At first glance, technology firm Garmin (GRMN) – which among many other business units, specializes in GPS devices and wearable connected innovations – doesn’t appear a compelling buy. Indeed, with sharp double-digit losses for the year, GRMN stock initially looks like a sell. Nevertheless, the underlying company caters to trends that have yet to materialize but may very well do so. Therefore, I am long-term bullish on Garmin.

As stated above, the immediate framework for the tech company is likely to repulse many investors, particularly those averse to risk. Since the opening volley of this year through the close of the Aug. 17 session, GRMN stock has dropped 26% in market value. Over the trailing-year period, Garmin has hemorrhaged 40%.

While it hasn’t given up all of its post-pandemic gains, it’s getting close. Plus, as tech firms, in general, are struggling – with the Nasdaq Composite index conspicuously lagging the benchmark S&P 500 – bidding up GRMN stock aggressively doesn’t seem like a wise move.

Moreover, financial reasons exist to be skeptical about Garmin. In late July, the company released its results for the second quarter, presenting a mixed bag. Per Reuters, the tech firm reported a net income of $1.33 per share. Garmin’s adjusted earnings were $1.44 per share. Here, the results met Wall Street’s expectation, which called for earnings of $1.44 a share.

However, the top line presented a less-than-ideal picture. Garmin rang up sales of $1.24 billion, missing analysts’ consensus target of $1.36 billion.

Finally, management stated that full-year 2022 earnings would be $4.90 per share. Previously, though, the leadership team had forecast $5.90. In addition, the consensus estimate among analysts was $5.90. Still, despite the hiccups, GRMN stock could be built for the long haul.

GRMN Stock and the Wearables Catalyst

It’s easy to forget within the madness of the new normal that prior to the COVID-19 pandemic, one of the major talking points in the business ecosystem was Alphabet (GOOG, GOOGL) via Google acquiring Fitbit, a popular manufacturer of fitness trackers. However, Garmin is also a fierce competitor in the arena, offering myriad consumer options – including fashion and hybrid smartwatches.

Fortuitously and cynically, Garmin’s total addressable market for its fitness trackers and smartwatches expanded due to two key reasons. Number one, Americans’ waistlines have gotten wider. Number two, inflation at multi-decade highs incentivizes one-off purchases rather than subscription-based fees (such as gym memberships).

First, the American Psychological Association (APA) reported from its survey that since the COVID-19 pandemic started, 42% of respondents disclosed that they gained more weight than they intended. “Of those, they gained an average of 29 pounds (the median amount gained was 15 pounds), and 10% said they gained more than 50 pounds, the poll found.”

Not surprisingly, the APA noted that “Such changes come with significant health risks, including higher vulnerability to serious illness from the coronavirus.” To gain back control of their lives, impacted people need to get on a fitness regimen. However, soaring consumer prices prevent easy access to fitness-related services.

That’s where Garmin’s fitness trackers come into play. While these devices aren’t exactly cheap, they represent a one-and-done type of acquisition. In other words, it’s personal and financial health all rolled under one convenient package.

Garmin Stock and the GPS Angle

According to TipRanks contributor Alex Galanis, “Garmin has been a pioneer in the wireless device industry for the last 30 years, as the company name has become a synonym for the use and commercialization of GPS services.” Today, Galanis writes, “the usage of global positioning (GPS), global navigation satellite (GNSS) and other global satellite receivers, lies at the heart of the vast majority of the company’s offerings, providing accurate and reliable navigation information to users.”

As with the wearables narrative, two dynamics provide brewing relevance: one, cars on U.S. roadways have hit a record in terms of age, and two, employers are increasingly likely to recall their workers.

A few months ago, The Wall Street Journal mentioned that the average age of vehicles on U.S. roadways hit a record 12.2 years. Further, the news outlet reported that this “was the fifth straight year the average vehicle age in the U.S. has increased.” By logical deduction, not everyone has leveled up to modern cars with integrated GPS systems, which means continued relevance for Garmin navigation-related products.

On the second point, traffic activity will likely increase as employers fade out their COVID-related work-from-home privileges. Indeed, with Google executives allegedly warning their employees about “blood on the streets” if productivity doesn’t pick up, there’s less incentive to stand out unnecessarily – such as complaining about not being able to work from home.

Is GRMN Stock a Good Buy?

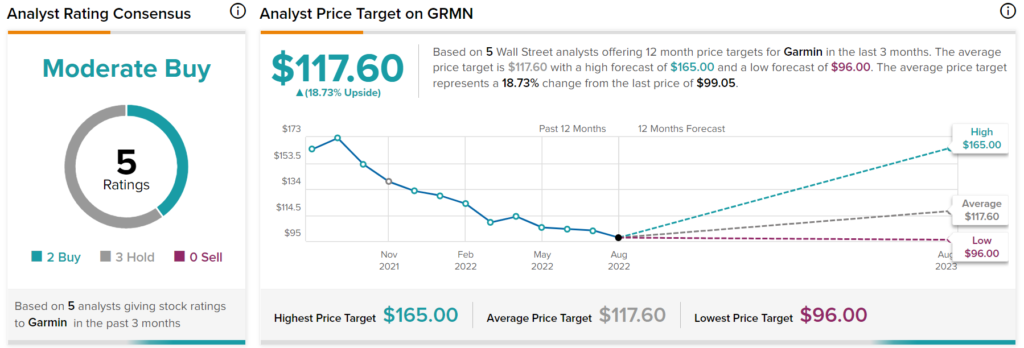

Turning to Wall Street, GRMN stock has a Moderate Buy consensus rating based on two Buys, three Holds, and no Sells assigned in the past three months. The average GRMN price target is $117.60, implying 18.7% upside potential.

Takeaway – Garmin Stock Investors Need to be Patient

Those who decide to invest in GRMN stock will likely have to wait a while until the broader narrative shifts favorably. For now, the tech sector faces enormous pressures from rising borrowing costs that disincentivize growth-oriented investments. Still, over the long run, Garmin presents an interesting thesis. With society poised toward a fuller return to normal – along with consumers attempting to cure the secondary consequences of the pandemic – GRMN stock just needs some patience to blossom.

Questions or Comments about the article? Write to editor@tipranks.com