The last few years saw the markets go crazy. Between the COVID lockdowns and market crash, the rebound recovery, last year’s sustained bull run, and this year’s devastating first half that saw the bull turn into a bear. But in all of that, there have been stocks that have outperformed the market.

These winning stocks have attracted attention from Jim Cramer, the well-known host of CNBC’s ‘Mad Money’ program. Among other things, Cramer has been following stocks which won big during the COVID crisis and have continued – and are continuing – to show gains. In his view, these stocks have demonstrated their strength and persistence, and are worth more investor attention.

“Wall Street wrote off all the Covid winners, but a handful of these companies have proven to be real staying power giants. and I think it’s absolutely worth sticking with their stocks,” Cramer explained.

Now let’s take a look at two such stocks on Cramer’s buy list. In fact, Cramer is not the only one singing these stocks’ praises. According to the TipRanks platform – they are both rated as Strong Buys by the Street’s analysts.

Thermo Fisher Scientific (TMO)

Thermo Fisher is a scientific and medical technology company – but rather than engage in research, it designs, manufactures, and supplies the wide range of equipment that makes it possible for scientific labs to operate.

Thermo Fisher’s products include a full range of laboratory supplies, equipment, and instruments, as well as chemicals, materials, and samples needed in modern lab testing. The company’s product lines are widely used in medical research, including biotech and pharmacology, as well as in academic, governmental, environmental, and industrial circles. Anywhere there’s a need to up-to-date labs and lab operations, Thermo Fisher can find a foothold.

It’s a profitable foothold, too. In 2021, Thermo Fisher saw more than $39.2 billion in total revenues, and the company is on track to beat that total this year. Both the Q1 and Q2 this year top line totals showed year-over-year growth, with the Q2 revenue, of $10.97 billion, up 18% year-over-year. Adjusted EPS in Q2, at $5.51 per share, was down slightly y/y, but it beat the $4.99 forecast by ~10%.

Turning to share performance, we find that TMO shares have been outperforming for the past year or more. In the last 12 months, during which the S&P 500 index fell 7%, TMO gained 8%.

In coverage for Baird, 5-star analyst Catherine Ramsey Schulte lays out a case for Thermo Fisher to keep gaining in the coming months. She writes, “Thus far, macro concerns, namely pricing/inflation pressures and broader recessionary fears, have not affected TMO’s end markets/activity levels, and management remained constructive on underlying demand, bookings/order trends, and its overall portfolio positioning/mix. Ultimately, this confidence drove TMO to again raise 2022 revenue/EPS guidance, with core outperformance and modestly higher COVID testing expected to offset incremental FX pressures. We continue to view TMO as a core holding and top idea into 2H22/2023.”

In line with her bullish stance, Schulte rates TMO a Buy, and her $711 price target implies room for ~22% upside potential in the next 12 months. (To watch Schulte’s track record, click here)

Overall, this mega-cap scientific firm has picked up 12 recent analyst reviews, which include 10 to Buy and 2 to Hold – for a Strong Buy consensus rating. TMO shares are trading for $580, and their $667.18 average price target indicates room for ~15% growth in the year ahead. (See TMO stock forecast on TipRanks)

Danaher Corporation (DHR)

The second Cramer pick we’re looking at, Danaher Corporation, is a global conglomerate company. Like TMO above, it operates in the science and technology fields, where its subsidiaries and partner firms produce and provide technology and services in the life sciences, diagnostic, environmental, and applied solutions fields. Danaher’s leading position in this niche brought it $29.5 billion in revenue last year; this year’s first-half revenue of $15.4 billion is already up 9% year-over-year.

While revenues are up, Danaher’s earnings in 2Q22 showed mixed results. The net income of $1.68 billion was down 5% y/y. At the same time, the $2.76 non-GAAP diluted EPS was up 12% from the year-ago quarter. Danaher’s business also brought in an operating cash flow of $2 billion in Q2, with a non-GAAP free cash flow of $1.7 billion.

Over the past three months, while the S&P 500 has risen by 3%, TRGP shares outperformed, climbing about 19%.

JPMorgan analyst Rachel Vatnsdal looked under the hood at Danaher, and described the recent quarterly results as ‘impressive.’ Vatnsdal wrote: “Overall, we are impressed by 2Q results given the macro backdrop, especially in China, and we view management’s bullish outlook on non-COVID bioprocessing as encouraging for sustained future MSD+ base business core growth.”

Getting to the bottom line, the analyst went on to say, “We view DHR as one of the highest quality names in our coverage universe, built around the Danaher Business System (DBS), which provides a playbook and set of tools for continuous operational improvement across the portfolio…”

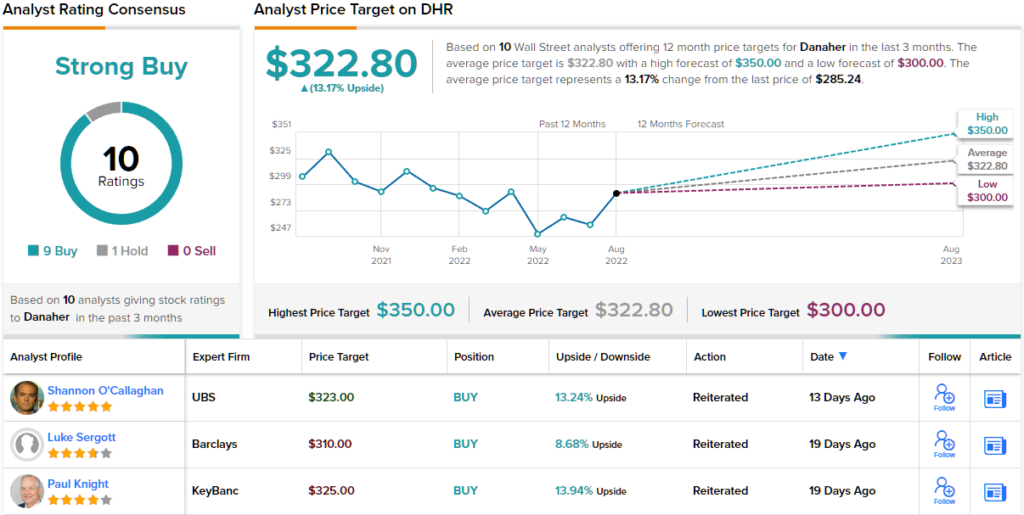

Given these bullish comments, it comes as no surprise that Vatnsdal rates Danaher shares an Overweight (i.e. Buy), or that her $350 price target suggests a 23% upside for the stock going forward. (To watch Vatnsdal’s track record, click here)

Overall, Danaher has a Strong Buy consensus rating based on 10 recent analyst reviews, which include 9 to Buy and 1 to Hold. The stock’s average price target is $322.80 and its current trading price is $285.24, giving a 12-month upside gain potential of 13%. (See Danaher stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.