We’re only 6 weeks away from 2025, which means that it’s time to check in again with Wall Street’s investment banks and professional analysts – they’re selecting their ‘top pick’ stocks for the coming year. These are the choices that the experts believe will bring solid returns in the coming year, and investors should pay close attention.

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

The ‘top picks’, the must-have stocks, can come from a wide range of sectors, depending on the analysts’ preferences. Some like industrials, others like biotech, others go for Big Tech, while some advise buying into venture capital. The common denominator is simple – the analysts all pick stocks that are primed for gains going forward.

Right now, the analysts at JPMorgan are taking the lead, highlighting their own must-haves for 2025. According to the latest data drawn from the TipRanks platform, two stocks they are highlighting boast ‘Strong Buy’ consensus ratings and solid upside potential; let’s give them a closer look, and add in the JPM commentaries, as well, to find out what makes them top picks.

HA Sustainable Infrastructure Capital, Inc. (HASI)

The first stock on our list is HA Sustainable Infrastructure, formerly known as Hannon Armstrong. This company’s name points toward its business: HA Sustainable is a finance company and asset manager focused on supporting the energy transition from fossil fuels to renewable power sources. In short, this company provides capital and financing resources for firms involved in clean or green energy.

This is a potentially high-growth field, as there are several pushes supporting an energy transition – social pressures, to reduce our modern society’s pollution footprint; business pressures, to ensure a reliable power supply as non-renewable sources grow scarce; even governmental pressures, as legislatures respond to the more grass-roots pressures and provide support for an energy transition. HASI, from its base in Annapolis, Maryland, is working to provide financial support in this field – and at the same time, to provide solid returns for its own investors.

The company has over 35 years’ experience in its field, and currently boasts an investment portfolio worth $6.3 billion. This is split among three key market segments: behind-the-meter, which includes energy efficiency, residential solar, and community solar projects, and makes up approximately 47% of the total portfolio; grid connected, which includes wind and solar power generation, along with large-scale power storage projects, and makes up some 40% of the portfolio; and fuels, transport, & nature, which includes renewable natural gas, fleet decarbonization projects, and ecological restoration initiatives, and adds up to about 13% of the portfolio. This breakdown only refers to the investment portfolio; in addition, HASI has total managed assets of $13.1 billion.

Of particular interest to return-minded investors, HASI has a long history of keeping a reliable dividend payment. The most recent declaration was on November 7, of 41.5 cents per common share for a January 10 payment. This payment annualizes to $1.66 per common share, and gives a forward yield of 5.9%.

We should note here that HASI shares fell sharply in the wake of the recent election. Trump’s victory, and the related anticipation of sharp policy differences from the previous administration, particularly in the area of climate policy, spooked investors on the subject of green energy investment. Shares in HASI are down by 20.5% since the election.

That said, JPM analyst Mark Strouse, writing several days after the vote, was clearly not worried about this stock when thinking of its prospects. He said, “We believe the company is largely tracking expectations and continue to see conservatism in the medium-term targets as project yields continue to trend higher and the company’s recent investment grade credit rating likely benefits spreads over time. Given the scale, diversification, and maturity of its portfolio, we highlight HASI as being relatively more insulated from potential policy changes under a new administration compared to the rest of our renewables coverage… HASI is a top pick within our coverage.”

Strouse goes on to rate this stock as Overweight (Buy), with a $42 price target that suggests a one-year upside potential of 50%. (To watch Strouse’s track record, click here.)

From the Street generally, this stock gets a Strong Buy consensus rating, based on 8 reviews that include 6 Buys and 2 Holds. The shares are priced at $28.05 and their $41.83 average target price implies a one-year gain of 49%. (See HASI’s stock forecast.)

Xenon Pharmaceuticals (XENE)

The second stock on our list, Xenon Pharmaceuticals, describes itself as a neuroscience-focused biopharma company. Xenon has made solid progress in the development of new therapeutic agents for the treatment of epilepsy, and its lead product, azetukalner, is currently undergoing multiple late-stage clinical trials in several seizure and mental-health applications.

Azetukalner is a Kv7 potassium channel opener, described by Xenon as both novel and potent. It was developed as a potential treatment for focal onset seizures (FOS) as well as primary generalized tonic-clonic seizures (PGTCS), and is also being tested as a treatment for major depression. While epilepsy and major depression are very different disorders, both frequently prove resistant to current treatments – leading to high unmet medical needs among patients.

