Markets have taken a pounding in recent sessions and investors are understandably nervous. The NASDAQ, which had been leading the markets’ recent gains, tumbled 8% in the last two days on fears over high valuations.

So, it’s time for defensive stocks. These are stocks that will provide your portfolio with a degree of insulation, protection from the negative chances inherent in the markets. Sometimes that protection comes in the form of high dividends, sometimes in the form of countertrend share appreciation, and sometimes it comes from a solid business foundation and cash-flow.

Therefore, today we’ll look at three defensive stocks that have been chosen as Top Picks by Wall Street analysts. These are buy-rated stocks that the analysts foresee having a 25% or better growth potential in the year ahead.

Using TipRanks’ Stock Comparison tool, we lined up the three alongside each other to get the lowdown on what the near-term holds for these Dow players.

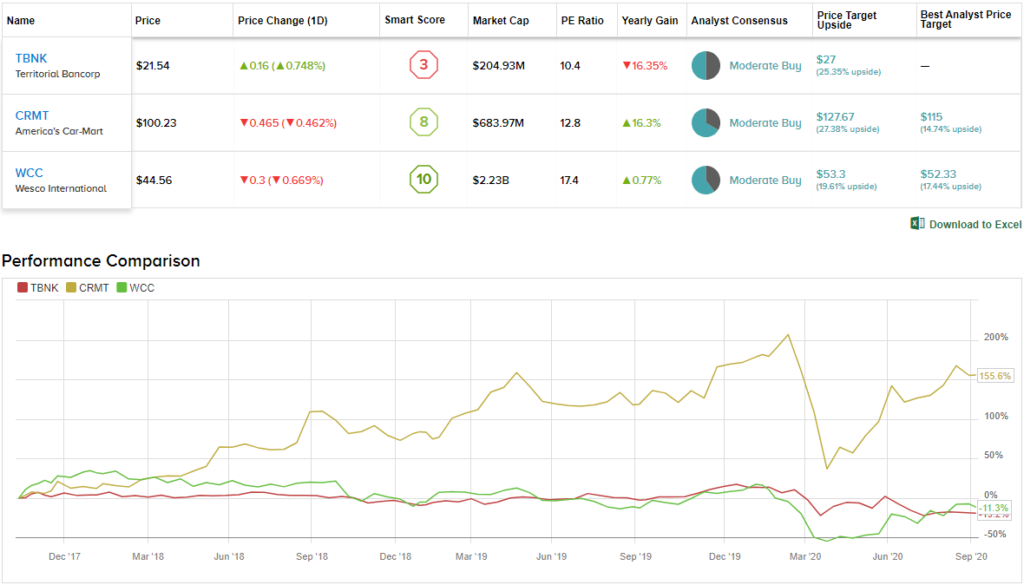

Territorial Bancorp (TBNK)

We start with a small-cap financial stock, Territorial Bancorp. This holding company offers, through its subsidiary Territorial Savings Bank, commercial and retail banking services to customers in Hawaii. Services include deposits, commercial and industrial real estate loans, consumer loans, residential mortgages, and home equity lines of credit. The bank’s name reflects the Islands’ status when the company was formed, in 1921.

The company reported EPS well above the forecasts in both Q1 and Q2, beating estimates by 17% and 30% respectively. Revenues remained stable during those quarters, and the outlook for Q3 predicts sequential improvements as the economy reopens.

The company has kept up its dividend payment through the corona crisis. Territorial has a history of adjusting the dividend to fit the times – but has not done so during the ‘corona half’ 1H20. The regular quarterly payment of 23 cents was last sent out in August. At that rate, it annualizes to 92 cents per common share and yields 4.32%.

Compass Point analyst Laurie Hunsicker makes TBNK her top pick, rating the stock a Buy and giving it a $30 price target that suggests a robust 40% upside potential. (To watch Hunsicker’s track record, click here)

In her comments, Hunsicker says, “TBNK has a history of paying out ~100% of EPS in the form of dividends and buybacks; TBNK does not currently have a buyback in place (completed its ninth buyback in 2Q20), and in our view has substantial room to declare a special dividend and/ or authorize a new buyback, relative to our EPS projections versus the $0.92 annual dividend… We continue to believe that TBNK will be the top performing bank in our coverage from a credit perspective during the COVID-19 crisis.”

