In this piece, I evaluated two fast-food stocks, McDonald’s (MCD) and Restaurant Brands International (QSR). A closer look suggests a bullish view of McDonald’s and a neutral view of Restaurant Brands.

Known for its signs with the golden arches, McDonald’s is one of the most widely recognized fast-food chains in the world, operating and franchising more than 30,000 locations in over 100 countries around the globe. Meanwhile, Restaurant Brands International operates multiple fast-food chains, including Burger King, Popeye’s, and Tim Horton’s.

Shares of McDonald’s have tumbled 8% year to date and are off 4% over the last year, while Restaurant Brands stock is also down 8% year to date, although it’s roughly flat over the last 12 months.

Although both stocks are down by matching percentages year to date, there’s a meaningful gap in their valuations. We compare their price-to-earnings (P/E) ratios to gauge their valuations against each other.

The overall valuation of the restaurant industry is skewed due to extreme P/E ratios on names like Cava Group (CAVA), which is trading at a P/E of around 223.2x. Thus, a comparison with the rest of the industry is not really helpful because both companies are legacy operators rather than rising stars in the market.

McDonald’s

At a P/E of 23.6x, McDonald’s is trading at a premium to Restaurant Brands. However, since it’s trading near the lower end of its usual valuation range and has shown long-term share-price gains, a long-term bullish view looks appropriate.

McDonald’s mean P/E range since October 2019 is 28.4x, but that includes quite a bit of ups and downs around the pandemic. More recently, the fast-food giant appears to have bottomed at a P/E of around 21 in early July, and its range since plunging in August 2021 has been 21x to about 35x.

Additionally, McDonald’s just looks like a safe investment through economic slowdowns, as the shares are up 39% over the last five years and 269% over the last decade. Typically, consumers turn to low-cost dining options when their wallets are feeling the pinch, and McDonald’s certainly fits the bill.

As such, there’s been lots of talk about the chain’s new $5 menu, which management told franchisees in a memo is beginning to reverse their traffic slump. They reported a “notable” increase in diner traffic and said that the $5 menu is starting to pull customers from rival chains.

McDonald’s reported an “incremental lift” of almost 3% in guest counts during the promotion. In fact, management said more diners had tried the deal than they had previously expected.

While this is a short-term answer to the problem, the consumer confidence index fell to 100.4 in June from May’s reading of 101.3 as Americans became concerned about their prospects in the near term. Notably, the $5 promotion started in late June.

Additionally, the measure of expectations for income, business, and the job market ticked down from 74.9 in May to 73 in June. Anything below 80 suggests a recession could be around the corner.

Thus, it seems like McDonald’s is prepared to weather the storm of another economic downturn, and the current dive in its stock price and valuation looks like a buy-the-dip opportunity.

What is the Price Target for MCD stock?