On the clinical trial side, the company is highly optimistic about azetukalner on the FOS track. The X-TOLE trial series is proceeding with good results, and Xenon expects to release topline FOS data from the Phase 3 X-TOLE2 clinical trial by the second half of next year. In addition, on the major depressive disorder (MDD) track, Xenon has presented data from the Phase 2 study of azetukalner, and is preparing to initiate a Phase 3 trial, X-NOVA2, before the end of 2024. Backing up the array of clinical trials, Xenon also has several pre-clinical programs underway. These include the Nav1.7 sodium channel inhibitors under investigation as treatments for pain indications, and the Nav1.1 sodium channel openers being studied as a potential treatment for Dravet Syndrome.

All in all, Xenon is a biopharmaceutical company with multiple shots on goal lined up – and that has caught the attention of JPM analyst Tessa Romero. Covering this stock for JPM, Romero writes of it, “At a high-level, we have reason to believe that the stock will start to work again as we move towards 2025 which we expect to be a pivotal year for the company with XTOLE2 data anticipated for azetukalner in FOS that, if positive, could unlock the path to product approval and send shares towards the $60/sh level (our FOS deep dive here); we also expect increased visibility on the development pipeline in validated targets such as Nav1.7 and Nav1.1 that mgmt seemed particularly excited about in our conversation to be additional drivers for the stock… Remains a top pick heading into 2025.”

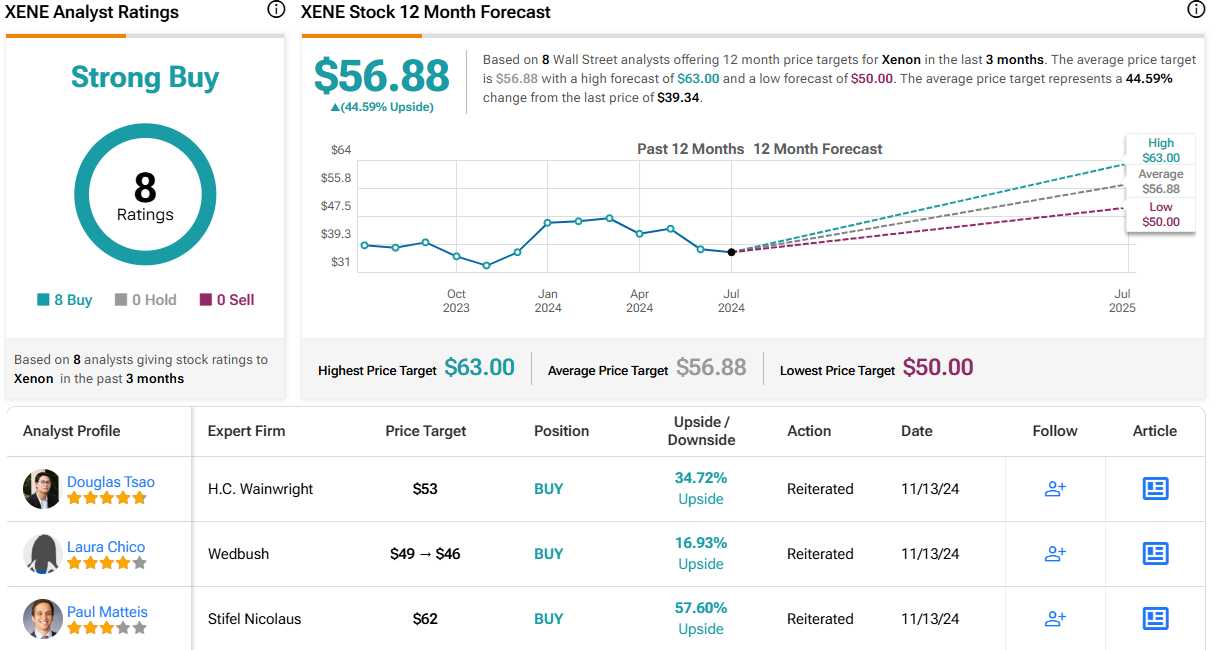

Along with choosing XENE as a top pick, Romero puts an Overweight (Buy) rating on the shares – and a $63 price target that indicates room for a 50% gain in the next 12 months. (To watch Romero’s track record, click here.)

The Street would concur – as is clear from the unanimously positive Strong Buy consensus rating, based on 8 recent analyst reviews. XENE shares are trading for $39.34, and their $56.88 average price target implies an upside of 44.5% on the one-year horizon. (See XENE’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.