It has been relatively quiet when it comes to other analyst activity. In the last three months, only 2 analysts have issued ratings; one is a Buy and the other is a Hold making the consensus rating a Moderate Buy. Shares are selling for $21.30 and have an average price target of $27, giving the stock a 25% one-year upside potential. (See TBNK stock analysis on TipRanks)

America’s Car-Mart (CRMT)

Next up, America’s Car-Mart, is an Arkansas-based company in the lucrative used vehicle marketplace. The company operates in both brick-and-mortar dealerships and online, and boasts that it specializes in assisting customer with poor or no credit. Car-Mart offers low down payments, flexible financing arrangements, layaway, and buyers and payment protection plans. Car-Mart has a market cap of $684 million, and operates 140 locations in 12 states.

With economic pressure on consumers increasing, used vehicles have seen an increase in popularity and sales. CRMT has seen revenues remains stable during 1H20, while earnings made strong sequential gains in Q2. At the top line, revenues have remained between $186 and $195 million, with the most recent quarter, the company’s fiscal Q1, showing $187 million. That same quarter saw earnings of $2.83, 91% above expectations.

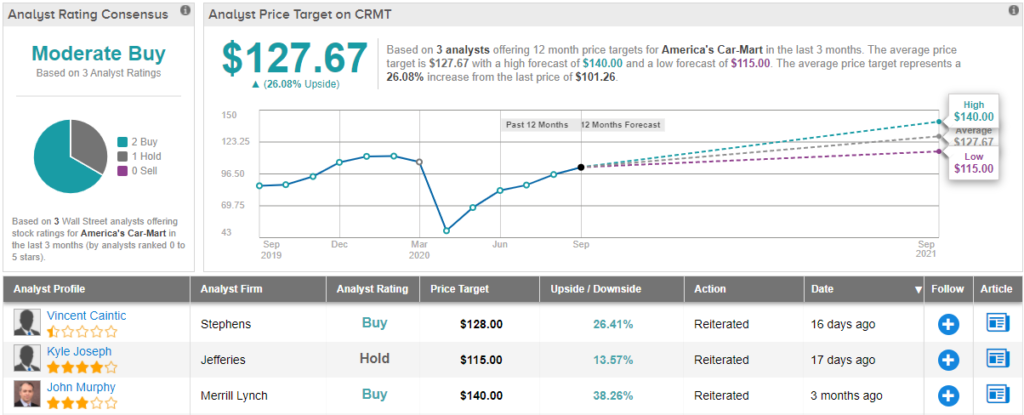

Vincent Caintic, reviewing the stock for investment firm Stephens, sees Car-Mart getting a boost from the general conditions of the vehicle market. He writes, “We are encouraged that Car-Mart’s used car supply has been fixed. It does seem like the price/volume dynamic will fluctuate over the next few quarters, with mgmt. expecting “relief” in car prices over the next six months. Recall that lower car prices are better for CRMT.”

In line with those comments, Caintic makes CRMT his top pick. The analyst rates the stock an Overweight (i.e. Buy) along with a $128 price target. This figure implies an upside of 28% from current levels. (To watch Caintic’s track record, click here)

The Moderate Buy analyst consensus rating on CRMT is based on 2 Buys and 1 Hold set in recent weeks. The average price target, at $127.67, is in line with Caintic’s. (See CRMT stock analysis on TipRanks)

Wesco International (WCC)

Last on our list is Wesco, a major name in the electronics industry. Wesco manufactures, distributes, and services communications, electrical, industrial, and maintenance repair and operating and original equipment manufacturer products (MRO and OEM), and also offers logistics and supply chain management. Wesco boasts a $2.24 billion market cap, and over $8 billion in annual sales.

While earnings fell in Q1, the Q2 results showed a quick return toward normal levels – and beat the forecast by 57.5%. Going forward, the Q3 prediction is for further gains. Revenues in the first half were stable, at about $2 billion in each quarter.

Wells Fargo analyst Michael McGinn covers this stock, and he is impressed by Wesco’s recent business improvements.

“Underlying trends look favorable and appear to be showing a healthy dose of positive momentum. This is most notable within organic sales, which were limited to a 12% decline, marking a vast improvement from the highteens% declines previously reported April through May,” McGinn opined. “We think what matters most for investors is the prolific (1) scale, (2) demand (e.g., datacenter, IoT, security, denser fiber, 5G, utility T&D), (3) countercyclical FCF and (4) synergy potential, WCC will have to drive an estimated 30% EBITDA and 40% FCF accretion.”

With that in mind, McGinn makes WCC his top pick. The analyst rates the stock an Overweight (i.e. Buy) along with a $60 price target, which implies a 34% upside potential from current levels. (To watch McGinn’s track record, click here)

Overall, with an average price target of $53.30, Wesco shows a 19% upside potential from the current share price of $47.27. The Moderate Buy consensus rating is based on 10 reviews, including 6 Buys and 4 Holds. (See WCC stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.