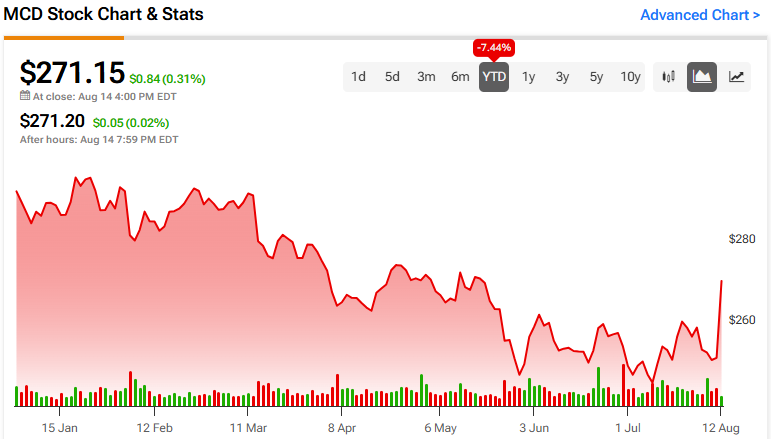

McDonald’s (MCD) shares have declined by 7.4% year-to-date, mainly due to enduring bearish sentiment sustained by decelerating comparable sales, which even dipped into negative territory in its most recent Q2 results. This, in turn, can be largely attributed to wider industry trends and factors beyond McDonald’s control. Despite this, the company is on track to see record sales and near-record earnings this year, all while trading at an attractive valuation. Thus, I am bullish on MCD stock and believe it is a compelling buy at its current levels.

Discover the Best Stocks and Maximize Your Portfolio:

- See what stocks are receiving strong buy ratings from top-rated analysts.

- Filter, analyze, and streamline your search for investment opportunities with TipRanks’ Stock Screener.

Geopolitics and Inflation Impact Revenue Growth

At first glance, McDonald’s Q2 revenue growth appeared relatively soft. The company’s revenues held steady at $6.5 billion, showing no year-over-year increase and continuing a trend of slowing growth seen in recent quarters. Despite ending the quarter with 42,406 locations – an increase of 1,605 from last year, which contributed to the top line -this expansion was offset by a 1% drop in global comparable store sales. This decline was observed across key markets, including the U.S., Australia, Canada, and Germany.

However, there’s more to the story, as McDonald’s decline was not the result of any notable operational missteps. Instead, it was influenced by various external factors beyond the company’s control. The negative comparable sales were primarily driven by macroeconomic pressures and geopolitical tensions that affected the entire quick-service restaurant (QSR) industry.

For example, enduring inflationary pressures have been a significant challenge. In many of McDonald’s core markets, inflation rates have soared between 20% and 40% over the past few years, straining consumer purchasing power and altering dining habits. This inflation surge forced consumers to reconsider their spending and opt for more budget-friendly dining options. As a result, McDonald’s experienced reduced traffic and lower sales per visit.

Additionally, geopolitical tensions, particularly the ongoing conflict in the Middle East, compounded these challenges. The instability in these regions has led to decreased consumer spending and weakened traffic at McDonald’s restaurants in that area, resulting in revenue decline.

MCD’s Financials and New Initiatives

In addition to McDonald’s somewhat disappointing top-line metrics, its earnings also weakened. This decline was largely due to inflationary pressures driving up costs, which, coupled with decreasing same-store sales, led to shrinking restaurant-level margins. The company reported adjusted earnings per share (EPS) of $2.97, marking a decline of about 5% compared to last year in constant currencies. This decline was also affected by a higher effective tax rate and higher interest expenses, which grew by 13% to $373 million.

That said, I remain bullish on the stock and believe McDonald’s overall results and earnings are set to rebound rapidly. This is because the company is actively addressing the current challenges. For instance, to manage the current consumer price sensitivity, McDonald’s has introduced initiatives like the $5 meal deal in the U.S., which has shown positive results and is being expanded nationwide.

Additionally, McDonald’s is revitalizing its menu with new items, such as The Big Arch burger, to attract more customers and increase foot traffic in its restaurants. The expansion of its loyalty program, now numbering 166 million members, also supports its goal of increasing customer retention and market share.

Along with easing inflation, foot traffic is anticipated to increase during the latter half of the year. Wall Street forecasts full-year sales of about $26.1 billion, which translates to a 2.3% year-over-year increase and implies a rebound in sales growth for the second half of the year. This estimate also suggests the company is on track to set a new revenue record despite the current challenges and prevailing market pessimism.

Additionally, adjusted EPS is expected to land at $11.81, indicating a mere 1.1% decline from last year’s record of $11.94. Finally, the market anticipates solid single-digit growth in both revenue and EPS for FY2025 and FY2026, signaling a steady recovery.

MCD’s Valuation

Another reason for liking the stock right now is its valuation. Following the share price decline over the past year, McDonald’s seems to be trading at a fairly attractive valuation. Based on Wall Street’s adjusted EPS estimate of $11.81, McDonald’s is trading at a forward P/E of about 23x, which I find quite compelling, given its robust brand value and impending revenue and EPS growth rebound.

Historically, McDonald’s stock has commanded premium multiples. I believe that as revenues and EPS return to an upward trajectory, investor confidence will likely recover. This will likely lead to potential returns driven by the company’s underlying growth and the opportunity for a multiple P/E expansion..

Is MCD Stock a Buy, According to Analysts?

Despite Wall Street’s recent skepticism about the stock, McDonald’s retains a Moderate Buy consensus rating. This rating is based on 19 Buys and eight Hold ratings assigned in the past three months. At $302.13, the average MCD stock price target suggests an 11.4% upside potential.

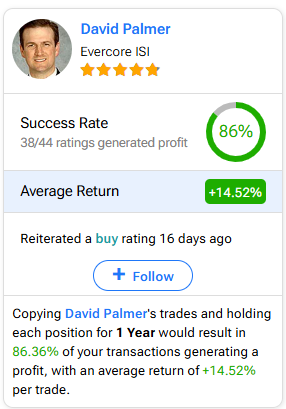

If you’re wondering which analyst to follow for buying or selling MCD stock, David Palmer from Evercore ISI stands out as the top choice. Over the past year, he has achieved an impressive average return of 14.52% per rating, with a remarkable 86% success rate. Click on the image below to discover more about his insights.

Takeaway

Despite recent challenges, including falling comparable sales and dipping earnings due to external factors like inflation and geopolitical tensions, McDonald’s is on track for record sales and near-record earnings this year. Further, the company’s proactive initiatives to address inflationary pressures and improve foot traffic, along with its historically robust brand, suggest a potential revenue and EPS growth rebound. I believe that McDonald’s valuation is attractive and doesn’t fully price in these factors – hence my bullish view of the stock.