If the rise of Donald Trump has taught us anything about politics, it’s to expect the unexpected – but with his second term as President just a few days away, there are a few things that we can confidently predict. Prime among these is a drastic change in American energy policy.

A supportive policy for energy will likely include both new exploration and new drilling activities – and that will open up plenty of opportunities as oil and gas companies expand their revenue bases.

Morgan Stanley’s sector expert Devin McDermott is reevaluating his stance on energy companies, in light of these likely developments. The 5-star analyst has tagged two energy stocks in particular as buying opportunities and is placing bets on both.

Let’s take a closer look at these names, using data from the TipRanks database, to find out just what makes them compelling choices today.

Permian Resources (PR)

We’ll start with Permian Resources, an independent oil and gas exploration and production (E&P) company based in Midland, Texas. The company works mainly in the state’s rich Permian Basin, near the boundary with New Mexico. Permian Resources’ holdings include a total of 450,000 net acres, of which 85,000 are net royalty acres. Of the hydrocarbon reserves on those holdings, an estimated 46% is oil. In the company’s last reported quarter, 3Q24, Permian’s average production reached 347.1 thousand barrels of oil equivalent per day (MBoe/d).

In recent months, Permian has taken actions to both expand its E&P activities and streamline its overall operations. In September of last year, the company completed a bolt-on acquisition to its assets in the Delaware Basin, a rich sub-region of the larger Permian formation. This transaction involved Occidental Petroleum and added some 29,500 net acres—of which approximately 9,900 were net royalty acres—to Permian’s holdings in Reeves County, Texas.

More recently, in December, Permian announced an agreement with Kinetik Holdings to sell its oil and gas midstream assets in Reeves County. The divested assets include gathering systems and pipelines. Permian stands to receive $180 million in cash consideration, subject to adjustments post-closing.

On the financial side, Permian reported solid results in its Q3 earnings. Revenue was up 60.8% year-over-year, hitting $1.22 billion and beating the forecast by $10 million. At the bottom line, the company realized a GAAP EPS of 53 cents, up 40 cents from the prior year and 21 cents per share better than expected. Also noteworthy, the company’s adjusted free cash flow in Q3 was $303 million, up 84% year-over-year.

When we check in with Morgan Stanley analyst McDermott, we find that he is upbeat about Permian’s ability to improve efficiency without compromising the quality of its assets or its ability to generate free cash flow. He writes of the company: “PR is differentiated by a high-quality asset base, capital efficient growth, and a low cost structure, supporting sustainable (and growing) free cash flow generation. Management has a track record of operational execution and financial discipline. We estimate PR offers 2025 FCF yield of 11% FCF and 3.4x EV/EBITDA at $70 WTI (oil E&P median of 11% and 3.7x), while also offering stronger growth (12% oil per debt adjusted share CAGR over the next three years vs. 6% median for peers). As one of the lowest cost operators in the Permian, we see upside to long-term value creation from further efficiency capture from continuous focus on cost reduction and potential opportunistic M&A.”

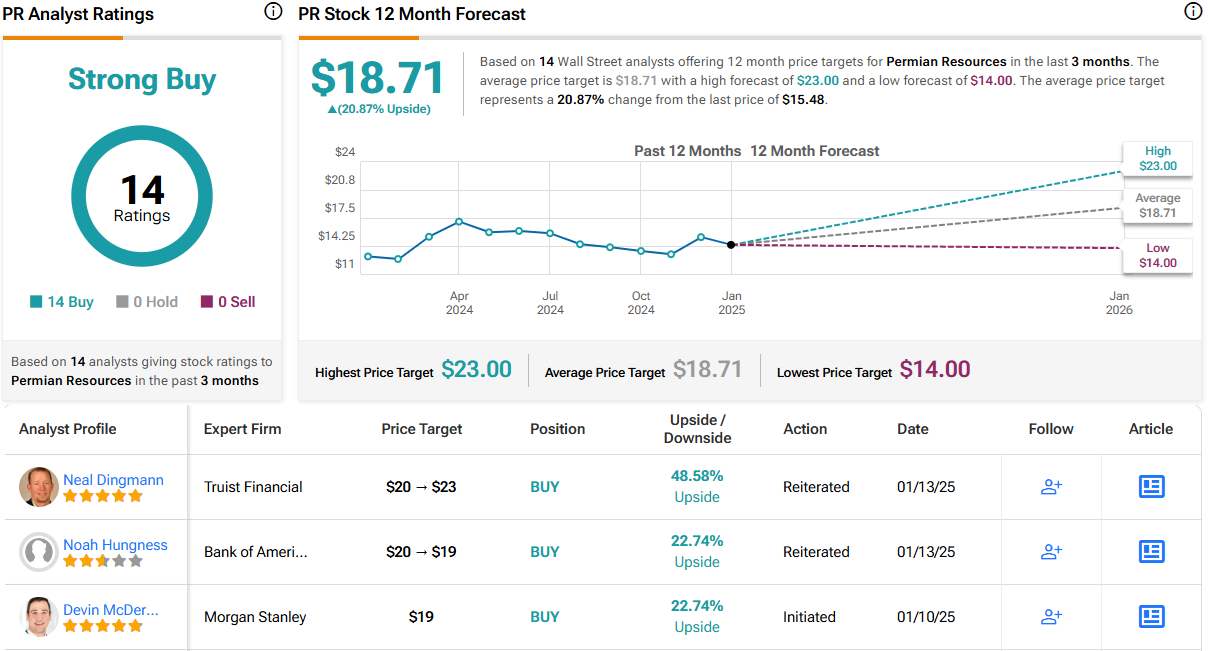

McDermott goes on to rate these shares as Overweight (i.e., Buy), with a $19 price target that implies a one-year upside potential of 23%. (To watch McDermott’s track record, click here)

