Despite being the world’s numero uno stock for the longest time, Microsoft (MSFT) stock has recently underperformed the S&P 500 (SPX). A weaker-than-expected Azure outlook overshadowed Microsoft’s otherwise strong earnings, causing it to drop to the position of the third-largest company by market cap. The question now is: can Microsoft reclaim its number-one spot? I believe that concerns over AI investments and growth outlook are temporary.

Confident Investing Starts Here:

- Easily unpack a company's performance with TipRanks' new KPI Data for smart investment decisions

- Receive undervalued, market resilient stocks right to your inbox with TipRanks' Smart Value Newsletter

Microsoft’s long-term outlook remains strong, as the company is well-positioned to capitalize on AI growth and realize the benefits of its substantial investments in this space.

Microsoft’s AI Capital Investments Continue to Rise

One key reason for Microsoft’s weakness is that the company continues to aggressively invest in AI infrastructure. The investor community is eager to see how these investments translate into monetization and improved profitability.

For example, during FY2024, Microsoft’s capital expenditures (CAPEX) surged 58% year-over-year to $44.5 billion. However, the margins of its cloud segment declined, coming in at 71% in the most recent fiscal first quarter compared to 73% a year earlier. While cloud revenue grew by an impressive 20% year-over-year, this growth failed to translate into higher margins, leaving investors disappointed.

Further adding to concerns, management has projected that CAPEX will rise even higher in FY2025 than in FY2024. If revenue growth and margins do not keep pace with these investments, Microsoft’s profitability could face pressure.

Azure Growth Outlook: A Short-Term Concern

MSFT stock has recently faced a dual challenge: rapidly increasing capital investments in AI infrastructure and a short-term unpromising AI growth outlook, leaving investors uneasy.

The company has provided a conservative outlook for Azure, citing supply and capacity constraints. However, these constraints are expected to ease as Microsoft’s substantial capital expenditures take effect. Despite the challenges, Azure revenues exceeded the company’s projections for the quarter. This indicates the concerns are temporary, driven by capacity limitations rather than a lack of demand.

Investors’ worries may be more emotional than factual. AI growth trends can fluctuate based on capacity availability and broader macroeconomic sentiment. In the long run, however, AI remains a transformative opportunity, representing the fastest-growing business segment for Microsoft and its AI peers.

Long-Term AI Growth Potential Remains Intact

At its recent Ignite event, Microsoft outlined its AI growth strategy, which may include increased M&A activity to enhance its AI-related products and services. The company also introduced two new customizable AI chips—the Azure Integrated HSM and the Data Processing Unit (DPU)—designed to accelerate AI operations and strengthen data security at its data centers.

Notably, AI demand remains robust, as evidenced by impressive commercial bookings. In Q1 FY2025, Microsoft reported a 30% year-over-year increase in AI service bookings.

Azure growth is also expected to accelerate in the coming year as production of AI chips ramps up. This development will likely bring the company closer to achieving its $10 billion annual run rate in AI revenues.

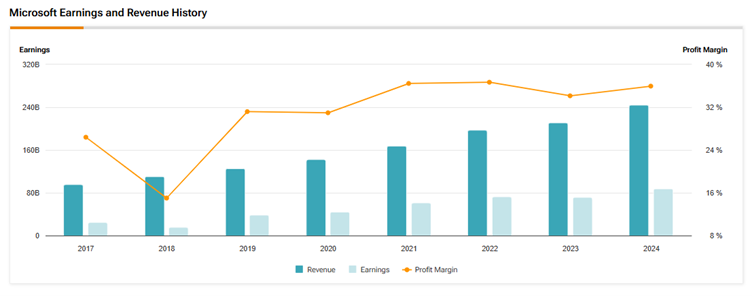

To get a clearer picture, Microsoft’s performance over the past seven years highlights its impressive trajectory. Revenues more than doubled from $97 billion in FY2017 to $245 billion in FY2024, reflecting a compound annual growth rate (CAGR) of 14.2%. What’s even more applaudable is earnings have more than tripled from $25 billion to $88 billion over the same period, achieving a CAGR of 19.7%, driven by strong profit margins.

This data reinforces my confidence in Microsoft’s solid business fundamentals and its consistent growth trajectory. With the company’s fastest-growing AI segment poised to make incremental contributions to revenue and margin growth, it’s only a matter of time before these investments yield substantial results.

MSFT’s Weak Azure Outlook Overshadowed an Otherwise Upbeat Quarterly Print

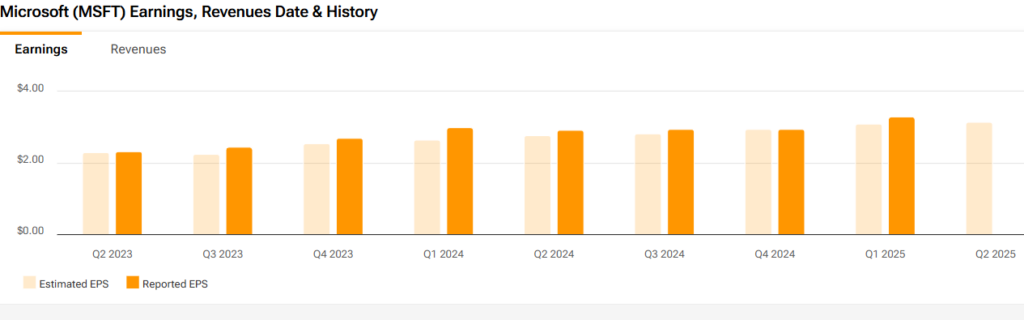

On October 30, Microsoft reported better-than-expected Fiscal Q1 results for the ninth consecutive quarter, exceeding analyst expectations. Adjusted earnings of $3.30 per share were 20 cents cent ahead of analysts’ estimates of $3.10. Also, earnings jumped 10.37% year-over-year compared to $2.99.

