The economic environment is riddled with uncertainty, yet stocks are climbing higher. To kick off the week of trading, all three of the major U.S. stock indexes landed in the green yesterday, with the market aggressively charging forward since its trip to bear territory in March.

Stay Ahead of the Market:

- Discover outperforming stocks and invest smarter with Top Smart Score Stocks

- Filter, analyze, and streamline your search for investment opportunities using Tipranks' Stock Screener

So, is there still room for stocks to rise? J.P. Morgan says yes. The firm’s strategists led by Nikolaos Panigirtzoglou argue that billions of dollars could still get pumped into equities instead of bonds as investors rebalance portfolios.

“Investors are still underweight equities and signs of overextension are confined to momentum traders… There is still plenty of room for investors to raise their equity allocations,” Panigirtzoglou wrote in a note to clients. This suggests that investors have the capacity to support the market during a more tumultuous time.

Bearing this in mind, we used TipRanks’ database to get all of the details on three stocks in J.P. Morgan’s coverage universe. Looking at two tickers the firm believes could surge in the next year and one it is sidelined on, we wanted to find out if the rest of the Street agrees with the calls. As it turns out, they do.

Kala Pharmaceuticals (KALA)

Focused on developing therapies using its mucus-penetrating particle (MPP) technology, Kala Pharmaceuticals wants to provide patients suffering from eye diseases with more effective treatments. On the heels of a major milestone for the company, J.P. Morgan gave it a rave review.

Representing the firm, analyst Christopher Neyor highlights the FDA’s recent acceptance of the NDA resubmission for Eysuvis, KPI-121, which incorporated pivotal Phase 3 results from the STRIDE-3 study. Given the October 30 PDUFA date, the analyst thinks this sets the stage for a possible late 2020 approval and launch of KALA’s lead asset in acute dry eye. He also sees this development as making the risk/reward profile “highly favorable”, with “a potential move into the mid-teens near-term and further upside longer term.”

Speaking to the market opportunity, Neyor estimates that peak sales could exceed $750 million based on “fairly conservative assumptions for both product pricing (below chronic dry eye therapies) and market penetration (among ~17 million U.S. diagnoses dry eye patients) with upside to over $1 billion potential peak sales.”

To support this forecast, Neyor stated, “Our physician feedback indicates significant unmet need for an acute dry eye treatment with patients of nearly all severity levels experiencing intermittent flares. Further, there are currently no approved products on the market or late-stage competitors that offer rapid relief for short-term acute dry eye symptoms within a few days.”

The good news doesn’t end there. The company already has sales and marketing infrastructure for its approved product in post-surgical pain and inflammation, Inveltys (KPI-121), which could be leveraged during Eysuvis’ launch. KALA plans to further expand its sales team, with the Inveltys salesforce completely overlapping the target Eysuvis ophthalmology prescribing base. In addition, the significant unmet need means there could be faster uptake and reimbursement decisions, in Neyor’s opinion.

With Neyor also calling Inveltys “de-risked”, the deal is sealed. He assumed coverage with an Overweight call and lifted the price target from $14 to $19, implying 42% upside potential.

Turning now to the rest of the Street, other analysts are on the same page. With 100% Street support, or 5 Buy ratings to be exact, the consensus is unanimous: KALA is a Strong Buy. The $23 average price target brings the upside potential to 72%. (See Kala stock analysis on TipRanks)

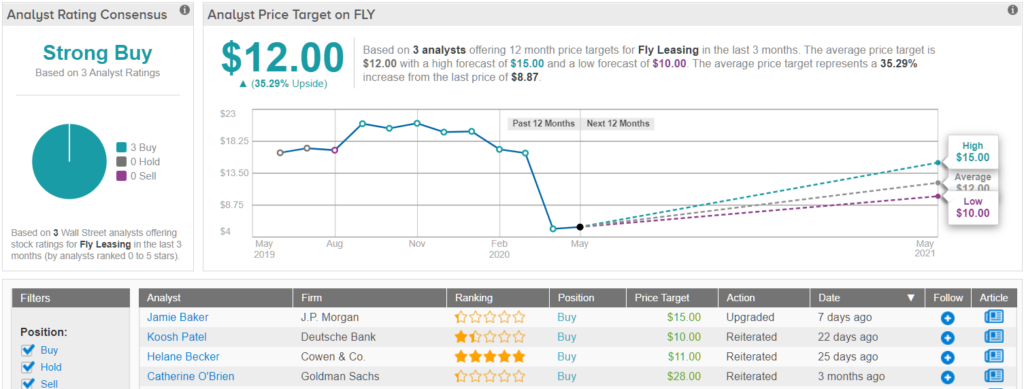

Fly Leasing Limited (FLY)

