This year started with a bang, saw a fizzle in April – but now appears to be regaining its stride. As we saw last year, the gains continue to be dominated by the ‘Magnificent 7’ tech stocks. This group of mega-cap companies collectively experienced a 48% year-over-year earnings increase in the recent first-quarter 2024 releases, in contrast to a 2% collective decline across the other S&P companies.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

Going forward, however, expectations are that the remaining 493 companies on the S&P will close that gap, and Bank of America strategist Ritesh Samadhiya sets out a case for the Mag 7 stocks to realize a 15% earnings share gain in Q4 while the rest of the index increases its share to 14%.

That forecast implies a hefty broadening of the base, opening more opportunities for investors. The combination of a broader base and the current improved investor sentiment has Samadhiya’s team feeling bullish – and their colleagues among the Bank of America stock analysts are running with it, telling investors that it’s time to take advantage of the potential for wider gains and to jump on the bandwagon for two stocks in particular.

A look into the TipRanks data shows that these 2 stock picks from BofA offer widely divergent potentialities – but Bank of America’s analysts are predicting solid upsides for both. Here are the details.

Cisco Systems (CSCO)

Cisco Systems is a well-known name in the world of networking technology, with a wide and varied set of product lines on the market. The company’s product offerings include switches, routers, cloud and network management, interfaces and modules, outdoor and industrial wireless access points, wireless controllers, firewalls, and secure endpoints. The list is long and includes product lines for data centers, data analytics, video, IoT, and software. There are few areas involved in online networking and security that Cisco isn’t involved in.

In a move designed to bolster its strong position in software and data analytics, Cisco acquired the analytic software company Splunk in a transaction worth approximately $28 billion. The deal brings Splunk’s capabilities in data searching, monitoring, and analysis into Cisco’s stable of product offerings, making Cisco one of the world’s largest software companies. New features for Cisco, derived from the acquisition, include security and observability solutions. The transaction was completed on March 18.

Cisco has multiple opportunities on tap for the near future, including the movement of AI systems to Ethernet networks. This will bring the ‘shiny new thing,’ gen AI, directly into one of Cisco’s core competencies. In addition, Cisco’s strength in optical networks will open up opportunities for the company to move into the hyperscaler ecosystem.

Despite Cisco’s solid reputation and strong market position, the company’s stock has underperformed in recent months. The company reported its fiscal 2Q24 results in February, and while the financial results surpassed the forecasts, the company’s guidance failed to impress.

But the Q2 results do bear a closer look. The company brought in $12.8 billion in revenue, down 6% year-over-year but $100 million better than had been expected. At the bottom line, Cisco’s non-GAAP EPS of 87 cents was 3 cents per share over the estimates. Looking forward, management gave fiscal Q324 revenue guidance in the range between $12.1 billion and $12.3 billion – but the consensus had looked for $13.1 billion. The EPS forecast of 84 of 86 cents per share was also lower than the 92 cents analysts had hoped to see.

At least one analyst, however, is not fazed by Cisco’s guidance. Tal Liani, 5-star analyst from Bank of America, believes that the upside potential here – coming from Cisco’s strengths in the AI and Security segments, as well as the Splunk acquisition – simply outweigh the weaknesses.

“We expect Networking to start normalizing and see renewed growth driven by Cisco’s share gains in Ethernet-based AI buildouts of hyperscalers. We expect Security growth to accelerate with the help of firewall stabilization and recent new product launches. Lastly, we see great growth synergies from Splunk’s acquisition. While the next two quarters may remain pressured, we believe this weakness is fully reflected in Street expectations and management guidance is adequately conservative,” Liani opined.

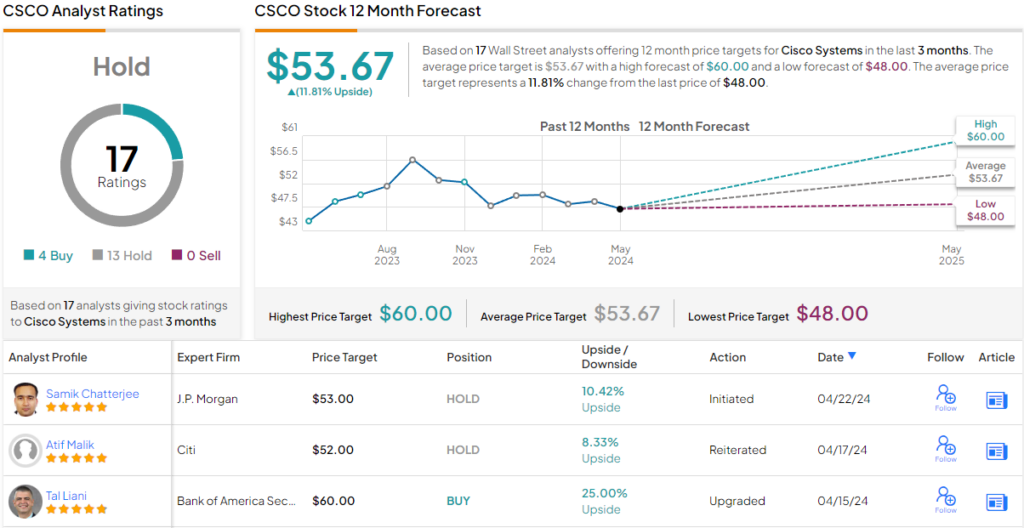

Liani complements his positive stance with a Buy rating on CSCO, and a $60 price target that points toward a 25% upside on the one-year time horizon. (To watch Liani’s track record, click here)

