Match Group, Inc. (MTCH), the global leader in online dating, sued Alphabet Inc. (GOOGL) on May 9 in light of restrictive policies introduced by Google. These included the decision to exert pressure on developers to use Play Store Billings for subscription services.

Maximize Your Portfolio with Data Driven Insights:

- Leverage the power of TipRanks' Smart Score, a data-driven tool to help you uncover top performing stocks and make informed investment decisions.

- Monitor your stock picks and compare them to top Wall Street Analysts' recommendations with Your Smart Portfolio

The lawsuit claims Google is engaging in anticompetitive behavior to retain its monopoly on the Android platform, by requiring developers to use Google’s billing system and share a percentage of sales to gain access to the Play Store. Google has also announced plans to remove apps that breach its billing policies.

Match Group, on May 20, announced that Google has temporarily agreed to allow alternate billing systems by not enforcing the mandatory use of Google Play Billing. This is a positive development for Match, but the company is not out of the woods yet as this is not a permanent agreement. As discussed below, Match Group faces many other challenges in the post-pandemic era as well. Despite the threat posed by these challenges, I am bullish on the company’s long-term prospects.

The Dispute Will Continue

On Android-based smart devices, the Google Play Store is often regarded as the safest and preferred app distribution channel. With over 90% of all Android app downloads being completed through the Google Play Store, it is undoubtedly a powerful and influential tool. The company store also collects fees from developers, making it a lucrative revenue stream for GOOGL.

Although Google initially required only certain types of in-app payments to be made through its billing service, the company announced in 2020 that all apps selling digital products must utilize its billing system. This allowed Google to earn up to 30% in commissions on each Play Store digital purchase.

In March 2021, however, Google reduced its fees to 15% for the first $1 million a developer generates through sales. According to Google, reducing fees equally for all companies was a reasonable way to assist developers of all sizes. Despite this, Match Group accuses Google of using a “bait and switch” approach to deceive developers about its payment policies. Google, in response, said that it charges for providing services similar to any other business and that Match Group’s move is a “self-interested campaign” to avoid fee payments.

Following complaints from app developers and legislators, both Google and Apple, Inc. (AAPL) have changed their app payment policies in recent years. However, developers claim these changes are inadequate to address concerns raised by them. With Match Group filing a lawsuit against Google, authorities in the Netherlands started a preliminary investigation into Google’s suspected anticompetitive actions. The regulatory body has also ordered Apple to allow dating applications to accept alternative payment methods and imposed a series of fines after the company refused to comply with this decision.

Taking into account these recent developments, it seems reasonable to believe that Match Group and Google are unlikely to reach a permanent solution any time soon, which in turn will keep Match Group stock under pressure.

Growth Might Hit a Wall This Year

On May 3, Match Group reported first-quarter earnings of 60 cents per share, beating analyst expectations of 53 cents. Revenue came to $799 million, up 20% year-over-year with paying subscribers jumping 13% to 16.3 million. Tinder accounted for 10.7 million of those payers, representing a 1% increase from the previous quarter. The total revenue per payer (RPP) also increased by 6% to $16.

Match Group has experienced double-digit revenue growth over the last three years, but the company is facing several challenges that could limit growth in 2022.

Due to headwinds such as Russia’s invasion of Ukraine, new waves of COVID-19 infections, and the strengthening of the U.S. dollar, Match expects revenue to rise around 14% in the second quarter against Wall Street expectations for 18% growth. The company expects the Russia-Ukrainian war to cost approximately $10 million per quarter until the conflict is resolved.

The company’s operating margin was 26% in Q1, down 300 basis points from the previous quarter, and this could be an early indication of rising costs becoming a major headwind in the coming quarters.

Promising Regulatory Developments

Regulatory bodies in Europe and the U.S. are attempting to address the ongoing in-app payment issues resulting from Google’s policy changes, and the impending Digital Markets Act could help resolve some of these issues. However, this Act is not expected to come into effect in 2022, meaning Match Group still has a long way to go before securing regulatory support.

In the U.S., the Open App Markets Act, a bill introduced by the Senate Judiciary Committee in February, is also planning to address the anti-competitive practices in app markets. If passed into law, this will allow developers to use their own billing systems.

South Korea also approved a law in August 2021 requiring Apple and Google to allow developers to utilize third-party payment services.

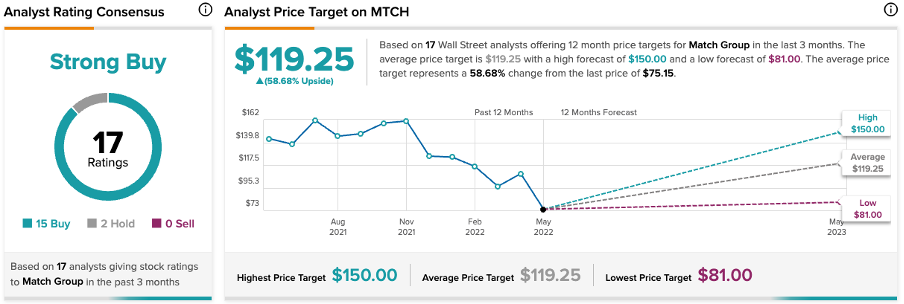

Wall Street’s Take

The recent pullback in the stock price has pushed Match Group into the undervalued territory. Based on the ratings of 17 analysts offering 12-month price targets, the average Match Group price target comes to $119.25, which implies upside of 59% from early Tuesday market prices.

Takeaway

Google is focused on leveraging its dominant position in the Android market by exerting pressure on developers to exclusively use Play Store Billing, which is becoming a hurdle for Match Group to grow. In the short run, Match Group will also come under pressure as the pandemic boon comes to an end with people embracing more traditional ways of meeting new partners, instead of digital channels.

Despite these headwinds, Match Group still is well-positioned to grow in the long run aided by the long runway for growth in markets outside the United States, particularly in Asia and Latin America. The company enjoys competitive advantages because of its massive scale and diversified services offering, and these will be catalysts for growth.

Discover new investment ideas with data you can trust

Read the full Disclaimer & Disclosure.