Lululemon stock (NASDAQ:LULU) is currently trading near all-time high levels, following a tremendous 44% year-to-date rally. The sports apparel company that climbed the industry’s ranks through its iconic yoga leggings is expected to post an exciting Q3, given the robust results in the previous quarter. The stock’s inclusion in the S&P 500 (SPX) in October will also likely be a positive contributor moving forward due to increased ETF-related trading volumes. Thus, I remain bullish on the stock.

Lulululemon’s Robust Momentum

Lululemon is poised to unveil its Q3 results, building upon the robust momentum achieved in the prior quarter. Remarkably, the company continued to impress in Q2, marked by vigorous growth across all facets of its operations. Notably, there was a considerable expansion in margins, paving the way for a significant upswing in profits. Let’s delve into the details.

Sales Growth Driven by Same-Store Growth, New Store Openings

In the second quarter, Lululemon achieved net revenue growth of 18% to $2.2 billion, driven by an improved performance in its existing and newly-opened stores, which also contributed to the top line. To be more specific, comparable sales rose by 11%, powered by a 7% rise in same-store sales and a 15% rise in e-commerce (DTC) sales.

Total retail sales rose by a more significant 21% compared to the prior year period, as Lululemon’s square footage expanded by 19% during this time. This expansion was, in turn, the result of Lululemon opening 72 net new stores since last year to a total of 672 locations.

Margin Expansion Drives Superb Earnings Growth

With a continual rise in same-store sales and a noteworthy surge in online sales, Lululemon’s unit economics have been consistently improving, leading to year-over-year expansion of the company’s profit margins. This trend was once again demonstrated in its Q2 results, where the gross profit margin reached an impressive 58.8%. This not only marked a substantial 230 basis points advancement from last year’s margin of 56.5%, but it also stands as the highest gross profit margin in the company’s history.

As the gross margin continued its upward trajectory, the operating income for the quarter reached approximately $479 million, accounting for 21.7% of net revenue—a noteworthy improvement from the adjusted operating margin of 20.9% reported in the previous year. This positive momentum resonated throughout the financial statement, culminating in a net income of $341.6 million, equivalent to $2.68 per share. This contrasts with the net income of $289.5 million, or $2.26 per share, posted in Q2 of last year.

What to Expect in Q3

Following an exciting Q2, the company’s momentum is expected to carry over in Q3. Management’s outlook supports this argument, as they expect net revenue for the quarter to range between $2.165 billion and $2.190 billion. This implies an increase of 17% to 18%. Further, Wall Street’s consensus estimates for the quarter point to earnings per share of $2.28, suggesting a year-over-year increase of 13.9%. Thus, earnings growth momentum is also expected to remain vigorous.

S&P 500 Inclusion to Boost Investor Interest in LULU Stock

LULU stock has received a significant boost with its recent addition to the S&P 500, a development likely to increase investor interest due to its inclusion in associated ETFs. As a constituent of such a widely-tracked index, Lululemon is likely to attract attention from institutional investors and index-tracking funds, leading to heightened trading activity and potential share price appreciation. Finally, inclusion often prompts index funds to rebalance their portfolios, necessitating increased holdings of LULU shares.

Is LULU Stock a Buy, According to Analysts?

Turning to Wall Street, Lululemon has a Moderate Buy consensus rating based on nine Buys, two Holds, and one Sell assigned in the past three months. At $427.92, the average Lululemon stock forecast implies 6.7% downside potential.

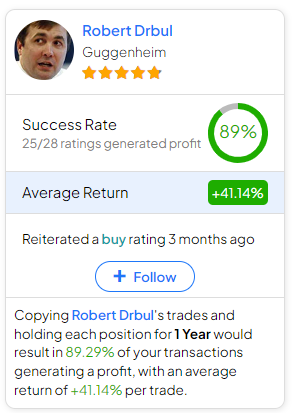

If you’re seeking guidance on which analyst to track when it comes to trading LULU stock, the most profitable analyst covering the stock (on a one-year timeframe) is Robert Drbul from Guggenheim, with an average return of 41.14% per rating and an 89% success rate. Click on the image below to learn more.

The Takeaway

Lululemon’s remarkable performance in Q2 sets a compelling stage for its upcoming Q3 results. The company’s impressive sales growth, driven by both same-store expansion and the successful launch of new outlets, underscores its resilience and market demand. Notably, the consistent headway in unit economics, showcased by a lofty gross profit margin of 58.8%, paints a picture of sustained financial strength.

As we anticipate LULU’s Q3 results, management’s positive outlook and Wall Street’s EPS growth estimates signal continued momentum. Lululemon’s recent inclusion in the S&P 500 further elevates its standing, attracting increased attention from institutional investors and index-tracking funds.

The stock’s tremendous rally year-to-date rally might be a concern for new investors to jump into the stock. The fact that shares trade at what appears to be a hefty forward P/E of about 38, based on Wall Street’s EPS estimate of $12.18 for the year, may also appear daunting. However, LULU stock has always traded near such elevated levels, as the company’s earnings growth has allowed it to grow its valuation constantly. Thus, I maintain my bullish stance on the stock.

Questions or Comments about the article? Write to editor@tipranks.com