Considering its solid fundamentals and growth prospects, California-based Marvell Technology, Inc. (NASDAQ: MRVL) could be an attractive investment option for investors seeking exposure to the U.S. semiconductor market.

The $45.7-billion company is an integrated circuit maker, which has expertise in making digital signal processing, analog, standalone, mixed-signal, and other varieties of semiconductor chips. The company also develops core processors (single or multiple), hard disk drives, and other products.

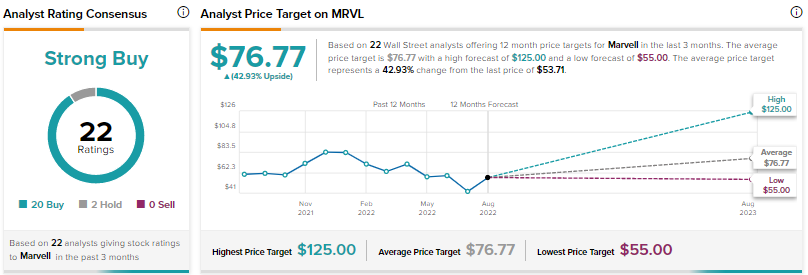

On TipRanks, analysts are unanimously optimistic about the prospects of Marvell and have a Strong Buy consensus rating based on 20 Buys and two Holds. MRVL’s average price target of $76.77 mirrors 42.93% upside potential from the current level.

A few days ago, Tore Svanberg of Stifel Nicolaus reiterated a Buy rating on MRVL with a price target of $78 (45.22% upside potential).

Factors Influencing Marvell’s Growth

The company’s products are widely used in automotive/networking, data center, enterprise networking, consumer, and carrier infrastructure markets. The growing popularity and need for cloud-optimized silicon are beneficial for it.

Its serviceable addressable market (SAM) is forecast to increase by 13% CAGR to $30 billion in the calendar year 2024 from $20 billion in 2021. Business opportunities are believed to be the highest in automotive/industrial and data center markets.

In addition to the above tailwinds, the company’s diversified portfolio of products and solutions, technological expertise, customer-centric approach, operational excellence, and solid management team raise its appeal.

Its financial performance has also been solid in the past few quarters. The average earnings surprise in the last fourth reported fiscal quarter was 6.6%. In the first quarter of Fiscal 2023 (ended April 30, 2022), the company’s earnings of $0.52 per share surpassed the consensus estimate of $0.51 per share by 2%. On a year-over-year basis, the bottom line grew 79.3% on the back of a top-line surge of 76.8%. High costs and expenses, however, played spoilsport in the quarter.

In May 2022, the company’s President and CEO, Matt Murphy, said, “We are guiding for growth to continue in the second quarter, projecting revenue at the midpoint to grow 5 percent sequentially and 41 percent year over year. With 88 percent of our overall revenue derived from data infrastructure, we are confident that our unique secular growth drivers in cloud, 5G, and auto, will continue to help drive sustainable long-term growth.”

On the contrary, supply-chain bottlenecks, cost inflation, and labor problems could hurt the company in the quarters ahead. Also, weakness in demand, due to the fears of a slowdown in the economy, could be troubling. These headwinds hold significance until the company gets fully equipped to deal with these issues considerably.

For the fiscal second quarter (ended July 2022), the company forecasts revenues to be $1,515 million (at mid-point) and adjusted earnings to be $0.56 per share (at mid-point).

Marvell is slated to release its results for the second quarter of Fiscal 2023 on August 25, 2022, after the market close. The consensus estimate for second-quarter earnings and revenues stands at $0.56 per share and $1.52 billion, respectively.

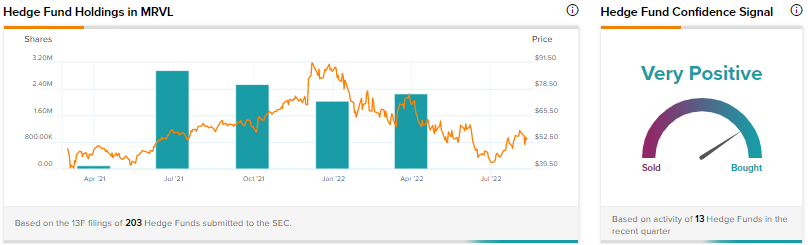

Bloggers & Hedge Funds Are Optimistic about Marvell’s Prospects

According to TipRanks, financial bloggers are 76% Bullish on MRVL, compared with the sector average of 65%.

Also, hedge funds are Very Positive about Marvell and have increased their stake in the semiconductor company by purchasing 224 thousand shares in the last quarter.

Concluding Remarks

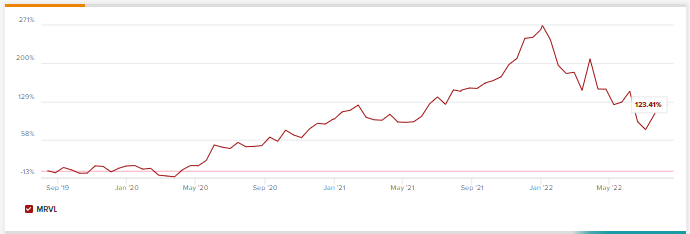

Marvell is a well-rooted company in the semiconductor market of the United States, as evident from its growth trajectory in the chart below. Also, the company has a Smart Score of 8, which mirrors its potential to outperform the broader market.

The chart also reveals that MRVL’s shares have fallen since the beginning of 2022. The 40% decline in the stock price was due to macroeconomic uncertainties and industry headwinds. For prospective investors, the company’s low price could be used to gain exposure to the stock.

Read full Disclosure

Questions or Comments about the article? Write to editor@tipranks.com