Stock analysis is all about predictions – but as wits from Mark Twain to Yogi Berra have reminded us, predictions are hard, especially when they’re about the future.

That’s why a recent market outlook from Fundstrat’s Tom Lee was so surprising. Lee, long known for his bullish views on stocks, is predicting that the S&P 500 could hit as high as 15,000 by 2030 – that is, nearly triple its current reading of 5,491.

Lee points at several factors to support his view, including demographics and technology. He believes that as the millennial and Gen Z cohorts reach their 30s and older – the prime years for taking on debt, making large purchases, and buying into risk-friendly investments – their economic activity will provide a boost to the stock markets. In addition, Lee believes that technological advances, and greater productivity, will more than compensate for potential labor shortages.

This raises an important point, namely, if the market is on track for long-term gains of this magnitude, then the time to buy is now. Some of Wall Street’s analysts are following that logic, and are picking out ‘Strong Buy’ S&P 500 stocks – but not just any such stocks, the ones with high upside potential. Using the TipRanks platform, we’ve pulled up the broader views on two of these picks, to find out just what makes them so compelling.

Micron Technology (MU)

We’ll start in the tech industry, with a semiconductor chip company. Micron Technology, from its base in Boise, Idaho, is a ~$100 billion player in the chip field, with a reputation for designing and distributing high-quality memory chips. The company was founded in the late 70s and has more than 45 years of experience on the cutting edge of tech. Micron’s current product lineup includes 9th generation NAND chips, DRAM memory solutions, and flash-based SSDs for optimized storage solutions at any scale. The company boasts that its memory technologies have helped enable the rapid recent growth of generative AI and real-time natural language processing systems.

Micron has a reputation as an innovator, and it has applied that to its AI-capable chips. The company’s products are found in numerous AI-related applications, from autonomous cars to IoT. At the same time, Micron remains a major supplier of memory storage, its core business. Micron is well-known as a supplier of SSD drives and storage chips for the PC industry, and the company’s NAND and DRAM product lines remain staples of its business, which is substantial. While not the largest chip maker on the global scene, Micron is still ranked a respectable 12th by market cap and 11th by revenue when compared to its peers.

A couple of Micron’s recent announcements show how the company is keeping itself at the forefront of its industry. At the beginning of August, Micron announced that it had developed PCle Gen 6 data center SSD technology, an industry first, which was added to its portfolio of AI-supporting products. And, just before that, at the end of July, the company began shipping out its 9th generation TLC NAND technology – again, an industry first.

Turning to the company’s financial side, we find that Micron reported $6.81 billion at the top line in its fiscal 3Q24 report (May quarter), the last released. That figure was up more than 81% year-over-year, and beat the forecast by $140 million. At the bottom line, Micron’s non-GAAP earnings came to 62 cents per share, 9 cents ahead of the estimates. In another important metric, the company’s operation cash flow for the quarter hit $2.48 billion, more than double the $1.22 billion from fiscal Q2 – and far higher than the $24 million reported in the prior-year period. The company credited the strong quarter to robust demand for AI-capable products and strong execution.

This stock is covered by Susquehanna’s Mehdi Hosseini, who lays out the clear bull case, despite the current bumpy terrain. The 5-star analyst writes, “The Memory is currently in a ‘mid-cycle’ correction in the middle of a longer up-cycle… Despite this ‘mid-cycle’ correction, we argue that for the first time in the history of Memory Industry, DRAM is structurally benefiting from successive generation of HBM products, preventing the ‘commoditization’ while NAND benefits from limits in bit supply growth. As such, and with the underlying assumption that the tight supply-demand dynamics sustaining into 2026 (yes, a 3-yr up-cycle), combined with the recent pull back makes MU risk/reward profile attractive.”

These comments back up Hosseini’s Positive (Buy) rating on MU, while his price target of $175 points toward a robust 96%-plus upside potential for the next 12 months. (To watch Hosseini’s track record, click here)

Overall, Micron gets a Strong Buy consensus rating from the Street, based on 27 recent analyst recommendations that include 25 Buys to just 2 Holds. The shares are priced at $89.39 and their average target price of $166.38 suggests that a gain of 86% lies in store for the year ahead. (See Micron stock forecast)

Dexcom, Inc. (DXCM)

The second stock we’ll look at is Dexcom, a medical device company working on the design, manufacture, and distribution of continuous glucose monitoring systems (CGMs), a high-end device used by patients to manage diabetes. CGMs are especially useful for diabetics with an insulin-dependent condition who self-administer their medication.

Dexcom has become a leader in the field of diabetic monitoring technology. From its base in San Diego, the company has put together a line of CGM devices that it continually upgrades. The latest version, the G7, is Dexcom’s most accurate CGM to date. The G7, like its predecessors, uses a simple sensor patch placed on the upper arm and can be monitored through a smartphone or smartwatch app that is compatible with both the Android interface and Apple’s iOS. Patients can use it to monitor glucose levels without resorting to finger-prick blood tests, a known bane for long-term diabetes patients. In addition, the system can give patients alerts for high or low blood sugar levels, notify them of routine insulin dose scheduling, and can even customize these notifications to account for work schedules, changes in meal patterns, or even the shift from the work week to the weekend.

