Wall Street is on a roller coaster again, as investors try to navigate the path between high inflation and the Fed’s aggressive interest rate hikes. What we know for certain is that the S&P 500 is down 18% year-to-date, and the NASDAQ is down 26%.

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

At least one investing expert, however, is getting on his soapbox to encourage investors to buy now, while prices are low. This is the view of Shark Tank investor Kevin O’Leary. The venture capitalist makes a case for investors to take advantage of volatility to start a buying streak.

“If you’re an investor, maybe the best thing to do here is – since you can’t guess the bottom – is to take opportunities like today and buy stocks that you think are attractive,” O’Leary noted.

With this in mind, Wall Street’s analysts have identified two compelling tickers whose current low share prices do not reflect their long-term value. Noting that each is set to take back off on an upward trajectory, the analysts see an attractive entry point. Using TipRanks’ database, we found out that the analyst consensus has rated both Strong Buy, with considerable upside potential also on tap. Let’s take a closer look.

Couchbase, Inc. (BASE)

The first stock stands out in the world of database management. Couchbase produces and distributes a series of open-source database-as-a-service (DBaaS) platforms, offering users a distributed architecture that allows elastic scaling, workload isolation, and real-time data replication, while avoiding security issues associated with single points of failure. The system is built for use on mobile and IoT devices that use intermittent connections, or depend on microservers or consumption-based cloud computing.

Which is all a fancy way of saying that Couchbase’s products – Capella, the Couchbase Server, Couchbase Mobile, and the Autonomous Operator – go where your work is.

Couchbase went public on the NASDAQ in July of last year, raising $200 million in its IPO. The shares have dropped by about half since then, even as the company’s top line has steadily increased and the bottom line net losses have moderated.

In its most recent quarterly report, for Q2 of fiscal year 2023 – the quarter ending on July 31 – Couchbase showed a 34% year-over-year gain in revenue, with the top line hitting $39.8 million. The revenue total included a 32% y/y gain in subscription revenues, which were reported at $37.1 million. Annual recurring revenue (ARR), a key metric of future business, hit $145.2 million, a 26% gain year-over-year. The company’s earnings came in at a loss, of 19 cents per share in non-GAAP measures. This was a dramatic improvement form the $1.54 per-share loss recorded in the year-ago quarter.

Covering this stock for Oppenheimer is 5-star analyst Ittai Kidron, who writes, “Couchbase handily beat F2Q expectations, and again noted positive demand trends for Capella. It also appears relatively resilient to macro-related demand headwinds, given its historical focus on large enterprises and multi-year deals. While watchful of possible recessionary pressure, we remain LT bullish given the large NoSQL opportunity, and market expansion with DBaaS/Capella.”

Kidron follows up on his commentary with an Outperform (i.e. Buy) rating, and a $22 price target that implies a one-year upside of ~44%. (To watch Kidron’s track record, click here)

Overall, the Strong Buy consensus rating on this stock is based on 5 recent analyst reviews, including 4 to Buy and 1 to Hold. The average price target of $22 is practically the same as Kidron’s. (See Couchbase stock forecast on TipRanks)

Helios Technologies (HLIO)

Next up is Helios Technologies, a player in the global industrial technology sector. Helios is a leading provider of hydraulics and electronics, developing, designing, manufacturing, and marketing a wide range of products and hard tech solutions. The company’s products include custom electronic control systems, hydraulic cartridge valves, and quick release valves, among other items, all for a variety of end-use markets. Helios has sales and customers in more than 90 countries around the world.

Helios is working toward a 10-year goal, set in 2015, of reaching $1 billion in annual sales. The company boasts that it is on track hit that goal ahead of schedule, in 2023. In the last full calendar year, 2021, Helios had over $869 in net sales; the company posted $482 million in revenue for 1H22, and is on track to beat last year’s total. The most recent quarter, 2Q22, saw $241.7 million in revenues, up 8% year-over-year. Earnings for 2Q22 came in at $1.18 per diluted share, in non-GAAP measures. This was flat from Q1, and down 2% y/y.

That said, Helios has faced headwinds in the last 12 months, including supply disruptions, price/cost pressures, and inventory destocking. As a result, the stock has lost 51% year-to-date.

However, 5-star analyst Nathan Jones, from Stifel, remains upbeat on the stock, pointing out several factors that should chart a path forward.

“We continue to see multiple opportunities for Helios over the next several years, within the company’s control: Acquisition made over the last several years provides Helios the opportunity to transform from a holding company to an integrated operating company and to gain capacity, reduce costs, shorten supply chains, and increase market penetration globally…. Successfully leveraging the businesses to simultaneously drive above-market growth while reducing the cost structure,” Jones explained.

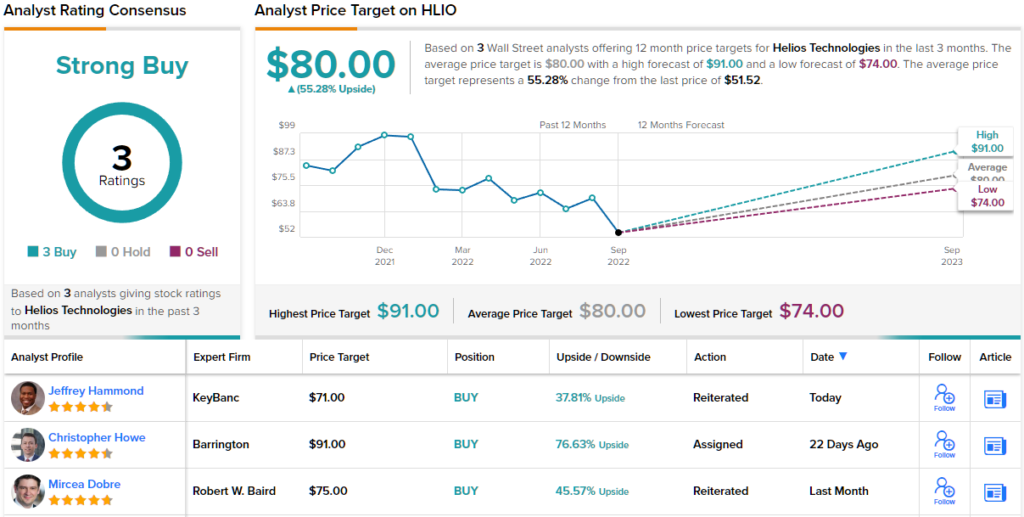

Building from this stance, Jones gives HLIO shares a Buy rating, and sets a price target of $74. This figure indicates potential for ~44% gains in the coming year. (To watch Jones’ track record, click here)

All in all, all three of the recent analyst reviews here are positive, giving Helios’ stock its unanimous Strong Buy consensus rating. HLIO is currently priced at $51.52 and its average price target, $80, implies a 12-month upside of 55%. (See HLIO stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.