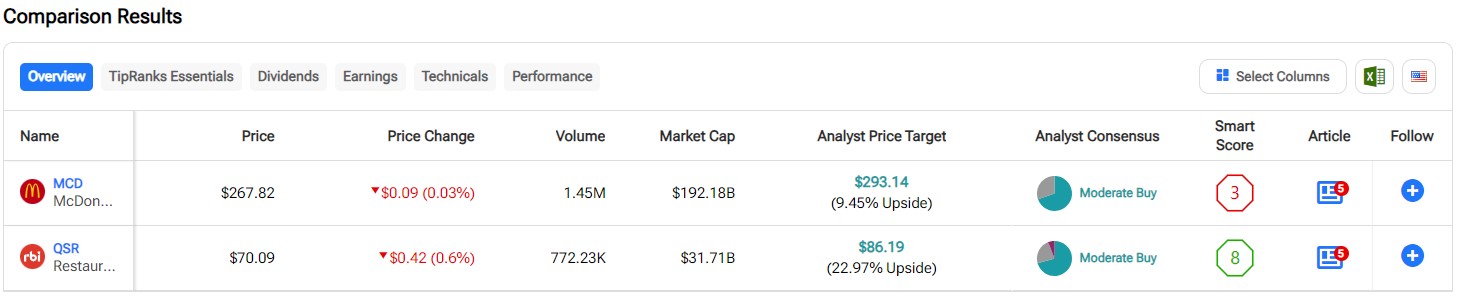

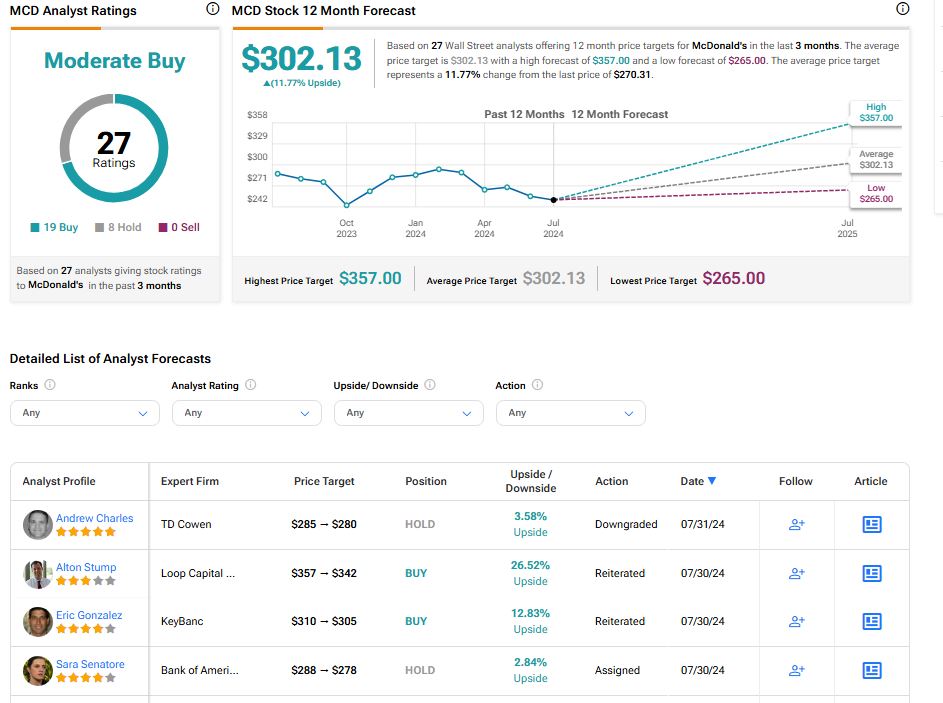

McDonald’s has a Moderate buy consensus rating based on 19 Buys, eight Holds, and zero Sell ratings assigned over the last three months. At $302.13, the average McDonald’s stock price target implies upside potential of 11.77%.

Restaurant Brands International

At a P/E of about 17.4x, Restaurant Brands International shares tend to be less volatile than McDonald’s shares. They’ve also been trading at the bottom of their range since August 2021, so a neutral view seems appropriate.

Over that time frame, Restaurant Brands shares have usually traded between 17.4x and about 23.8x, except for a spike that carried them to about 30x in January. Some investors may consider a bullish stance on the stock, as there is a meaningful upside here. However, another consideration is that the company’s long-term share price gains are far less than those of McDonald’s.

Restaurant Brands stock is only up 13% over the last five years and 149% over the last 10 years, so there may be less upside in the shares versus McDonald’s stock over the long term.

Additionally, if McDonald’s $5 menu continues to steal customers from Restaurant Brands’ chains, it could be detrimental in the near term. Meanwhile, Restaurant Brands’ Burger King was one of the first to offer a $5 menu in the summer.

However, its U.S. same-store sales were roughly flat for the summer quarter, suggesting consumers see more value in the $5 menu from McDonald’s.

What is the Price Target for QSR stock?

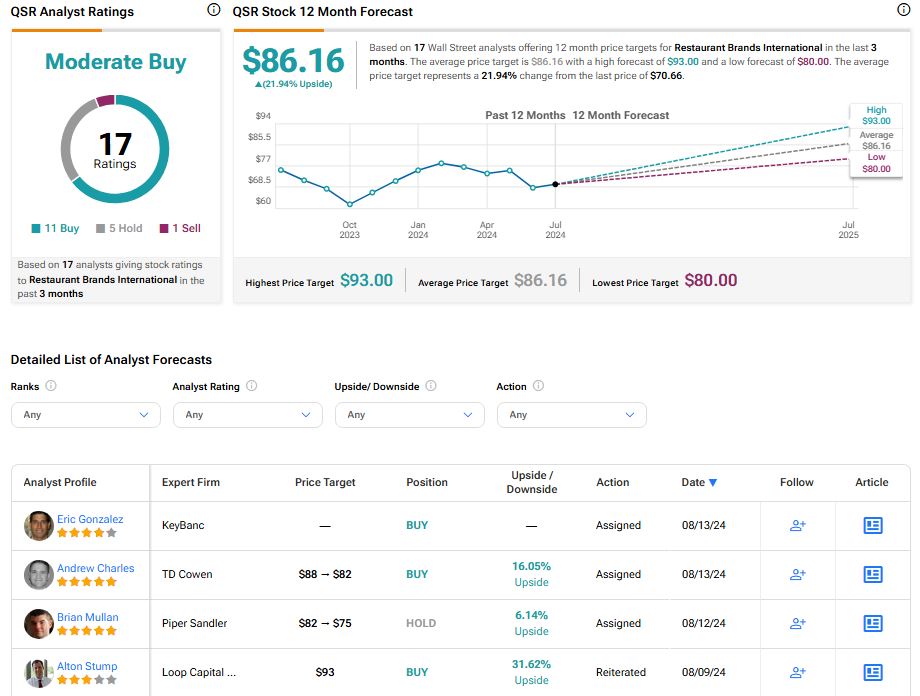

Restaurant Brands International has a Moderate Buy consensus rating based on 11 Buys, five Holds, and one Sell rating assigned over the last three months. At $86.16, the average Restaurant Brands stock price target implies upside potential of 21.94%.

Conclusion: Bullish on MCD, Neutral on QSR

While both McDonald’s and Restaurant Brands International have shown signs of stability during economic downturns, McDonald’s simply looks like the better player in the fast-food space. There’s more upside potential in the shares based purely on the stock’s trading range, and it has gained more over the long term than Restaurant Brands stock has.