Two leading tech companies, Microsoft (MSFT) and Apple (AAPL), are battling for market share and investor capital. Typically, these two multibillion-dollar giants compete on software; both tend to outperform in retail and stock markets, but as of late, they’ve decoupled on their financials.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

As a result of my analysis, I am bullish on Microsoft and bearish on Apple because the former provides a shrewd long-term, growth-oriented capital allocation model, while the latter is overfocused on product quality and a closed ecosystem that stunts sales growth. My proprietary valuation model forecasts a 15% compound annual growth rate for MSFT over the next five years, compared to a mere 6.5% for AAPL over the same period.

Looking at the price action year-to-date, MSFT has outperformed AAPL significantly by recording a 1.3% gain, while the iPhone maker has slumped 11.3%.

Microsoft Asserts Strong Growth Prospects

Microsoft has delivered an uptrend in its revenue growth rates over the past 10 years, rising from a 13% 10-year annualized revenue growth rate to 16.4%. Moreover, the company has increased its free cash flow from 13.9% over 10 years to a one-year rate of 14.8%.

I predominantly attribute these sturdy growth trends to CEO Satya Nadella’s leadership and the company’s shrewd positioning in cloud infrastructure, which is further compounding with the advent of AI. Furthermore, Microsoft operates a business structure that gives its divisions greater control over products and services, opening up more accretive M&A activity compared to Apple’s closed ecosystem approach.

Microsoft’s agile and financially driven capital allocation model is perhaps most powerfully illustrated by its recent $14 billion investment in OpenAI. The deal put Microsoft in a unique position to integrate ChatGPT’s capabilities into its Azure Cloud and other service offerings. In contrast to Apple, Microsoft is at the forefront of AI-model development, contributing to a far brighter long-term investment outlook.

To further illustrate how Microsoft remains agile and delivers sustained growth over time, consider that it has made 25 divestments since its first acquisition in 1986. This reveals that the company is committed to a growth strategy reliant on innovation while shedding non-core or underperforming assets.

Valuation Gap Puts Microsoft in Pole Position

By January 2030, I expect Microsoft to generate ~$500 billion in annual revenue, with a net margin of 37.5% and around $187.5 billion in net income. The company’s diluted share count will likely be around 7.2 billion if management maintains its existing share buyback strategy. Therefore, my diluted earnings per share estimate for MSFT stock in five years is $26.

Notably, Microsoft’s five-year trailing price-to-earnings (P/E) ratio is 33.5, equating to a fair value price of $870 in 2030. The Windows maker’s stock is currently trading around $430, inferring a five-year compound annual growth rate of 15%.

To determine the fair value of a stock, I discount my price target back to the present using the average long-term annual return of the S&P 500 (SPY), currently at 10%. This accounts for the opportunity cost of not investing in the diversified index fund. Using this method, I estimate Microsoft’s intrinsic value at $540 per share. With the current stock price at $430, this implies a margin of safety of 20%, indicating that Microsoft is undervalued relative to its five-year growth potential.

Is Microsoft Stock Expected to Rise?

