It’s hard to tell where the markets are heading right now. Are we on the path to recovery or is there more pain ahead? Is a recession at the gate or can it be averted?

Don't Miss Our Christmas Offers:

- Discover the latest stocks recommended by top Wall Street analysts, all in one place with Analyst Top Stocks

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Going by one indicator, a recession is indeed in the cards, according to J.P. Morgan’s head of global equity strategy Mislav Matejka.

Whenever jobless claims have exceeded by 10% or more their current three-month average, a recession has materialized. And that has just occurred.

But that doesn’t necessarily mean it’s time to pack up the portfolio. In fact, the indicator is actually a bullish signal for stocks. Whenever it has flashed, the other consequence has been an 11% uptick, on average, for the S&P 500 over the next year.

Further boosting confidence, Matejka thinks the central bank will relax its monetary policy soon. “The Fed could undertake a much more balanced policy view post September,” Matejka explained, “as some of the inflationary pressures continue abating.”

Against this backdrop, Matejka’s analyst colleagues at the banking giant have homed in on two lesser-known stocks which they think are poised to charge ahead. Are they alone in believing so or do they have the backing of other experts in the analyst community? With the help of the TipRanks database, we can certainly find out.

Bowlero (BOWL)

The first J.P. Morgan pick we’ll look at is American bowling center operator Bowlero. With roughly 300 centers, the majority of which are U.S.-based, the company is the largest ten-pin bowling center operator in the world. That’s not the only big thing about the company; while most U.S. bowling centers have an average of 21 lanes, Bowlero’s have an average of 40. Its family of brands includes Bowlero, Bowlmor Lanes, and AMF, and combined their lanes cater to over 26 million guests every year. Not to mention, in 2019, the company acquired the Professional Bowlers Association which came with thousands of members and a global fan base in the millions.

The company has yet to report its fiscal fourth quarter results (June quarter) but we can get a feel for the business’s performance by looking at the March quarter report.

Revenue reached $258 million, amounting to a 129.8% year-over-year increase and a 25.8% improvement over pre-pandemic levels. Adjusted EBITDA of $108.4 million rose by $81 million (295.7%) compared to the same period last year and came in $41 million (60.9%) above the pre-pandemic display.

Investors have obviously been pleased with the company since it went public at the end of last year via a SPAC merger. Even in 2022’s very difficult environment, shares are up 31% year-to-date.

J.P. Morgan analyst Kevin Heenan thinks there’s more to come and highlights the company’s distinctive attributes.

“Bowlero is unique, with unmatched scale yielding material P/L benefits tied to two key economic traits of the industry: (i) ~2/3 of revenue comes with essentially no variable costs (bowling & amusement), driving material operating leverage on incremental visits/games; and (ii) ~90% market share is captured by local independents, of which ~1,500 (or >40%) represent ‘high quality acquisition’ targets for Bowlero to apply its proven operating model on,” Heenan explained.

“Looking ahead – our work points to stable/improving margins at 10% modeled top-line growth w/ bowling industry tailwinds exiting the pandemic (in contrast to outdoor-based leisure peers),” the analyst added.

To this end, Heenan initiated coverage on Bowlero shares with an Overweight (i.e., Buy) rating and $17 price target, suggesting shares will climb 44% higher in the year ahead. (To watch Heenan’s track record, click here)

Bowlero has slipped under the radar a bit, and only has 2 recent analyst reviews. They both agree, however, that it’s a stock to buy, making the Moderate Buy analyst consensus unanimous. With shares trading at $11.82, the $15.50 average price target suggests room for ~31% upside. (See Bowlero stock forecast on TipRanks)

Arco Platform (ARCE)

Next up we have Brazilian technology company Arco Platform, which operates in the field of education. The Sao Paulo, Brazil-based firm provides educational systems with technologically advanced features made to deliver educational content mostly to private schools across the country.

The curriculum is designed for K–12 grade levels and is accessible in printed and digital forms via a dedicated site. Publishing, editing, promoting, and advertising educational materials for private schools are all activities of the business and the services are catered toward parents, teachers, administrators, and kids.

Arco reported 2Q22 earnings earlier this month, with revenue increasing by 60.8% year-over-year to R$412.1 million ($80.43 million). Adjusted EBITDA hit R$110.7 million ($21.61 million), amounting to a 53% year-over-year uptick, as the company’s efficiency initiatives appear to be taking shape and are helping offset a rise in operating costs, mainly regarding higher printing and freight costs.

The focus on efficiency is one of the reasons J.P. Morgan’s Marcelo Santos has changed his tune on Arco. The enticing share price (down 35% year-to-date) is another, and those are not the only ones.

“With the exception of the pandemic years of 2020 and 2021, private K12 schools have been successful in increasing tickets above inflation since at least 2006, and we expect this positive behavior to continue in coming years. Content providers like Arco should benefit, also being able to push higher prices,” Santos wrote. “We see (1) the company well positioned to ride the uncertain macroeconomic scenario, given strong inflation pass-through capabilities of the private K12 market; and (2) the weakness in shares being an attractive entry point, given significant underperformance versus the broader education sector.”

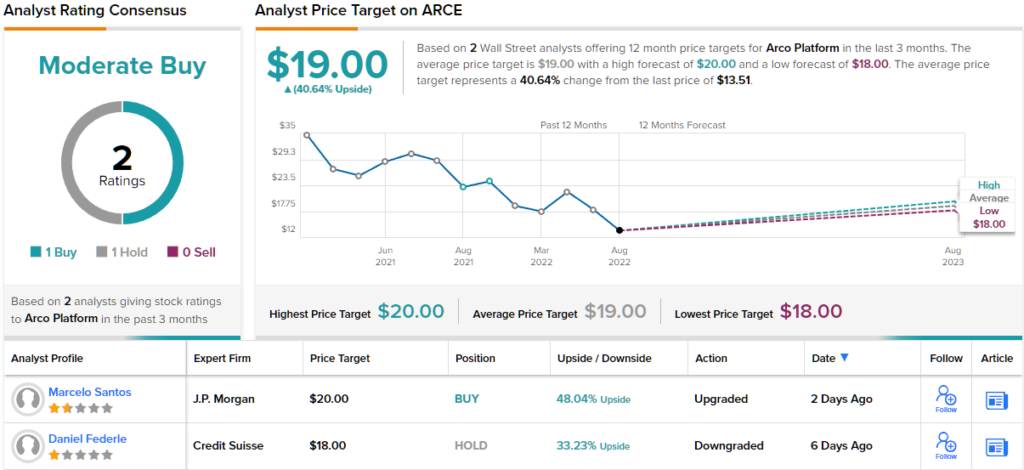

Based on the above, Santos recently upgraded Arco’s rating from Neutral to Overweight (i.e. Buy) while his $20 price target makes room for one-year gains of 48%. (To watch Santos’s track record, click here)

Small-cap foreign companies don’t always get a lot of analyst attention. Indeed, Arco has stayed relatively under-the-radar, with its Moderate Buy consensus rating breaking down into 1 Buy and 1 Hold. Arco shares are priced at $13.51, with an average price target of $19 indicating a runway toward ~41% upside for the next 12 months. (See ARCE stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.