Taking its place as one of the top aircraft leasing companies, Fly Leasing offers a fleet of modern, high-demand and fuel-efficient commercial jet aircrafts. As a result of its lagging equity recovery from mid-March lows and peer-leading valuation, J.P. Morgan just gave it a thumbs up.

Comparing FLY to other major players, analyst Jamie Baker tells clients that the company has been left in the dust by the larger names. Still, since its “mid-March pummeling”, it has staged a significant recovery. Although it lacks the “market cap enormity” as well as an order book, Baker thinks that the current share price reflects a unique buying opportunity.

“Based on our revised forecasts, FLY’s valuation relative to peers has widened to a level we now believe begets opportunity… Simply put, at current levels, we believe risk/reward in FLY shares is skewed to the upside,” Baker commented.

On top of this, after evaluating FLY and its peers under the same set of deferment and write-off assumptions, Baker believes its liquidity is more “robust”. As there are only $10 million of debt maturities for the rest of 2020 and $413 million in 2021, with no capex for the remainder of 2020 and only ~$27 million in 2021, liquidity is still positive and doesn’t rely on revolver capacity.

It should be noted, however, that FLY doesn’t boast the same level of revolver availability as its competitors do. That said, Baker remains confident in FLY’s ability to round out the year with liquidity of $409 million and $242 million in 2021.

To this end, Baker to take a more bullish approach. In addition to upgrading FLY’s rating from Neutral to Overweight, he reduced the price target. Even with the haircut, the $15 figure still suggests shares could climb 69% higher in the next year. (To watch Baker’s track record, click here)

All in all, other analysts echo Baker’s sentiment. 3 Buys and no Holds or Sells add up to a Strong Buy consensus rating. Based on the $12 average price target, the upside potential comes in at 35%. (See Fly Leasing stock analysis on TipRanks)

HP Inc. (HPQ)

When evaluating information tech giant HP, J.P. Morgan saw the lack of catalysts, fiscal Q2 earnings release that was impacted by headwinds in the printer segment and weak outlook for printing in fiscal Q3 as reason enough to step onto the sidelines.

During the quarter, EPS came in at $0.51 on revenue of $12.5 billion, down 10% year-over-year in constant currency, but slightly above the consensus estimate. While the personal systems (PS) business was helped by strong WFH demand, the printing segment dropped 18% year-over-year, with the steepest decline in commercial hardware, which fell 31% year-over-year.

Going forward, its guidance for fiscal Q3 EPS is below expectations. Writing for the firm, analyst Paul Coster stated, “Mostly it is continued weakness in the printing business that should draw attention of the skeptics.”

That being said, Coster believes the HP bulls will point to management’s decision to postpone the use of leverage in an expanded share buy-back as being the source of the negative sentiment. Coster acknowledges that given the historic levels of uncertainty, it makes sense why HP chose to delay the leveraged buybacks. However, he argues that “absent this catalyst, in our view, there isn’t much reason to add to positions in this stock through year-end given tough second half year-over-year comps for the PS segment, and ongoing declines in the Printer segment.”

Coster added, “There should be some downside support owing to strong cash-flow prospects and a ~4% dividend yield, and the planned expense containment warrants attention, but for now we think HPQ is stranded in value territory.”

Based on all of the above, Coster downgraded HPQ from Overweight to Neutral. Additionally, he trimmed the price target from $21 to $20. Despite the cut, the target still implies upside potential of 32%. (To watch Coster’s track record, click here)

What does the rest of the Street have to say about HPQ? It turns out that other analysts agree with Coster. 10 Holds, 1 Buy and 1 Sell have been received in the last three months, so the consensus rating is a Hold. At $17.55, the average price target suggests 16% upside potential. (See HP stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.