Earlier this summer, Dexcom began marketing its Stelo biosensor patch as an over-the-counter product. This patch uses the same technology as the biosensor patch in the G7 CGM, but is tailored for patients with type-2 diabetes who do not use insulin injections. The patch fits on the upper arm, can be linked to smart devices, and provides a steady stream of bio data to help patients manage their diabetes through diet and other daily activities or medications. The Stelo patch is the first such device available in the US markets without a prescription.

Dexcom released its last set of financial results, covering 2Q24, toward the end of July – and the results were mixed. At the top line, second quarter sales came in at $1 billion, up almost 15% year-over-year, although the figure missed the forecast by $40 million. The company’s earnings, by non-GAAP measures, came in at 43 cents per share, 4 cents per share better than had been anticipated.

Those mixed results, however, did not justify the stock falling by more than 40% in the wake of the release. That was down to the company’s disappointing outlook. Dexcom published Q3 revenue guidance in the range of $975 million to $1 billion, where the consensus had hoped to see $1.15 billion. Full-year 2024 revenue was guided toward a $4 billion to $4.05 billion range, while analysts had expected $4.33 billion.

While the stock fell on the guidance miss, BTIG analyst Marie Thibault still sees Dexcom as a sound option for investors. She expects that the company has multiple routes toward further growth and writes, “DXCM has several growth opportunities, including continued insulin-intensive adoption, the basal-only user, Stelo OTC CGM, and expansion in international geographies like Japan. Assessing MedTech peers that have mid-teens sales growth, we see that these companies trade near an average ~7x NTM EV/Sales. We think DXCM does still deserve a premium to these peers, since it is more profitable than most, retains a strong position in a market duopoly, and has a path back to higher growth.”

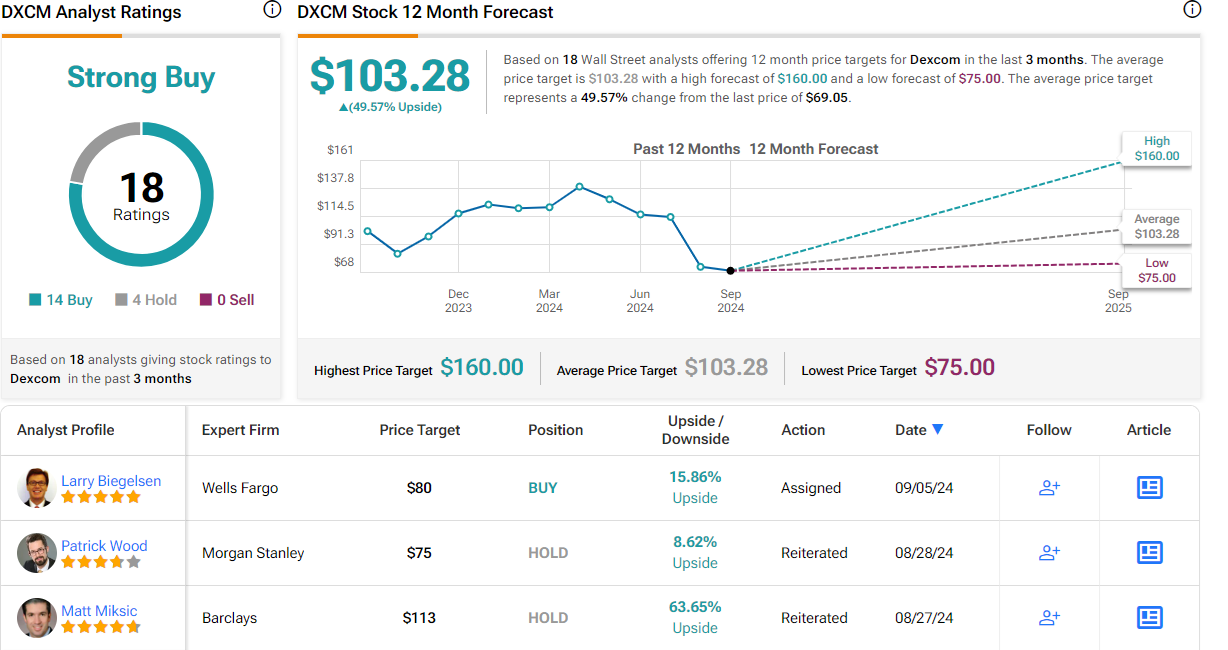

Looking ahead, Thibault rates DXCM as a Buy, and she complements that rating with a $120 price target that suggests a one-year upside potential of 74%. (To watch Thibault’s track record, click here)

There are 18 recent analyst reviews on record for Dexcom shares, and the 14 to 4 split between Buys and Holds supports the Strong Buy consensus rating. The shares are currently trading for $69.05 and have an average target price of $103.28, implying that the stock will gain 49.5% by this time next year. (See Dexcom stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.