2020 has been disastrous for the retail sector, but you wouldn’t know it if you are Lululemon Athletica (LULU). The athleisure specialist has turned the coronavirus on its head (wind) and used it as a springboard. A pivot toward the digital realm resulted in a resilient Q1 earnings report (Lululemon’s digital sales increased by 70% to make up 54% of its business), and Wall Street has cheered on its progress. The evidence? Shares are up by 56% in 2020.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Ahead of next week’s second-quarter earnings report (Sep 8, AMC), Deutsche Bank analyst Paul Trussel notes that 2Q data points are in LULU’s favor.

Highlighting solid comps from athletic peers such as Foot Locker and Dicks Sporting Goods in their respective recent 2Q reports, Trussel expects LULU “will continue to be a COVID-19 winner.”

Trussell now expects total sales to be up by 5.8%, a big increase compared to his previous -7.0% estimate. Additionally, the analyst raised his 2Q EPS forecast to $0.79 from $0.55 (Street calls for $0.52).

Nevertheless, despite the raises, Trussel stops short from recommending investors pounce on shares ahead of the earnings report, as there is one glaring problem keeping him on the sidelines.

Trussel explained, “Expectations are high heading into the print with some investors pointing to sales growth up 10%+ in 2Q (vs. guidance down HSD). Even if results come up short of the high buy-side bar, we believe the stock will likely continue to be resilient with bulls applying a premium multiple due to the company’s differentiated product and global expansion opportunities. With the stock trading at 51x and 44x our 2021 and 2022 EPS forecasts, respectively, we look for a better entry point.”

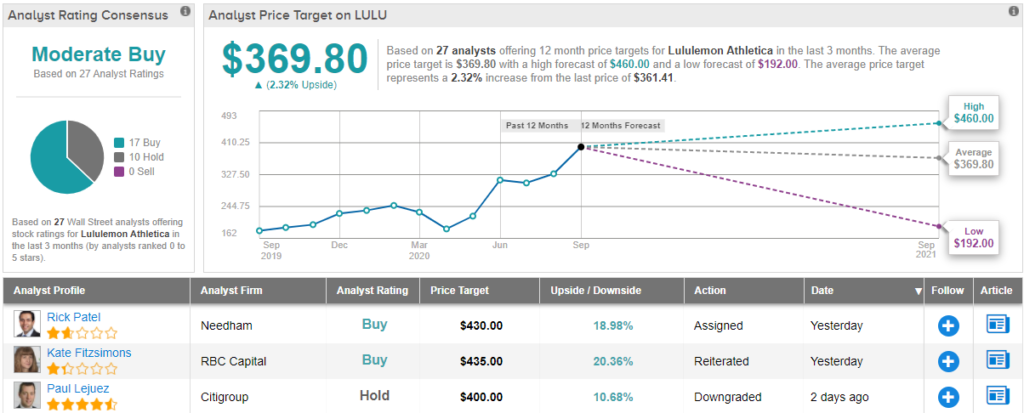

Trussel, then, keeps his Hold rating intact, while also maintaining a $341 price target for the stock. This figure implies a 5.5% downside from current levels. (To watch Trussel’s track record, click here)

Trussel’s colleagues are only slightly more bullish. LULU’s Moderate Buy consensus rating is based on 17 Buys and 10 Holds. The $369.80 average price target suggests shares will climb a modest 2%. (See Lululemon stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.