2022 has been a “how low can you go” competition in which even the stock market’s heaviest hitters have participated. For instance, Amazon (AMZN) stock has taken a sound beating and has overindulged to the downside; the shares have shed a hefty 49% throughout the year.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

Concerns around the growth prospects for both the e-commerce segment and for AWS have come at the same time the company has been in heavy investment mode.

Looking at Amazon’s actions, Needham’s Laura Martin thinks that its economic model has “problems created by itself.”

As an example, Martin notes that while she still expects FY22 revenues will reach $510 billion, costs will amount to almost $500 billion, and that means for a whole year of work, in FY22, operating income for 1 million employees will be around $11 billion (a 2% op margin).

“Why is AMZN running a not-for-profit enterprise?” asks Martin, who notes that with $510 billion of annual revenues, the company “clearly has scale.”

“Is AMZN in a lousy business or do they do a lousy job running it?” Martin further asks. Martin has no bone to pick with cost cutting being high on Amazon’s agenda. “We don’t object,” she says. “However, investors also want AMZN to demonstrate upside pricing power in 2023, since cost-cutting has limits to driving valuation upside.”

As for the numbers, Martin keeps the Q4 estimates the same, calling for Total Net Sales of $144.9 billion (a 5% year-over-year increase) and EPS of $0.13 (down by a hefty 91% from the same period a year ago).

However, there are changes to the FY2023 forecast. Martin now expects Total Net Sales of $564 billion, amounting to an 11% YoY uptick yet 5% below the previous outlook, and EPS of $1.85 – a big improvement over the $0.16 loss expected this year, yet 15% beneath the prior estimate.

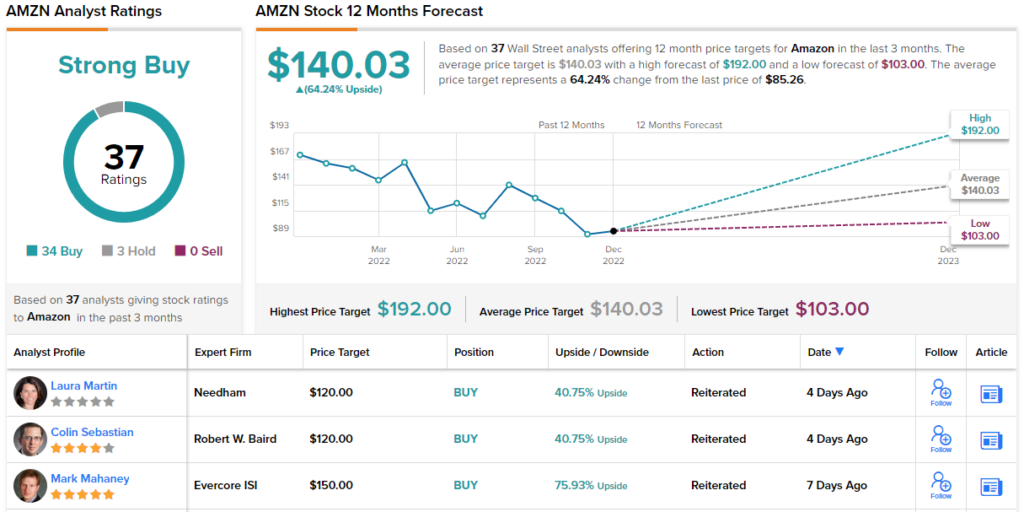

Despite Martin’s reservations regarding the economic model, the analyst remains in Amazon’s corner, reiterating a Buy rating while sticking with the $120 price target. The implication for investors? Upside of 41% from current levels. (To watch Martin’s track record, click here)

Turning now to the rest of the Street, where barring 3 skeptics the 33 other recent reviews are all positive, providing the stock with a Strong Buy consensus rating. The average target stands at $140.03, making room for 12-month gains of 64%. (See Amazon stock forecast on TipRanks)

Special end-of-year offer: Access TipRanks Premium tools for an all-time low price! Click to learn more.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.