SBA Communications (NASDAQ: SBAC) features some special qualities that have come in handy lately. Still, it’s likely that investors overvalue these qualities at the stock’s current valuation levels. Accordingly, I am neutral on the stock.

How Do SBAC Stock’s Qualities Contribute to Its Performance?

SBA features numerous qualities that have played a significant role in the company maintaining its continuous growth in revenues and profitability. For starters, SBA operates in an industry with few market participants. Leasing telecommunications towers is a niche area with only a handful of major other players, including Crown Castle (NYSE: CCI) and American Tower Corporation (NYSE: AMT).

The economics in an oligopolistic structure are always favorable while the company faces softer competitive forces. It’s very unlikely that competitors will emerge over time because the telecommunications towers space is very capital-intensive. It requires spending tons of money in capital expenditures continuously for a company to keep growing and stay competitive. Thus, the current players are likely to keep dominating the industry.

Additionally, SBA currently benefits from superior tenant dependability compared to most conventional REITs. Think about it; Retail REITs are currently encountering foot traffic issues amid worries over consumers’ purchasing power softening. Commercial REITs continue to report soft occupancy rates as hybrid working conditions have prevailed. Residential REITs experienced a massive drop in home prices following last year’s euphoric market landscape.

In comparison, SBA’s tenants include all telecommunication majors. For them, SBA’s towers are critical assets, and thus, fulfilling their lease obligations is of high priority. Hence, SBA faces no occupancy or rental collection issues.

It’s also worth mentioning that all telecommunication majors, including AT&T (NYSE: T), Verizon Communications (NYSE: VZ), and T-Mobile US (NASDAQ: TMUS), are publicly-traded companies with transparent financials. They also enjoy resilient cash flows due to the essential nature of telecommunications. Hence, SBA’s results have not been affected at all by the myriad of factors its sector peers are currently suffering from. Let’s examine.

Q3 Results: Unfazed Performance Despite Sector Headwinds

As just mentioned, SBA’s performance has remained unfazed by the ongoing headwinds the real estate sector is facing. Its most recent Q3 results make for a great illustration. The company reported record revenues of $675.6 million, up 14.6% year-over-year, powered by a larger portfolio of towers and higher leasing activity. With telecommunications towers remaining in high demand, the company continues to expand its property portfolio and sign leases at attractive rates. In Q3, SBA’s expansion endured, as SBA acquired 131 communication sites and also constructed 113 towers on its own.

Robust top-line growth led to similar adjusted funds from operations (also known as AFFO, a cash-flow metric used by REITs) growth as well. On a per-share basis, AFFO grew 14.4% to $3.10, driven by lower interest expenses and a lower share count amid SBA’s share buybacks. While higher operating expenses slightly offset the growth in revenues, these figures are quite impressive. Few REITs have managed to post double-digit bottom-line growth this year, which is a testament to SBA’s unique attributes.

Given that SBA’s tower acquisition and development spree is lasting, its growth is set to be sustained, moving forward. In fact, subsequent to the end of Q3, SBA acquired or was under contract to acquire about 34 communication sites. Management’s boosted guidance also points to further growth in financials. The company now expects site leasing revenues to be between $2.325 and $2.335 billion and AFFO/share to land between $12.12 and $12.34 (up from $11.87 to $12.24 previously). At the midpoint, management’s AFFO/share outlook implies year-over-year growth of 13.9%. This clearly exhibits that the company’s results have been unfazed by the ongoing headwinds the real estate sector is fronting.

Is Mr. Market Pricing SBAC Stock Fairly?

In my view, SBAC stock is not fairly priced by the market. SBA Communications has been a Wall Street darling for years now, as investors have long appreciated the company’s unique traits and their ability to result in robust financials, as discussed earlier. For this reason, the stock has consistently traded at a hefty premium. Shares have declined roughly 20% over the past year, yet SBA is trading at 24.8x the midpoint of management’s outlook.

Even if we assume that SBA keeps growing in the mid-teens, this valuation is hard to justify in a rising-rates environment. To illustrate how towering SBA’s valuation premium is, the sector’s forward P/AFFO median stands at 15x. The stock does deserve a premium, but surely not such a lofty one.

Is SBAC Stock a Buy, According to Analysts?

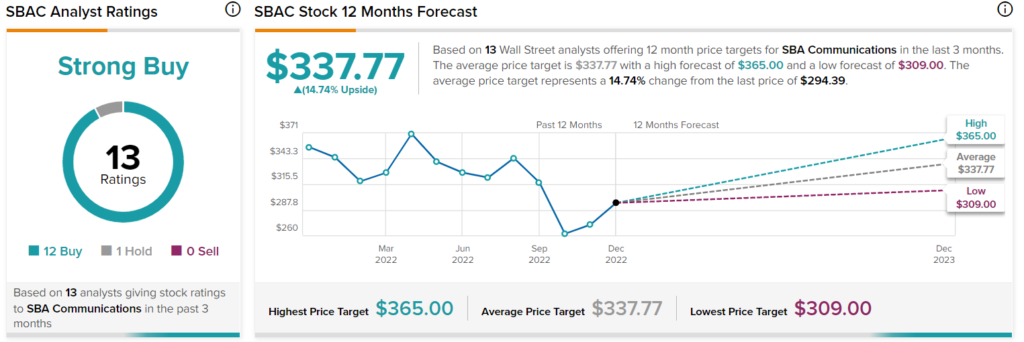

Turning to Wall Street, SBA Communications has a Strong Buy consensus rating based on 12 Buys and one Hold assigned in the past three months. At $337.77, the average SBA Communications stock forecast implies 14.74% upside potential.

Takeaway – A Resilient Company at a Steep Price

SBA Communications has proven resilient against the ongoing challenges the real estate sector is encountering, with its revenues and AFFO/share set to end the year at new record highs. Nevertheless, the stock’s elevated valuation multiple should discourage investors from driving the stock higher. In fact, the stock’s future returns could be limited given that SBA’s valuation could easily undergo a compression. Accordingly, I will stay on the sidelines on this one for the time being.

Questions or Comments about the article? Write to editor@tipranks.com