Picking the right stocks is key to building a successful portfolio, but how do you identify them? That’s the central question, especially in a market environment like the one we’ve seen in recent weeks, with increased volatility and sharp swings up and down in reaction to Presidential statements, competitive tariffs, and international manoeuvring amid geopolitical chaos.

That’s where Wall Street’s heavyweights step in. Backed by deep research teams and decades of market insight, the major banking firms regularly cut through the noise to highlight their best stock ideas.

Right now, the pros at J.P. Morgan are shining the spotlight on two names they’ve crowned as top picks for the rest of 2025. These are stocks they believe are set to outperform in the months ahead. To get the full picture, we turned to the TipRanks database to see how the broader Street views these picks. Let’s dive in.

Primoris Services (PRIM)

The first JPM pick we’ll look at is a specialty construction company, with its focus on essential infrastructure projects and services. Primoris Services provides support for critical infrastructure in the utility, energy, and renewable sectors. The company operates in the US and Canada, and has a reputation as a quality provider of engineering, construction, and maintenance services on a wide range of projects, including power delivery, communications, transportation infrastructure, and utility-scale solar and other renewables.

Primoris’ business is conducted through two main divisions, Energy and Utility. On the energy side, the company is known for working on projects in the downstream and midstream segments of the oil, natural gas, and chemical industries. The company has extensive experience in energy projects, at all scales – including utility scale. Primoris can build out infrastructure for solar, energy storage, renewable fuels, and biomass gasification projects. On the utility side of its business, Primoris works with natural gas and communications providers across North America, on the engineering, management, and construction of delivery systems.

As a construction contractor, Primoris is a full-service company, putting a skilled and multi-disciplined workforce at the service of its customers. The company prides itself on delivering world-class quality, in support of the fuel and energy transformations now underway.

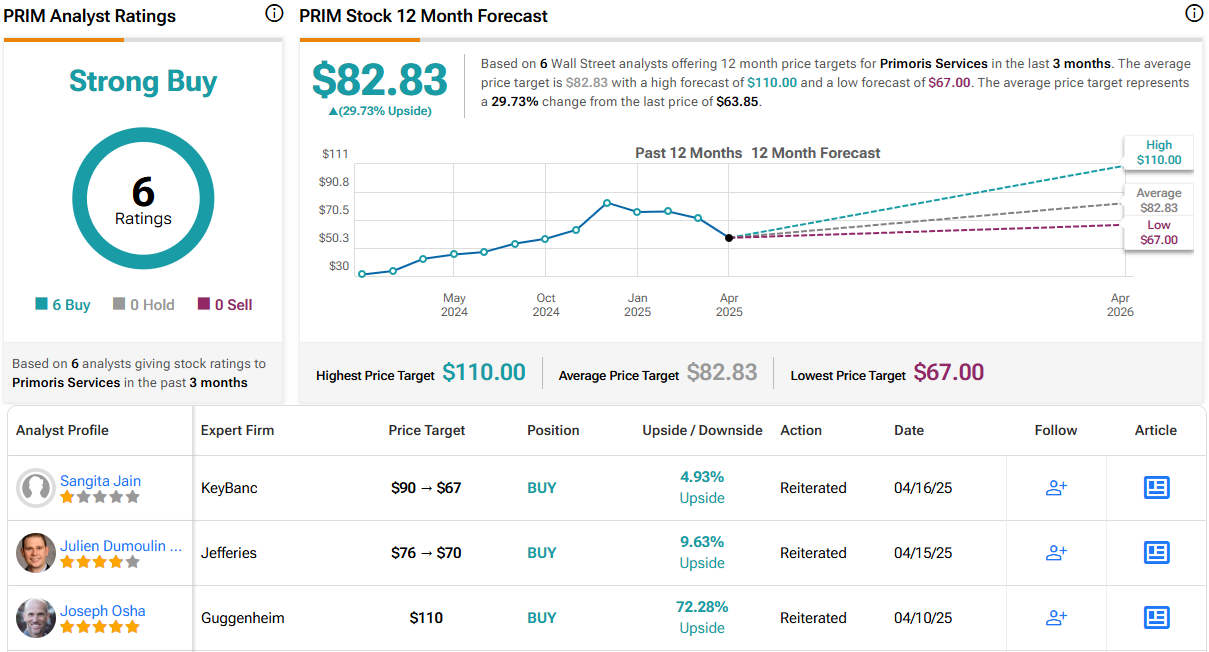

Primoris last reported financial results for Q4 and full-year 2024. In the fourth quarter, the company’s total revenue, $1.7 billion, was up 14.5% year-over-year and came in $110 million better than had been expected. At the bottom line, the company reported a non-GAAP EPS of $1.13, up from 85 cents in the prior-year period and 38 cents per share better than the forecast. We should note, however, that shares in PRIM, while up 36% for the past 12 months, are down 16% for the year-to-date. We should also note that Primoris’ CEO left the company this past March, and that the firm is now under interim leadership while the Board conducts a search.