This stock’s Strong Buy consensus rating is based on 14 unanimously positive analyst reviews set in recent weeks. The shares are priced at $15.48, and their $18.71 average target price suggests a 21% gain in store for the year ahead. (See PR stock forecast)

Expand Energy (EXE)

Next on our list, Expand Energy, was known as Chesapeake Energy until last year. As of October 1, on completion of its merger with Southwestern Energy, the company rebranded – and took its place as one of the largest natural gas producers in the US. Expand is based in Oklahoma City, and its operations include natural gas exploration and production in the Marcellus Shale in Pennsylvania, the Marcellus and Utica Shales of Ohio and West Virginia, and the Haynesville formation in Louisiana. The Appalachian operations deserve special note, as Expand’s Marcellus Shale holdings allow the company to tap into one of the world’s richest natural gas plays.

In the last few years, we’ve all seen headlines about horizontal drilling and hydraulic fracturing. Both techniques allow E&P companies to maximize hydrocarbon recovery – and Expand uses both in its natural gas operations. The company leverages these techniques to increase production and extend the lifespan of its active wells, in some cases to as much as 40 years.

Expand is also an important player in the liquefied natural gas sector, or LNG. This is a vital segment of the global economy, as LNG operations process natural gas into a more export-amenable form and ship it around the world. Expand has access to or is planning a series of LNG facilities on the Gulf Coast, in both Louisiana and Texas, which it feeds from the operations listed above. The company currently delivers between 1.5 and 1.8 bcfe/d (billion cubic feet equivalent per day) of natural gas to these liquefaction facilities.

We should note here that Expand’s CEO said this month that the company is on track to increase its natural gas production to approximately 7 billion cf/day this year. This compares favorably to the company’s 3Q24 production average, which was ~6.75B cf/day of gas equivalent.

McDermott, in his coverage of EXE for Morgan Stanley, highlights the firm’s unique attributes. He notes, “EXE is differentiated by leading scale in the Haynesville and attractive FCF growth from rising prices and volumes in 2025-26 as deferred wells are brought online and synergies are realized. EXE is well positioned to answer the call on the next growth cycle of US gas supported by a diverse transportation portfolio and direct access to the Gulf Coast LNG corridor. The stock is pricing in ~$3.35/mmbtu long-run Henry Hub, ~7% below the 2025 strip and ~11% below our $3.75 long-term assumption.”

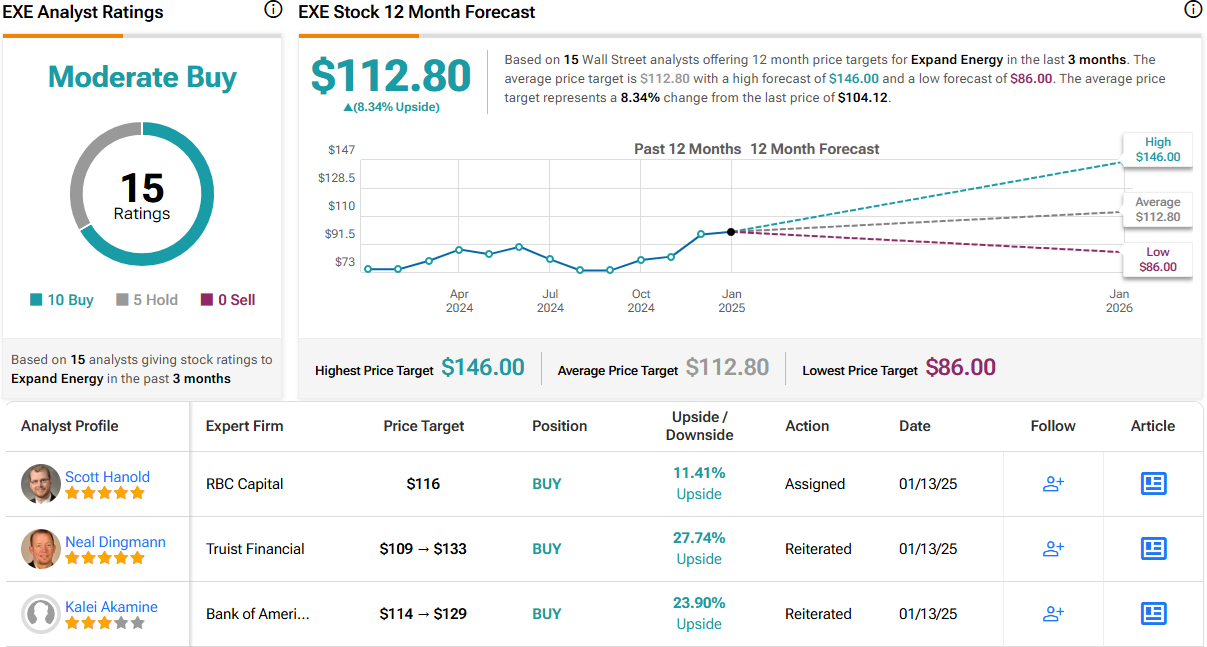

The analyst uses this stance to back up his Overweight (i.e. Buy) rating on EXE, and his price target, set at $127, reflects his confidence in a 22% upside potential on the one-year horizon.

Overall, this stock has picked up 15 analyst reviews recently, with a 10-to-5 split favoring Buy over Hold that gives the shares a Moderate Buy consensus rating. The stock is selling for $104.12, and its $112.80 average price target suggests that a 12-month gain of 8% is waiting in the wings. (See EXE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.