficamten is largely clinically derisked given that it has the same mechanism of action as Camzyos. Aficamten is likely to be differentiated based on its improved properties (shorter half-life and faster titration/reversibility), potentially translating to less stringent Risk Evaluation and Mitigation Strategies (REMS) requirements and/or improved efficacy.”

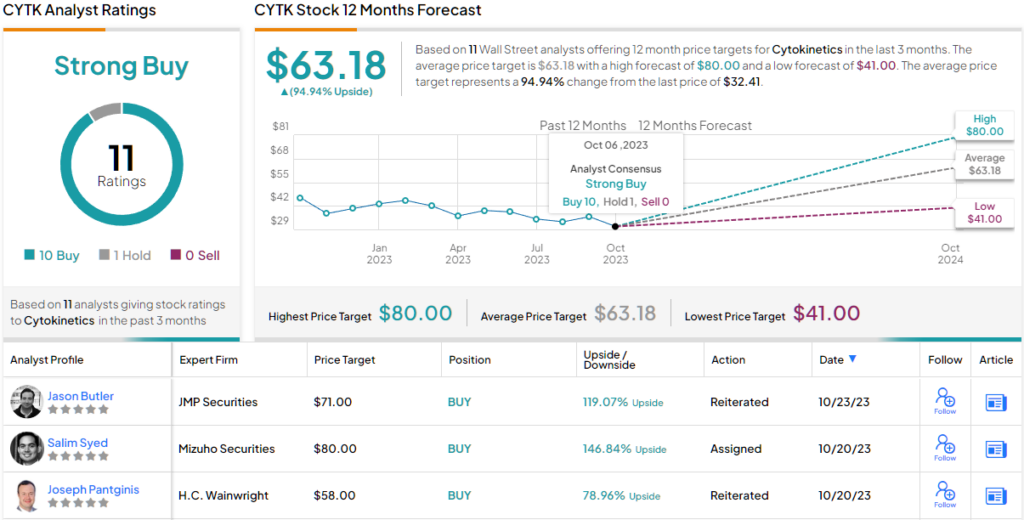

Hung sees this as reason to rate CYTK as Overweight (i.e. Buy), with a $60 price target pointing toward an 85% upside in the next 12 months. (To watch Hung’s track record, click here)

Overall, CYTK has picked up 11 recent analyst reviews, including 10 Buys against 1 to Hold – for a Strong Buy consensus rating. The shares are selling for $32.41 and the average price target, at $63.18, implies a robust ~95% upside for the coming year. (See CYTK stock forecast)

LifeStance Health Group (LFST)

The next stock Morgan Stanley is betting on is LifeStance, a company in the healthcare field that specializes as a provider of mental health services. LifeStance can connect patients with both in-person and online virtual mental healthcare services, which are offered on an outpatient basis for adults, adolescents, and children. The company works with 600 service centers across 33 states and has approximately 6,100 professional clinicians available for patients to choose from. LifeStance can connect patients with psychologists, therapists, advanced practice nurses, and psychiatrists.

Mental health is a growth segment of the healthcare industry, as the social stigma related to mental illness has been receding since the 1990s. LifeStance has leveraged that fact to generate growing revenues over the past several years, achieving consistent quarter-over-quarter top-line gains since the company went public in 2021.

One important figure will provide the essence of the story. In the company’s last quarterly financial release, for 2Q23, LifeStance reported a total of 6,132 clinicians on the roster, up 17% from the prior year.

Strong customer growth supported robust revenue growth. LifeStance reported Q2 revenues of $259.6 million, up 24% year-over-year and $4.4 million above the forecasts. At the bottom line, the company’s net loss of 13 cents per share was an improvement from the 19-cent EPS loss of the prior-year quarter, although it missed the estimates by 4 cents per share.

Looking ahead, the Street expects to see an 8-cent EPS loss for Q3 and revenues of $255.2 million; the company will report its Q3 results on November 8 before the opening bell.

Morgan Stanley’s 5-star analyst, Craig Hettenbach, covers LifeStance, and is upbeat on the company’s coming financial release. He writes, “We expect the company to deliver revenue upside in Q3 and guide above for Q4. With 2023 being characterized as a year of investment in the business, we’re looking for additional anecdotes on operational improvements (i.e., reduction in visit cancelation rates, increased clinician productivity, improved funnel conversion) that serve to instill greater confidence in margin expansion in 2024.”

Hettenbach doesn’t stop with that, as he is also impressed with LifeStance’s management, business model, and forward prospects: “Since industry veteran Ken Burdick joined LifeStance as Chairman and CEO in September 2022, execution has improved significantly yet the stock is down 30% and short interest has increased 40%. This is counter to improvements being made in the company’s business model and the strong secular growth drivers in mental health.”

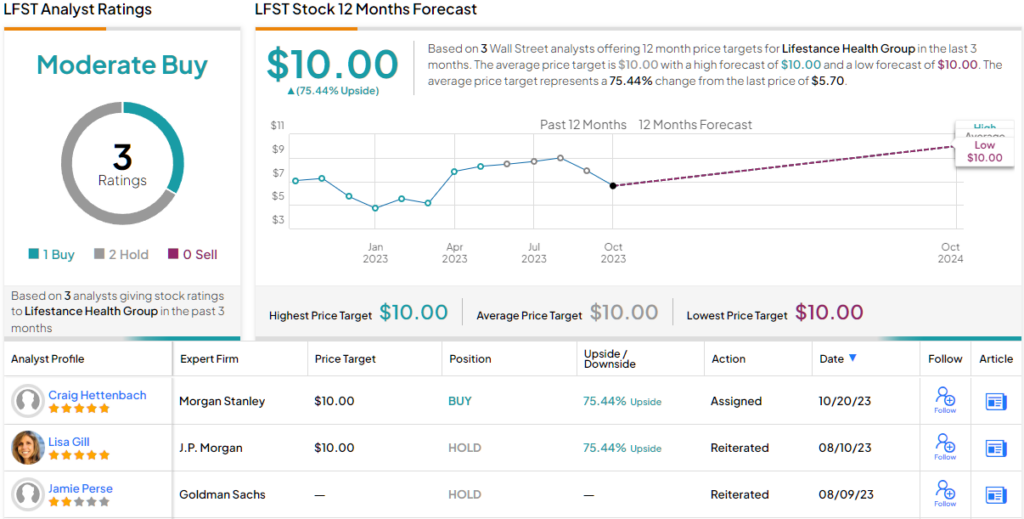

This all adds up to a stock with places to go, and Hettenbach rates LFST shares as Overweight (i.e. Buy). His price target, set at $10, implies the stock has a 75% upside potential by the end of next year. (To watch Hettenbach’s track record, click here)

Looking at the consensus breakdown, 1 Buy and 2 Holds have been published in the last three months. As a result, LSFT gets a Moderate Buy consensus rating. The $10 average target is the same as Hettenbach’s objective. (See LSFT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.