In life, there’s a common expression that also carries over into the dividend investing world: If it seems too good to be true, it usually is too good to be true. Oftentimes, dividend stocks with 6% or higher yields are yield traps. This means that the dividend income they provide to shareholders seems great, but it isn’t sustainable. Now and then, though, I stumble across high-yielding dividend stocks that aren’t yield traps. I believe that one such example is Pfizer (PFE).

Invest with Confidence:

- Follow TipRanks' Top Wall Street Analysts to uncover their success rate and average return.

- Join thousands of data-driven investors – Build your Smart Portfolio for personalized insights.

Interestingly, Pfizer’s 5.9% dividend yield is more than quadruple the 1.3% yield of the S&P 500 index (SPX). Despite the high yield, here is why I think the well-known healthcare stock is an income stock that warrants a Buy rating after its third-quarter earnings results.

Pfizer Put Up an Excellent Third Quarter

On October 29th, Pfizer released its third-quarter financial results. The firm’s total revenue jumped 31.2% over the year-ago period to $17.7 billion, which topped the analyst consensus by $2.8 billion. Rising COVID-19 infections in the summer and early fall led to an uptick in demand for antiviral COVID-19 treatment, Paxlovid, according to CEO Albert Bourla. That mainly was what drove the 43.6% year-over-year spike in Primary Care segment revenue to nearly $9.1 billion in the third quarter.

In addition, Pfizer’s Oncology segment posted $4 billion in revenue, which was up 29.8% over the year-ago period. This was due to ongoing momentum from advanced prostate cancer treatment Xtandi and the recent launches of advanced bladder cancer therapy Padcev and lymphoma therapy Adcetris. The company’s Specialty Care segment reported $4.3 billion in revenue during the quarter, which was equivalent to a 14% year-over-year growth rate. That was made possible by the expansion of the healthcare provider base for the Vyndaqel rare heart disease medication family.

Pfizer also posted $1.06 in adjusted diluted EPS for the third quarter, which was comfortably ahead of the analyst consensus of $0.61. These results were fueled by topline performance as well as by improvements in operating structure and favorable tax rates. On the first point, ongoing cost reductions have improved the company’s profitability. That’s how adjusted diluted EPS growth significantly outpaced revenue growth in the quarter.

A Brighter Future Is Ahead

After coming down from its COVID-19 pandemic high, Pfizer looks like it is firmly on the road to recovery, which adds to my bullish outlook. The company expects to realize $4 billion of its $5.5 billion-plus in annual targeted savings in 2024. That’s thanks to its cost realignment program launched last October. The other $1.5 billion-plus in anticipated annual savings are expected to materialize by the end of 2027 from the first phase of the manufacturing optimization program.

On the product launch side of the equation, Pfizer is also doing well. The company received several regulatory approvals in recent months. That includes an expanded indication for its respiratory syncytial virus vaccine to include high-risk adults in the U.S. aged 18 to 59 years old. The U.S. Food and Drug Administration also approved the monoclonal antibody therapy Hympavzi for adult and pediatric patients 12 years of age and older with certain types of hemophilia A and B.

Overall, Pfizer had over 100 drug candidates in its pipeline as of October 29th. As benefits from the cost savings programs are achieved and new drugs are launched, that’s expected to show up in the company’s earnings. This is why the analyst consensus is that Pfizer’s adjusted diluted EPS will rise by 46.2% in 2024 to $2.69, as well as by 5.2% to $2.83 in 2025 and by 7.8% to $3.05 in 2026.

The Market-Crushing Payout Is Sturdy

Furthermore, the reason why I think Pfizer is not a yield trap is because its above-average dividend looks to be backed up by its profits. The adjusted diluted EPS payout ratio is on track to be in the low 60% range in 2024. Combined with moderate earnings growth prospects in the coming years, this is why I believe that the dividend can reliably grow at a low single-digit pace annually. In my view, that’s a decent mix of starting income and dividend growth.

In addition, even after its acquisition of oncology company Seagen, Pfizer remains financially healthy. In the first nine months of 2024, the company has repaid $4.4 billion of debt. This suggests that Pfizer is making progress toward reaching its gross leverage target of 3.25x.

In the meantime, the company’s interest coverage ratio through the first nine months of 2024 was 5.1x, which was enough for S&P Global (SPGI) to award an A credit rating to Pfizer on a stable outlook.

The Stock Is a Good Value

Pfizer also looks to offer significant value from the current $28 share price. Indeed, this implies a current-year P/E ratio of just 10.6. That’s materially less than the 10-year average P/E ratio of 13.5. For a business that’s returning to growth, this is a compelling valuation.

Is PFE Stock a Buy, According to Analysts?

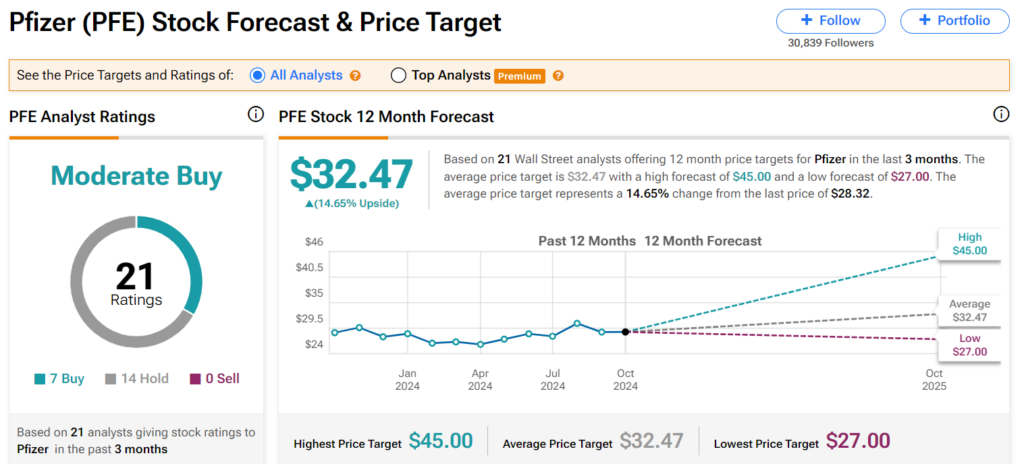

Turning our attention to Wall Street, analysts have a Moderate Buy consensus on Pfizer. Digging in deeper, seven analysts have assigned Buy ratings, and 14 have assigned Hold ratings in the last three months. With an average 12-month price target of $32.47 per share, Pfizer could see 14.65% upside ahead.

Investment Summary

Pfizer is an income stock that’s poised to fundamentally bounce back. The company’s existing product portfolio has momentum, new drug launches are doing well, and cost savings are being achieved. Moreover, the dividend looks to be relatively secure as Pfizer enjoys an A-rated balance sheet. Finally, the stock is trading at an intriguingly low valuation. It is for these reasons that I’m beginning coverage with a buy rating.