The bullish Bank of America viewpoint here is something of an outlier; this stock has a Hold rating from the analyst consensus, based on 17 recent recommendations that include 4 Buys and 13 Holds. The shares have a $53.67 average price target, suggesting a ~12% one-year gain from the current share price of $48. (See CSCO stock forecast)

89bio, Inc. (ETNB)

The second Bank of America pick we’ll look at is 89bio, a research-oriented biopharmaceutical company with a focus on finding, developing, and commercializing new therapeutic agents for the treatment of liver and cardio-metabolic diseases. The company’s research pipeline is organized around its advanced drug candidate BIO89-100, and includes clinical studies in the treatment of NASH (nonalcoholic steatohepatitis, sometimes now referred to as MASH, or metabolic dysfunction-associated steatohepatitis) and SHTG (severe hypertriglyceridemia).

The drug candidate BIO89-100, also known as pegozafermin, was engineered specifically to target the underlying metabolic issues that cause NASH and SHTG. The drug is a glycoPEGylated analog of FGF21, or fibroblast growth factor 21. FGF21 is a liver hormone known to act as a master metabolic regulator with broad effects, particularly on the glucose and lipid metabolism. Pegozafermin was developed to increase the half-life of the FGF21 hormone.

89bio has recently posted updates from three trials, all targeting the NASH indication. In March, the company initiated a Phase 3 trial, dubbed ENLIGHTEN, for non-cirrhotic (F2-F3) and cirrhotic (F4) patients. In addition, the company has also released two data sets from the Phase 2b ENLIVEN trial, in patients with advanced NASH and with cirrhotic NASH. The data sets demonstrated statistically significant improvements in key markers of liver health. On the SHTG side, the company is continuing to enroll patients in the Phase 3 ENTRUST trial, to evaluate the efficacy, safety and tolerability of pegozafermin in the treatment of SHTG. Data from this trial is expected for release in 2025.

The solid research program on pegozafermin and its long-term commercial potential caught the attention of analyst Alexandria Hammond, who writes in her coverage for Bank of America.

“Beyond macro uncertainties, we suspect concerns over competition in the fatty liver disease space (aka MASH) and commercial unknowns ahead of the first-to-market MASH launch have weighed sentiment. We acknowledge the uncertainties of the MASH commercial landscape, but, in our view, 89Bio’s FGF21 analogue pegozafermin offers intriguing upside as a next—and possibly best-in-class— MASH agent given a more favorable safety/tolerability profile (projected launch 2027) in a particularly attractive and less crowded market sub-segment,” Hammond opined.

Hammond adds, laying out a clear case for investors to buy in now, “With pegozafermin well-positioned to compete for the space’s meaningful—and addressable potential—along with the limited downside, we think the current risk/reward is particularly attractive.”

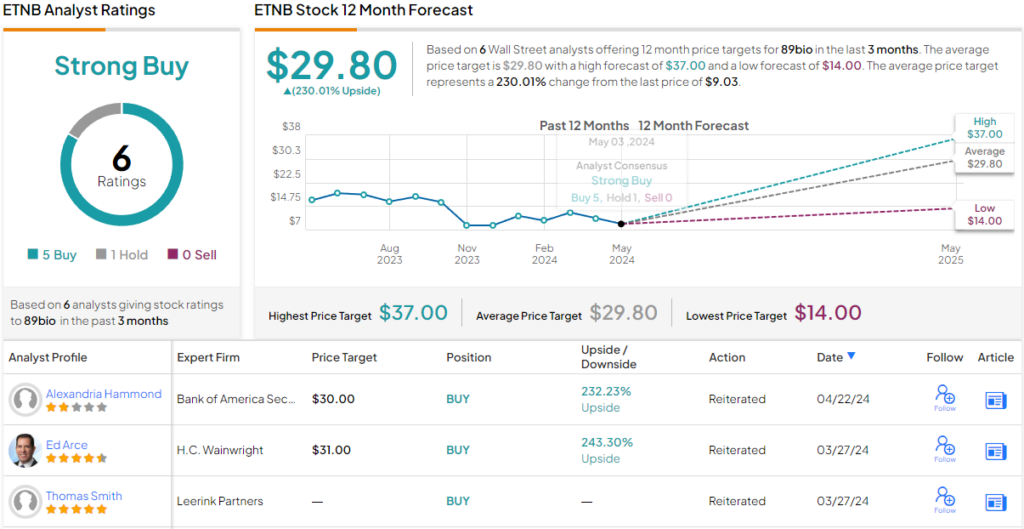

These comments support the analyst’s Buy rating on ETNB, while her $30 price target implies a robust 232% one-year upside potential. (To watch Hammond’s track record, click here)

Overall, this stock is clear winner in Wall Street’s eyes, boasting a Strong Buy consensus rating from the analysts based on 5 recent ‘Buy’ calls against a single ‘Hold.’ The stock is selling for $9.03 and its $29.80 average price target suggests that it will gain 230% over the course of the next 12 months. (See ETNB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.