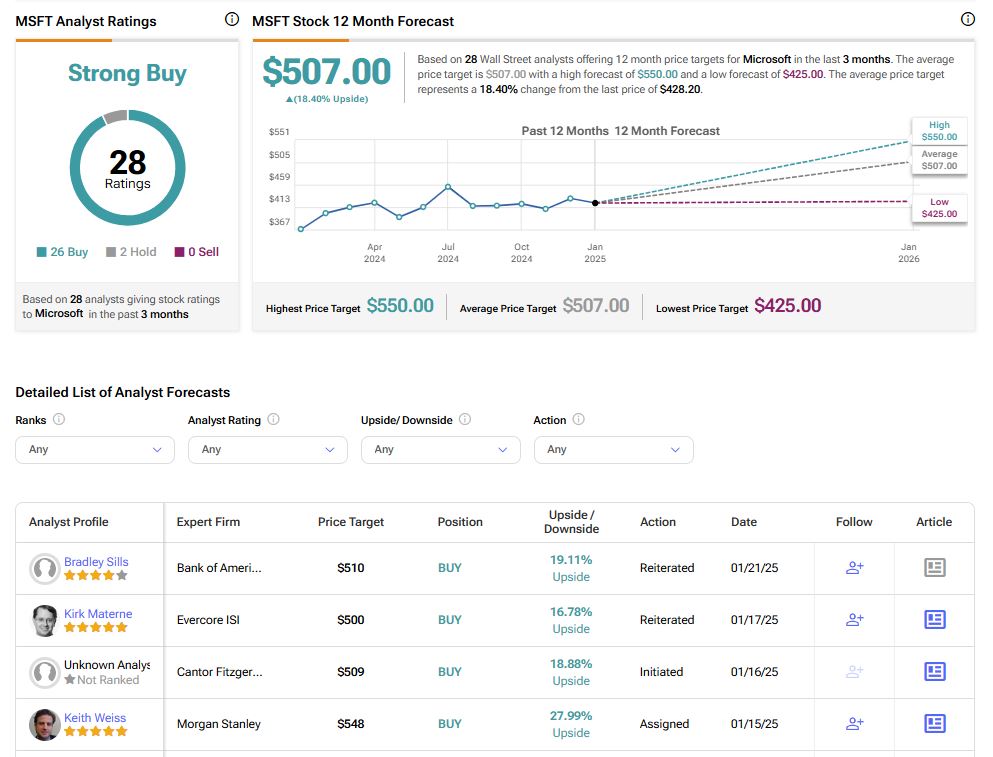

According to Wall Street analysts, Microsoft carries a Strong Buy rating based on 26 Buys and two Hold ratings. Notably, not a single analyst rated the stocks as a Sell. The average MSFT price target is $507 per share, indicating an 18.4% upside potential over the next 12 months.

Microsoft Leads as Apple’s Growth Slows

In contrast to Microsoft’s healthy revenue growth rates, Apple is seeing declining rates of growth. In fact, Apple’s 10-year annualized revenue growth rate is 13.4% compared to just 4.7% over the past year, which suggests underperformance. Moreover, the iPhone maker’s free cash flow is currently down to a 12.1% annual growth rate compared to 13.7% as a 10-year average. Even if this improves somewhat in the next few years, the company is unlikely to show a long-term growth uptrend.

As Apple’s growth tapers off, end-user consumers and investors are wising up to the fact that Apple’s flagship product — the iPhone — struggles to generate the margins it once did now that the smartphone market has saturated. To fight back against a rising tide, Apple is focusing on emerging markets and breaking ground in less lucrative segments to rediscover its successes from yesteryear. As a brief case in point, iPhone sales fell by 2% in 2024 while the global smartphone market grew by 4%.

Meanwhile, in the largest consumer market in the world, China, the iPhone has been overtaken by savvier peers such as Huawei and Vivo, thereby eroding Apple’s market share over time and directly proving that Apple’s once-held smartphone dominance is over. In 2024, Apple’s iPhone sales in China declined by 17% as competitors banked market share at Apple’s expense.

Given the stagnation in core product growth, I am bearish on Apple in the medium-long term. My sentiment is further corroborated by Apple’s toppy valuation, suggesting the company is now heavily dependent on intangibles for its short and long-term success.

Capital Strategies Spark MSFT and AAPL Divergence

I forecast Apple to post revenues in the region of $570 billion with a net margin of 25% within five years. If correct, this equates to a net annual income of $142.5 billion. Given management’s heavy share buyback strategy, Apple will likely have around 13.5 billion diluted shares outstanding in five years, which suggests Apple will end up with diluted earnings per share of ~$10 in 2030.

Also, I consider Apple’s price-to-earnings ratio of 37.5 to be too high and well above its five-year average. Assuming a P/E ratio of 30, Apple’s expected share price in 2030 would be around $315.

Apple is currently trading at approximately $220 per share, which implies a compound annual growth rate (CAGR) of 6.5% in my model. By discounting my price target to the present using the long-term yearly average return of the S&P 500 (10% as the discount rate), I calculate Apple’s intrinsic value to be $195 per share. With the current stock price at $220, the margin of safety is negative at -13%, indicating that the market is overvaluing Apple relative to its five-year growth potential.

Is Apple Stock a Buy or a Hold?

Turning to Wall Street, Apple has a Moderate Buy rating based on 19 Buy, seven Hold, and three Sell ratings. The average AAPL price target is $244.36, indicating an 11% upside potential over the next 12 months.

MSFT Wins the Tech Titan Battle with AAPL

Consumers and investors alike have realized that Apple’s bullish run is slowing. Both as a short-term speculative trade or a long-term investment, MSFT is currently better positioned than AAPL for sustained investor returns through 2025 and beyond. My valuation model points to a distinct advantage for MSFT, wielding a 15% compound annual growth rate over the next five years, compared to a mere 6.5% for AAPL. Once other capital-related, operational, and analytical factors are factored in, Microsoft stands out as the clear investment case winner over Apple in early 2025.