Is Walt Disney (NYSE:DIS) finally ready to turn a corner? There were plenty of positives to pore over after the House of Mouse released its fiscal fourth-quarter earnings report last week.

Although the $21.24 billion in revenue missed consensus expectations by a modest $170 million, investors seemed to overlook this shortfall as Disney’s cost-cutting efforts exceeded expectations, and its profitability profile did too.

As far as cost savings go, Disney is on course to reach annualized cost savings of $7.5 billion, $2 billion above its prior expectations of $5.5 billion. On profitability, adj. EPS rose from $0.30 in the same period a year ago to $0.82, some distance above the Street’s forecast of $0.71.

Meanwhile, streaming subscriber growth came in better-than-expected, with almost 7 million subs added in the quarter, bringing Disney+ subscribers to 150.2 million, with the analysts only expecting a touch above 147 million.

Based on ongoing operating income growth and cost reductions, Disney guided to operating cash flow of $14 billion in FY24. That’s a level not witnessed since FY18.

Morgan Stanley analyst Benjamin Swinburne believes the Experiences and DTC (direct-to-consumer) segments, in addition to gradual efficiency efforts, are “the primary drivers of this growth,” with the analyst also looking forward to the ongoing evolution of Disney’s streaming offerings and the return of its dividend.

“Overall,” Swinburne went on to say, “we see a high ROIC and high growth business in Experiences as undervalued in DIS shares today and a Media business that is both under-earning and undervalued. The incremental efficiency steps announced should help address the under-earning elements of its Media business, while product enhancements in streaming and strategic partnerships at ESPN in success will re-rate these assets.”

Accordingly, Swinburne rates DIS shares an Overweight (i.e., Buy) alongside a $105 price target. The implication for investors? Upside of 18% from current levels. (To watch Swinburne’s track record, click here)

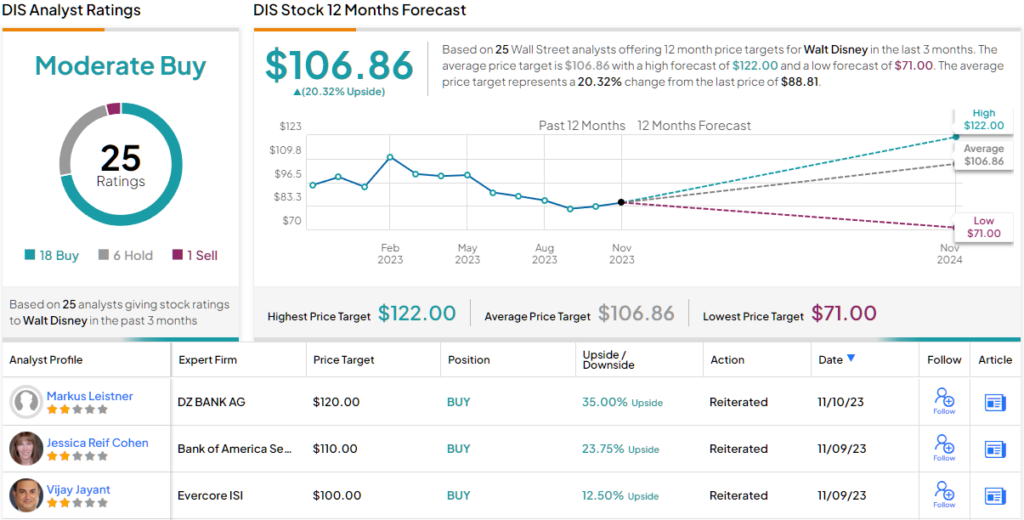

The rest of the Street mostly backs Swinburne’s stance. 17 analysts join him in the bull camp and with the addition of 6 Holds and 1 Sell, the stock claims a Moderate Buy consensus rating. The $106.86 average target is just a touch higher than Swinburne’s objective, implying ~20% upside potential. (See Disney stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.