Airline companies, including Delta Air Lines (DAL), were pummelled during the COVID-19 pandemic. As the airline industry is capital-intensive, investors were worried about interest expenses amid global lockdowns. Today, shares of Delta Air Lines and its peers continue to trade below all-time highs, making them attractive to value investors. I am bullish on Delta Air Lines stock due to its cheap valuation, improving debt profile, and focus on higher-margin products.

An Overview of Delta Air Lines

Sporting a market cap of $29.5 billion, Delta Air Lines is the largest airline carrier in the world. With a fleet of 1,273 aircraft, it provides scheduled air transportation for passengers and cargo in the U.S. and internationally.

The company’s core network is centered around core hubs in Boston, New York, Seattle, and Atlanta. Meanwhile, its international hubs are located in Amsterdam, London, Bogota, Tokyo, Paris, Mexico City, and Sao Paulo. Delta Air Lines connects people on six continents, with 4,000 daily flights across 280 destinations.

Delta Air Lines Braces for Record Q3 Sales

Last week, Delta Air Lines forecast record sales in Q3 of 2024 due to robust summer travel demand. It expects sales to rise by 2-4%, which was still below consensus estimates of 5.8%. Comparatively, it forecast adjusted earnings between $1.70 and $2 per share, below estimates of $2.05 per share.

The revenue miss was attributed to discount deals, as several carriers flooded the market with flights, resulting in oversupply. Moreover, its earnings remain under pressure as increased capacity continues to weigh heavily on fares amid an inflationary environment.

However, investors should note that Delta is the most profitable carrier in the U.S. and accounted for 40% of industry profits in 2023, up from 30% in 2014.

A Focus on High-Margin Sales

In 2023, Delta Air Lines reported revenue of $58 billion, of which Premium revenue accounted for $19 billion of sales. Back in 2014, Premium revenue for the company stood at $10 billion. In recent months, Delta has focused on adding more premium seats that result in higher sales and profit margins. The company explained that brand affinity and an affluent customer base are driving premium demand, while the margins for this segment are 10 percentage points above main cabin seats.

In Q2 of 2024, Delta’s premium tickets rose by 10% year-over-year to $5.6 billion, while revenue from coach tickets increased marginally to $6.7 billion.

“Diverse revenue streams, including premium and loyalty, contributed higher growth and margins, underpinning Delta’s industry-leading financial performance and increasing our financial durability,” said Glen Hauenstein, Delta’s President.

A Focus on ROIC and Free Cash Flow

Delta Air Lines increased its return on invested capital from 8.4% in 2022 to 13.4% in 2023. Due to its multiple revenue streams, optimization, and operational efficiency, it expects to end 2024 with an ROIC in the mid-teens. Its durable business is expected to deliver profitability through the current economic cycle.

Delta Air Lines emphasized that sustained free cash flow generation of $4 billion should help it strengthen its balance sheet and reduce debt. It is committed to improving its investment-grade metrics, which should further reduce the cost of debt.

Delta Air Lines reported free cash flow of just $200 million in 2022, and this number increased to $2 billion in 2023. In 2024, it expects free cash flow to range between $3 billion and $4 billion. In the first six months of 2024, Delta reported free cash flow of $2.7 billion. A widening base of free cash flow should help it pay down debt at an accelerated pace. In the last 12 months, it has reduced long-term debt from $16.87 billion to $14.08 billion.

This should help Delta Air Lines end 2024 with a debt-to-EBITDAR (earnings before interest, tax, depreciation, amortization, and restructuring or rent costs) of between 2x and 3x, compared to 5x in 2022.

Is Delta Air Lines Stock Undervalued?

Analysts expect Delta Air Lines to grow its adjusted earnings by 2% to $6.75 per share in 2024 and by 16% to $7.39 per share in 2025. So, priced at 7.2x forward earnings, DAL stock is really cheap, given that the sector median multiple is far higher at 19.2x.

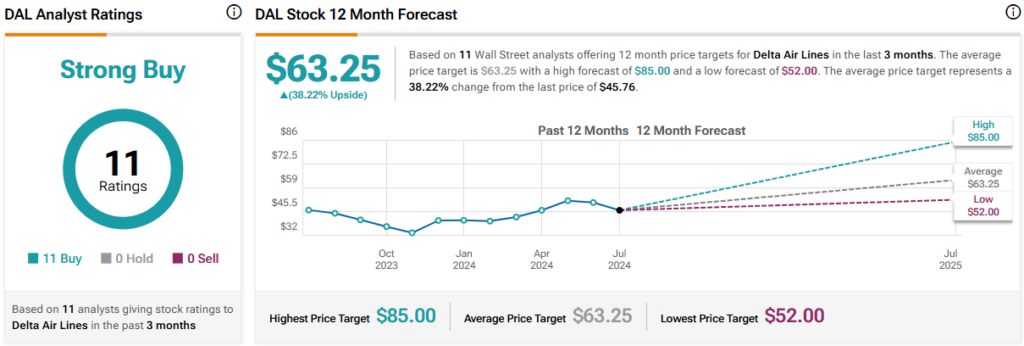

Is Delta Air Lines Stock a Buy, According to Analysts?

Each of the 11 analysts tracking Delta Air Lines stock has a Buy rating, indicating a Strong Buy consensus rating. The average DAL stock price target is $63.25, indicating upside potential of 38.2% from current levels.

The Takeaway

Delta Air Lines is struggling with lower profit margins and earnings despite strong travel demand. However, its improving cash flow and lower debt should help the company navigate a complex macro environment with relative ease. Additionally, the low valuation makes DAL stock look like a top investment choice right now.