Further, revenues soared 16% year-over-year to $65.6 billion. Despite an overall strong quarter, MSFT shares slid due to a revenue outlook that failed to meet Wall Street expectations.

The Intelligent Cloud business segment, encompassing Azure Cloud, SQL Server, and Windows, among others, witnessed an increase of 20% year-over-year to $24.1 billion. However, Azure and other cloud services stood out, delivering 33% revenue growth, exceeding the company’s forecasted range of 28% to 29% and surpassing the prior quarter’s 29% growth. Azure’s growth was fueled by strong momentum in OpenAI, with usage doubling over the past six months.

Despite the sequential growth in Azure, investor sentiment was dampened by Microsoft’s muted guidance for fiscal Q2. Azure revenue is projected to grow 31% to 32% in constant currency, falling short of expectations. On the bright side, Microsoft anticipates faster Azure growth in the second half of fiscal year 2025, providing a more optimistic long-term outlook.

Microsoft’s Valuation Isn’t Cheap but Isn’t Expensive Either

Despite being the third most valuable stock in the world, Microsoft’s valuation isn’t as expensive as one might think. At first glance, it may look expensive, trading at a forward P/E of 32x. Nonetheless, I believe the valuation premium is justified, given its favorable industry-leading market position, strong margins, diversified revenue stream, and huge exposure to high-growth AI and cloud businesses.

For comparison, Azure competitor Amazon (AMZN), an online retail and cloud computing giant, is trading at a P/E of 39x, while Apple (AAPL) is trading at a 31x forward P/E.

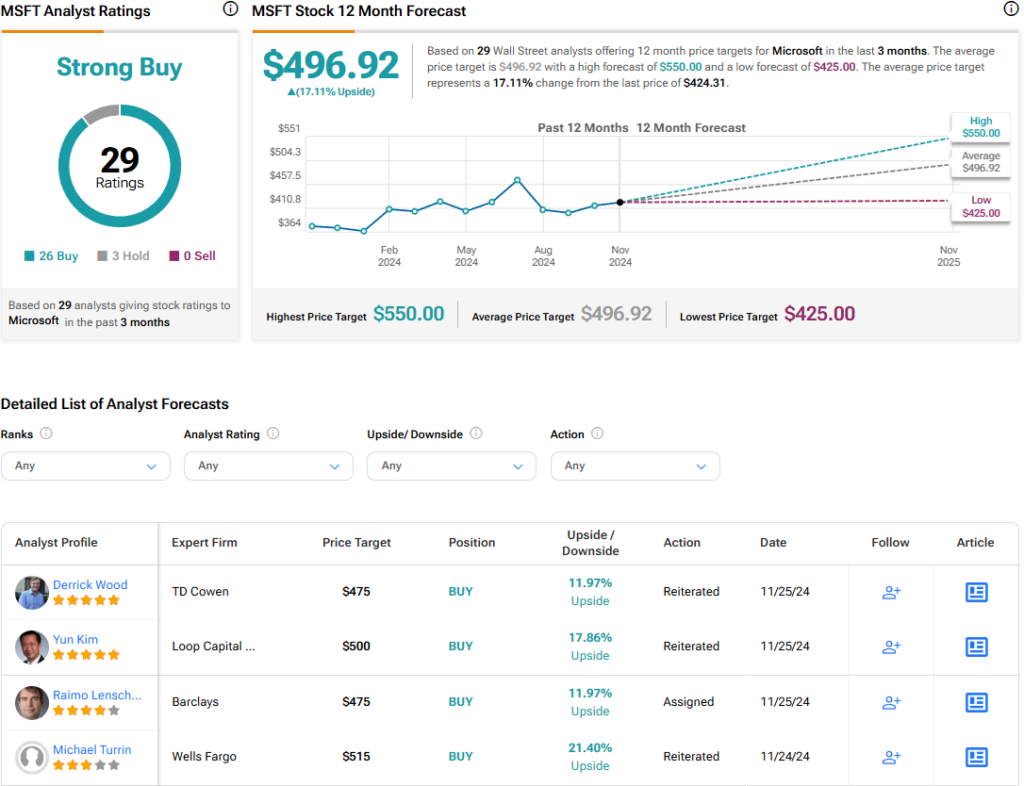

Is Microsoft Stock a Buy, According to Analysts?

Wall Street analysts continue to be bullish on Microsoft stock, despite some lowering their price targets after the earnings report. Overall, the stock commands a Strong Buy consensus rating based on 26 Buys and three Holds assigned in the past three months. Microsoft stock’s average price target of $496.92 implies a 17.11% upside potential from current levels.

Conclusion: Consider Buying MSFT for Long-Term Growth

Despite recent stock price weakness and a softer-than-expected Azure outlook, Microsoft’s long-term growth potential in AI remains strong, supported by its substantial investments in the space. I believe the market has overreacted, and Azure is poised to remain a key driver of revenue and profitability for Microsoft over the long term.

As such, the recent dip in MSFT’s stock should be viewed as a strategic buying opportunity for investors with a long-term perspective.