That decline in the stock price has caught the attention of JPM’s Drew Chamberlain, who also notes the company’s leadership turnover. He writes, “We increasingly believe PRIM’s valuation pullback presents an attractive entry point into the stock, as we gained comfort in the structural outlook and business fundamentals appearing largely unchanged… While we acknowledge an unexpected CEO change for a strong performing company and stock is rarely a welcome sign for investors, we believe PRIM, now trading at a slight discount to its 3-year average forward EBITDA multiple, has become too attractive to pass up, as the much improved business is priced at historical averages . We believe PRIM is the most attractive option in our EPC coverage and our top pick.”

Chamberlain goes on to put an Overweight (i.e., Buy) rating on this ‘top pick’ stock. His price target, set at $90, points toward a one-year upside potential of 41%. (To watch Chamberlain’s track record, click here)

The 6 recent analyst reviews on this stock are unanimously positive, for a Strong Buy consensus rating. The shares are priced at $63.85, and the $82.83 average target price implies a gain of 30% for the coming year. (See PRIM stock forecast)

Valley National Bancorp (VLY)

Next up is Valley National Bancorp, a bank holding company whose banking operations are conducted through its subsidiary, Valley National Bank. Valley National Bank is a regional bank, with its headquarters in New Jersey and more than 200 branch locations in New Jersey, New York, California, Illinois, Florida, and Alabama. The bank serves both individual and business customers.

The bank’s services include the usual full range of financial services and products, including checking accounts and credit cards; savings accounts, CDs, and IRAs; loans, including mortgages, home loans, auto loans, and personal loans; and wealth management, including trust and estate planning, and insurance services. Valley National was founded in 1927, and the bank has over $62 billion in assets.

Valley National released its 1Q25 results last week. The headline numbers missed the forecasts, coming in at $478.4 million for revenue and $0.18 per share in non-GAAP earnings. The revenue total was up 5% year-over-year, and fell short of the estimates by $4.9 million; the non-GAAP EPS figure was flat year-over-year and missed expectations by a penny.

Looking into some of the details, we find that Valley National’s loan business is improving on quality metrics. The company reported that accruing past due loans (those more than 30 days past due and still accruing interest) fell from December 31, 2024 to March 31, 2025, moving from $51.7 million to $47.5 million. The current figure represents 0.11% of the total loans. The company also saw its net loan charge-offs decline year-over-year, from $98.3 million in 1Q24 to $41.9 million in 1Q25.

Despite the headline misses, JPM analyst Anthony Elian remains upbeat on this company. He sees the bank’s business as solid, and writes, “We thought that it was a fairly routine quarter for Valley, highlighted by solid NIM expansion, good expense control, and credit quality playing out as previously telegraphed. Moreover, with Valley maintaining its 2025 outlook ranges for all metrics, when we layer in the additional disclosure that points to a certain direction for each metric, post the quarter our EPS estimates are little changed. Looking ahead, we thought it was very interesting to note that although the company is now pointing to the low end of its full year 2025 loan growth guidance of 3-5% (tied to 1Q25 off to a slower start), Valley may be in a position by the end of this year to actually see its CRE loan portfolio stabilize and potentially even see its balances grow… Consequently, we maintain our Overweight rating with VLY remaining one of our top picks coming out of 1Q25 earnings.”

Along with that Overweight (i.e., Buy) rating, Elian gives VLY shares a $10.50 price target, suggesting that the stock will appreciate by 20.5% in the year ahead. (To watch Elian’s track record, click here)

Overall, VLY gets a Moderate Buy rating from the Street’s consensus, based on 7 recent reviews that include 3 to Buy and 4 to Hold. The shares are currently priced at $8.71 and their $10.29 average price target indicates room for an 18% gain over the next 12 months. (See VLY stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.